TOA Paint (TOA TB)

Thailand’s paint leader at 8x P/E and 6.5% dividend yield

Hi! Welcome to a subscriber-only edition of Asian Century Stocks – a newsletter about Asian value stocks. For a complete list of all previous posts, check out the Table of Contents.

Disclaimer: Asian Century Stocks uses information sources believed to be reliable, but their accuracy cannot be guaranteed. The information contained in this publication is not intended to constitute individual investment advice and is not designed to meet your personal financial situation. The opinions expressed in such publications are those of the publisher and are subject to change without notice. You are advised to discuss your investment options with your financial advisers, including whether any investment suits your specific needs. I do not hold a position in TOA Paint at the time of publishing this article. To reiterate, this post and the presentation below are for informational and educational purposes only—not a recommendation to buy or sell shares.

TOA Paint (TOA TB — US$713 million) is Thailand's biggest paint manufacturer, with a 49% market share.

The company has been around since 1964, and has been run by second-generation leader Jatuphat Tangkaravakoon since 2001. Its market share has been stable, with TOA dominating the mass market, leaving the premium segment to Nippon Paint and AkzoNobel.

The business is straightforward. Mix ingredients in one of TOA's 9 factories across Southeast Asia, and then distribute them to its 8,600 retail partners. Many of them are equipped with TOA's automatic tinting machines, which help ensure customer loyalty, as customers often want to mix paint themselves.

It's challenging to judge paint quality, and the downside risks are clear, especially for health. So many contractors and consumers default to tried-and-tested brand names. And that gives TOA pricing power, explaining its current 20% return on equity.

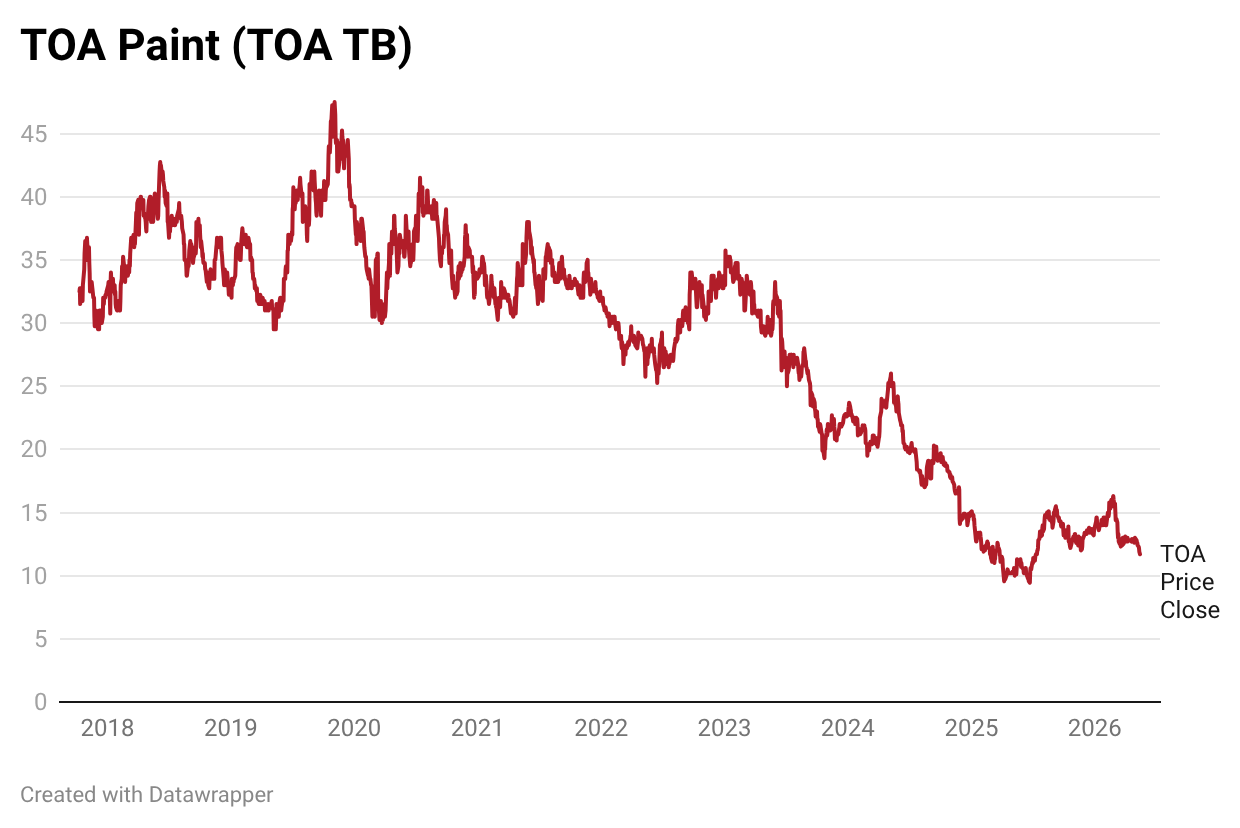

The stock has now come off 70% since 2019, despite its earnings per share rising by half:

Why? There have been three main reasons: