Update: TravelSky (696 HK)

GDS monopoly turned into a SaaS growth story at 11x P/E

Disclaimer: Asian Century Stocks uses information sources believed to be reliable, but their accuracy cannot be guaranteed. The information contained in this publication is not intended to constitute individual investment advice and is not designed to meet your personal financial situation. The opinions expressed in such publications are those of the publisher and are subject to change without notice. You are advised to discuss your investment options with your financial advisers, including whether any investment suits your specific needs. From time to time, I may have positions in the securities covered in the articles on this website. Full disclosure: I do not hold a position in TravelSky at the time of publishing this article. To reiterate, this post and the presentation below are for informational and educational purposes only — not a recommendation to buy or sell shares.

A quick background

Chinese aviation tech company TravelSky (696 HK — US$3.7 billion) was one of the first companies I ever wrote about on Asian Century Stocks:

In short, it's a state-owned monopoly that handles the bookings and inventory of almost all Chinese airlines.

The company was initially formed by the Civil Aviation Administration of China. This was back in 1979 when the opening-up reforms were just getting started. A few years later, TravelSky launched China's first air ticket inventory control system.

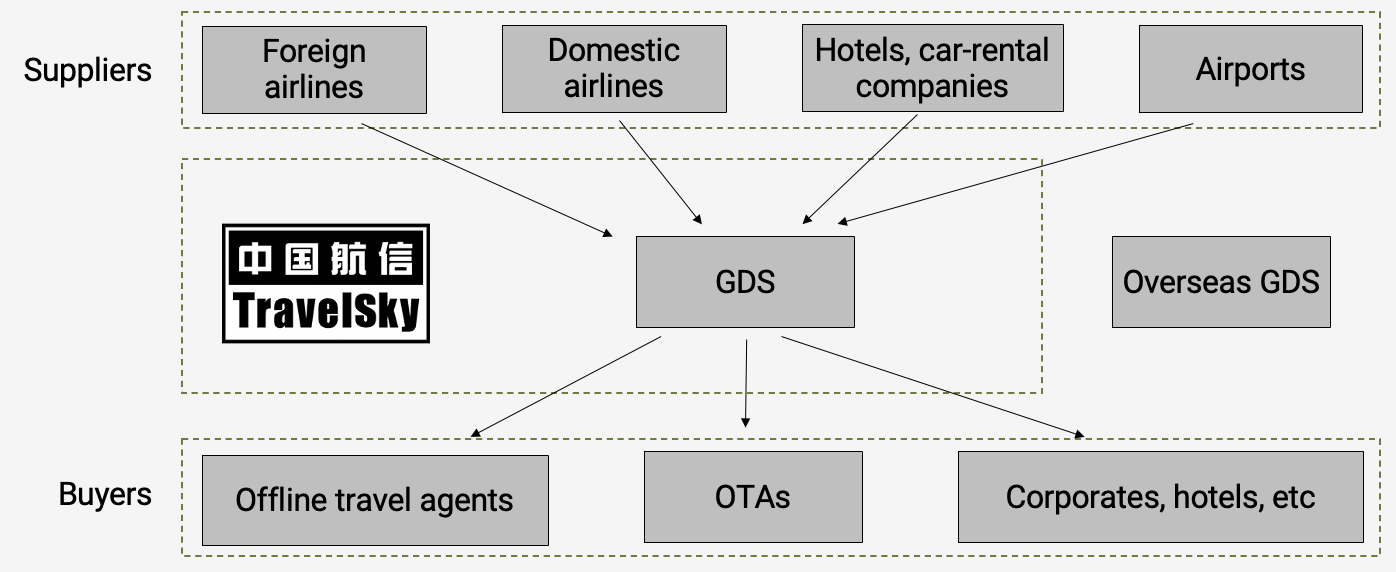

Technically, the software is known as a global distribution system (GDS). You can think of them as the backbone of the air travel industry, linking airlines with travel agents and other buyers of airline tickets. The airlines provide the system with seat inventory, pricing, etc. The GDS then aggregates the content and sends it to offline and online travel agents, corporate buyers, hotels, etc.

A global distribution system like TravelSky's has the following key features:

- An air ticket inventory control system, helping airlines disseminate flight information, fares, availability, client details, etc. Roughly 40 local airlines and 350+ foreign airlines are using the system.

- An air ticket computer reservation system, helping travel agents book flights across airlines. TravelSky has 70,000+ software terminals spread across 8,000+ agencies, both domestically and overseas.

- A departure control system that helps airports with check-in, boarding pass issuance and load planning at the airport gate

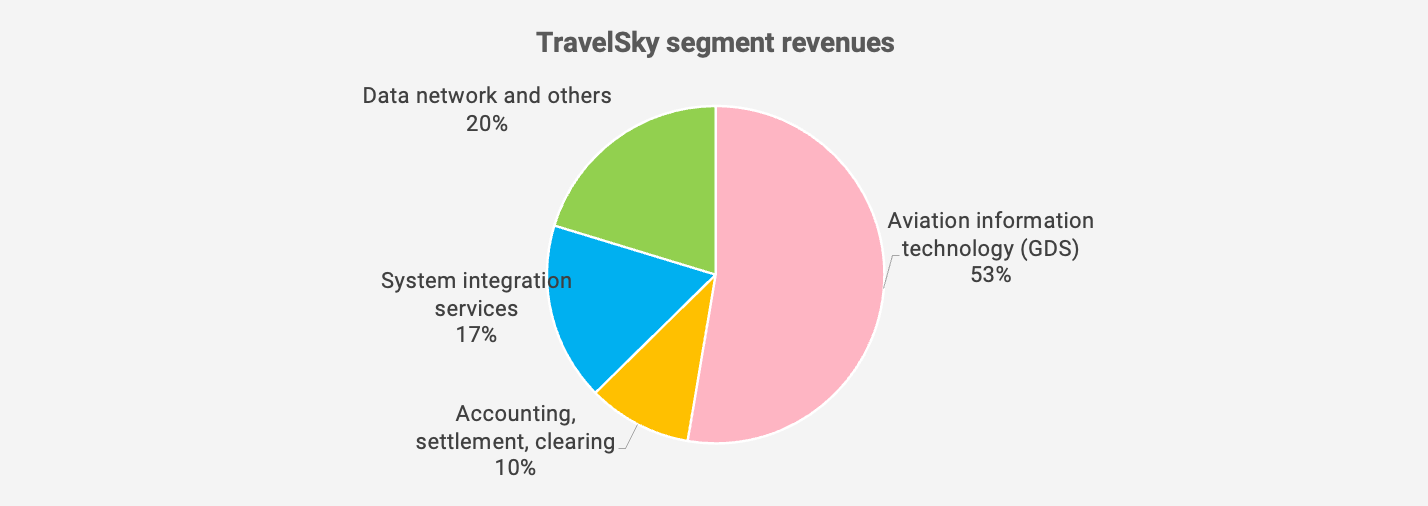

Revenues from these features are reported as part of TravelSky's aviation information technology segment, which in a normal year has represented 50% of revenues.

In addition, TravelSky has an accounting, settlement and clearing system, in which it acts as a payment processor or a clearing house.

Then, there's a system integration business where TravelSky installs hardware and software for airports, airlines and cargo operators on a project-by-project basis.

And finally, TravelSky has a segment called data network where travel agents, hotels, and other travel companies pay TravelSky for real-time access to its inventory data. But its global distribution system remains the core of its business.

Here's a diagram of TravelSky's position in China's airline industry as a provider of air ticket inventory control systems, booking systems, airport software, and related services:

So why can't airlines send their ticket information directly to the likes of Expedia and Trip.com? Because there are thousands of smaller travel agents and aggregators that rely on a single source of information when searching for all available flights. Airlines do not have an incentive to facilitate such comparisons.

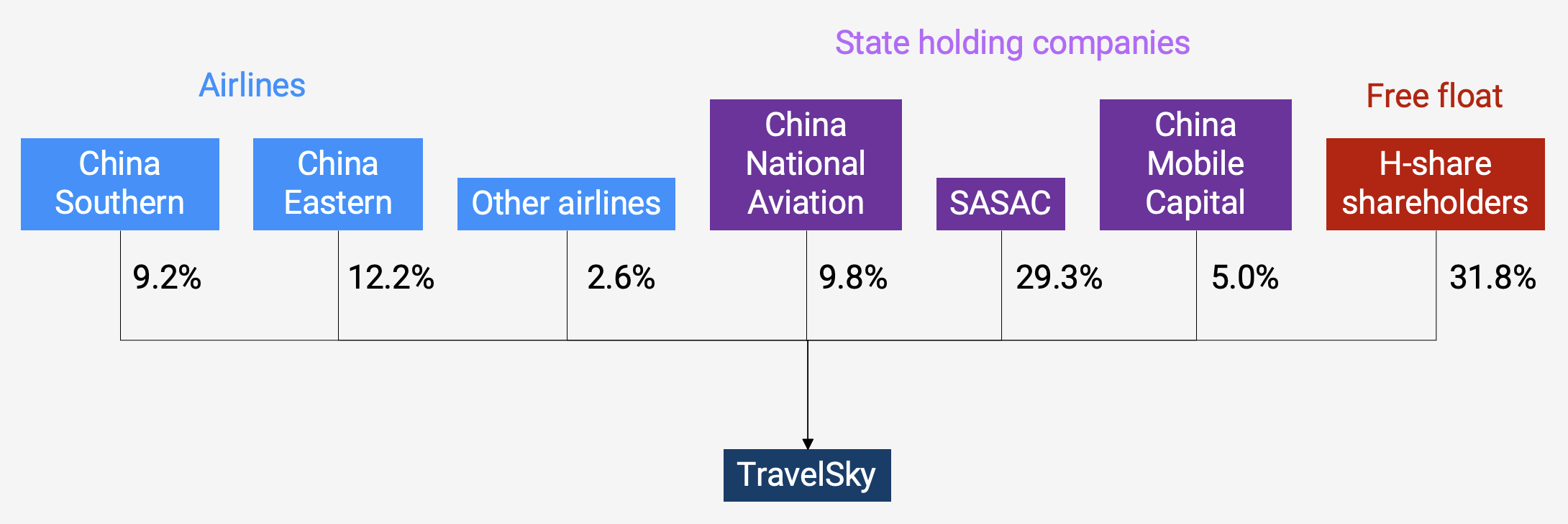

TravelSky is essentially a monopoly, and it enjoys the full support of the Chinese government. Its biggest shareholder is the government's State-owned Assets Supervision and Administration Commission of the State Council (SASAC). Other shareholders include China's major airlines Air China, China Southern and China Eastern, making TravelSky entrenched in the local airline industry.

Globally, there are several competitors, including Sabre (SABR US — US$747 million) in the United States and Amadeus (AMS SM – US$28 billion). But unlike these companies, TravelSky has virtually zero competition in China, with a 95% domestic market share.

The monopoly has been fraying at the edges. In 2012, a rule change allowed foreign airlines operating in China to use TravelSky's global GDS competitors. For domestic flights, however, TravelSky remains the only GDS provider.

When I first wrote about TravelSky, I noted that its earnings growth had been volatile. Part of the reason was its new operations center in Beijing, which came with massive data centers and weighed on the income statement with approximately CNY 200 million in extra expenses. However, that was a one-off hit that would become less important over time.

While hit hard by the COVID-19 pandemic, I felt TravelSky would eventually recover. The main issue was that China's borders were closed. But I predicted that the borders would eventually open.

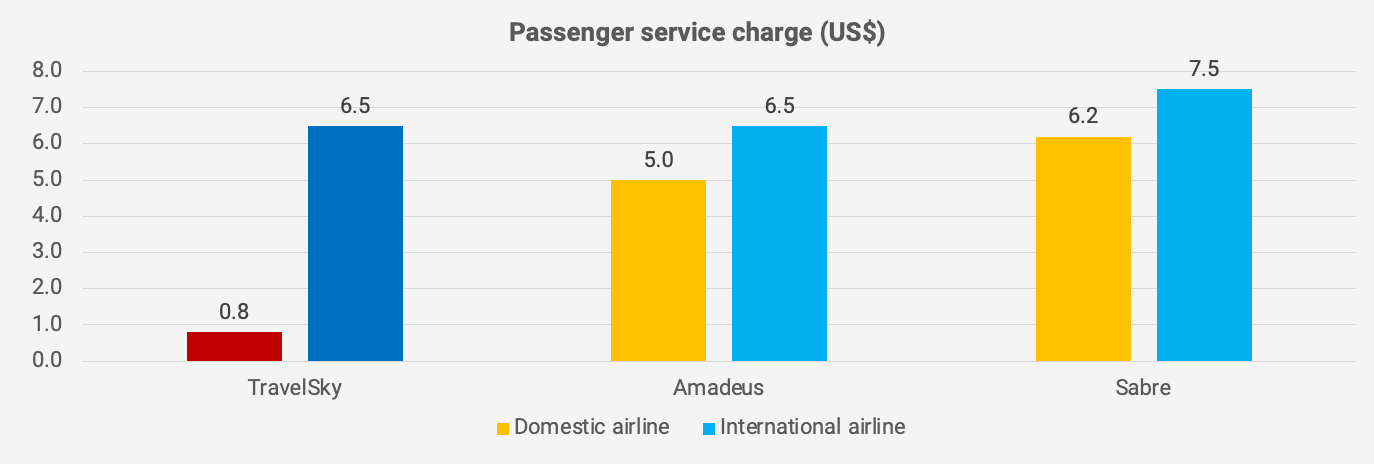

The international border reopening was important for TravelSky, because it charged international airlines more than 4x that of domestic:

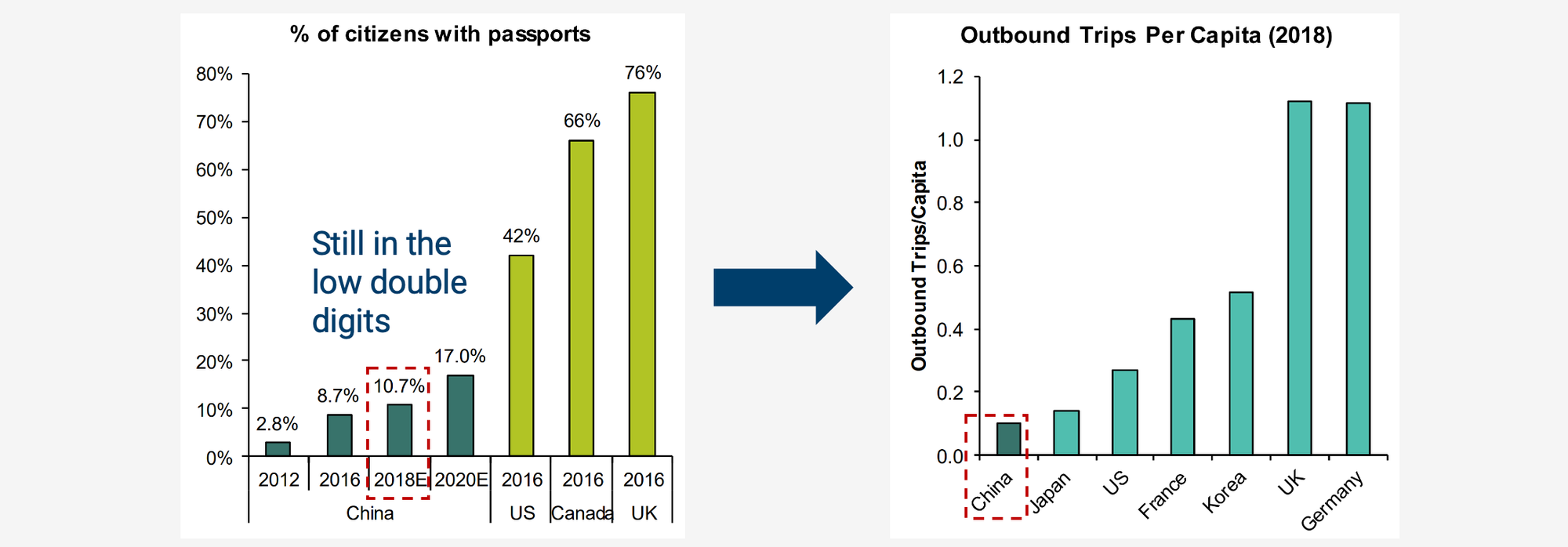

The border reopening would also help Chinese tourism close the gap with that of other countries. At the time of writing, only 10% of Chinese citizens owned a passport, compared to roughly half of Americans. And China's air travel penetration rate was only 0.4x trips per capita compared to 1.7 in South Korea.

The beautiful thing about TravelSky's business model is the fact that additional transactions are highly margin-accretive. But with almost 10% yearly growth in air traffic, TravelSky could easily defend its margins, or even see them expand.

At around HK$13/share, I foresaw a 2024e P/E ratio of 10x, at the lower end of TravelSky's historical trading range. Peers such as Amadeus traded at twice the P/E multiple.

The main issue with TravelSky was that, despite being a monopoly, it had been unable to raise its fees. There was a cap of CNY 10 per passenger for booking fees and airport passenger processing fees taken together. And the airlines sitting on its board would also object to any price increases. That's why the domestic booking charge remained less than US$1 per transaction – much lower than the US$5 charged by international competitors.

Another frequent concern is that online travel agents like Trip.com would replicate TravelSky's inventory control or booking systems. Apparently, they had tried, but smaller travel agents tend not to want to use competitors' systems. So, for completeness, everyone has continued to use TravelSky to offer their customers the best flight combinations at the lowest cost.

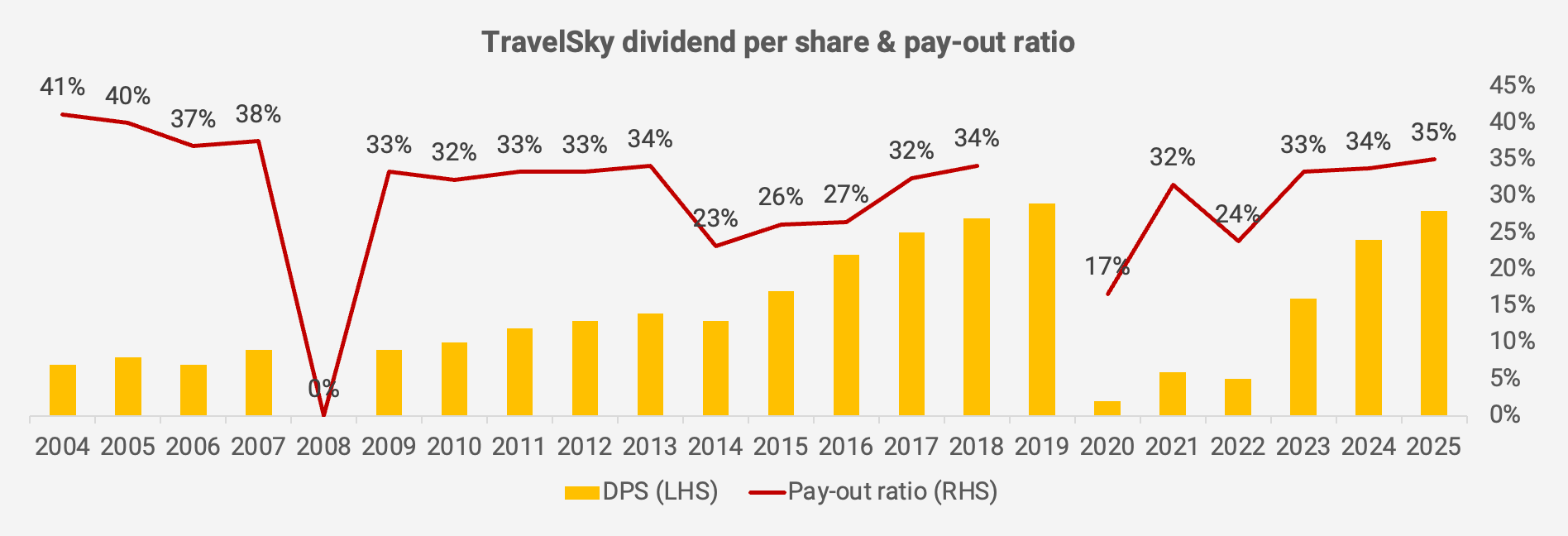

The balance sheet was clean with a solid net cash position. However, the dividend payout ratio was weak at just 35%, with zero share buybacks:

And there had been several asset injections, including the current accounting, settlement & clearing software, which was purchased from the parent back in 2018. In 2018, it also entered into a joint venture with China Merchants Group to create and sell insurance products. Several investors, including Terry Smith's Fundsmith, saw these transactions and decided to sell their stakes. However, there's more to the story.

An update to my original post

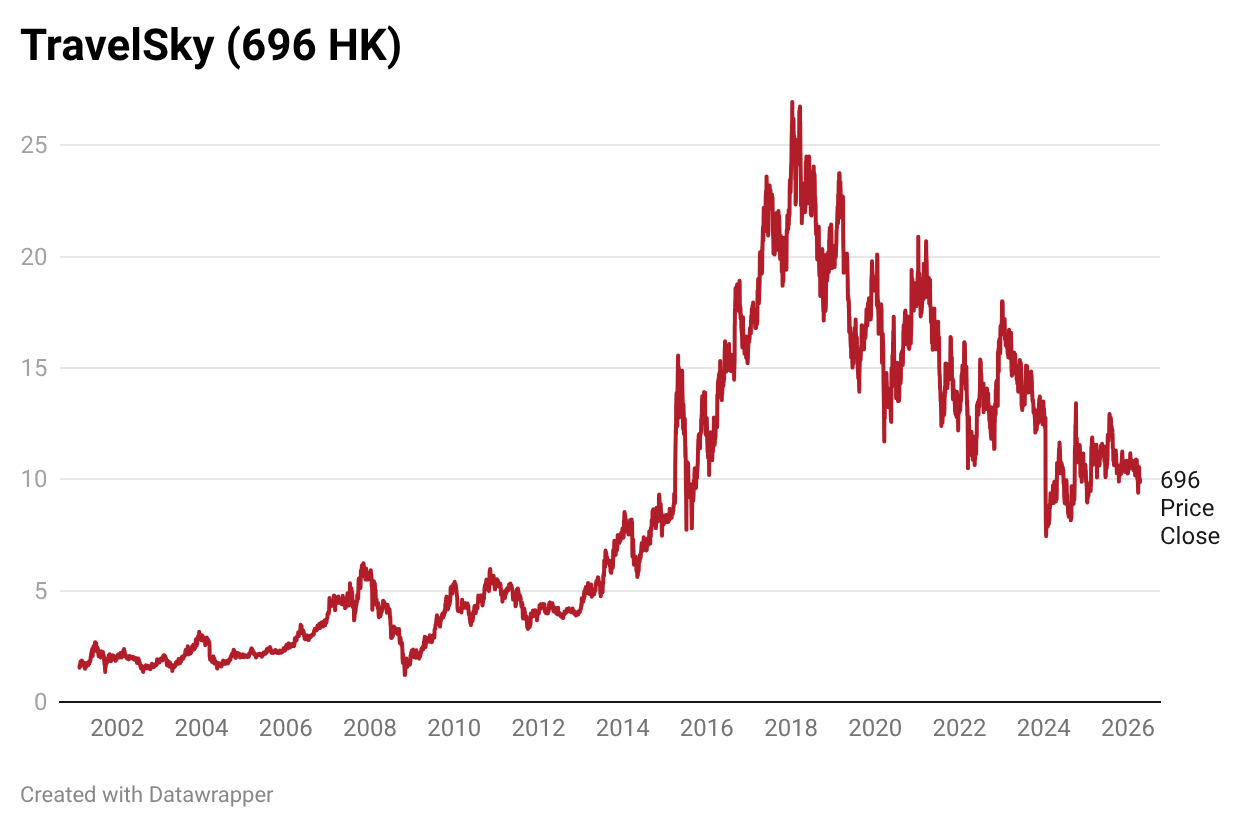

Since my initial write-up in 2021, TravelSky's stock price has drifted lower by another 20%: