NICE Information Service (030190 KS)

The FICO of South Korea at 10x P/E

Hi! Welcome to a subscriber-only edition of Asian Century Stocks – a newsletter about Asian value stocks. For a complete list of all previous posts, check out the Table of Contents.

Disclaimer: Asian Century Stocks uses information sources believed to be reliable, but their accuracy cannot be guaranteed. The information contained in this publication is not intended to constitute individual investment advice and is not designed to meet your personal financial situation. The opinions expressed in such publications are those of the publisher and are subject to change without notice. You are advised to discuss your investment options with your financial advisers, including whether any investment suits your specific needs. I do not hold a position in NICE Information Service at the time of publishing this article. To reiterate, this post and the presentation below are for informational and educational purposes only—not a recommendation to buy or sell shares.

On Wednesday, I published a guide to Asia's publicly-listed credit bureaus.

In that guide, I argued that credit bureaus were essentially toll booths on lending. Before granting a loan, a bank will request a credit report. And the credit bureaus will then send over a credit report at almost zero marginal cost.

That's why I paid special attention to South Korea's NICE Information Service (030190 KS — US$564 million) ("NICE IS"). Its margins remain lower than its peers, yet they're moving steadily higher.

NICE IS holds a 71% market share in Korea's consumer credit scoring industry, owning the so-called "NICE Score". This credit score is the closest you'll get to a FICO score in South Korea and helps banks assess a borrower's creditworthiness.

Banks can also purchase more comprehensive credit reports on the borrower, allowing them to better understand payment behavior with more granular data.

The consumer business is clearly the jewel. But NICE also has a corporate credit information business that sells reports on 4.2 million Korean businesses. Competition is greater in this segment, but NICE remains dominant domestically.

In addition, NICE IS owns a debt collection and credit investigation business, included in its asset management segment. It also owns a bond valuation business, an advertising business, and a capital markets information business that's now ramping up to compete with FnGuide.

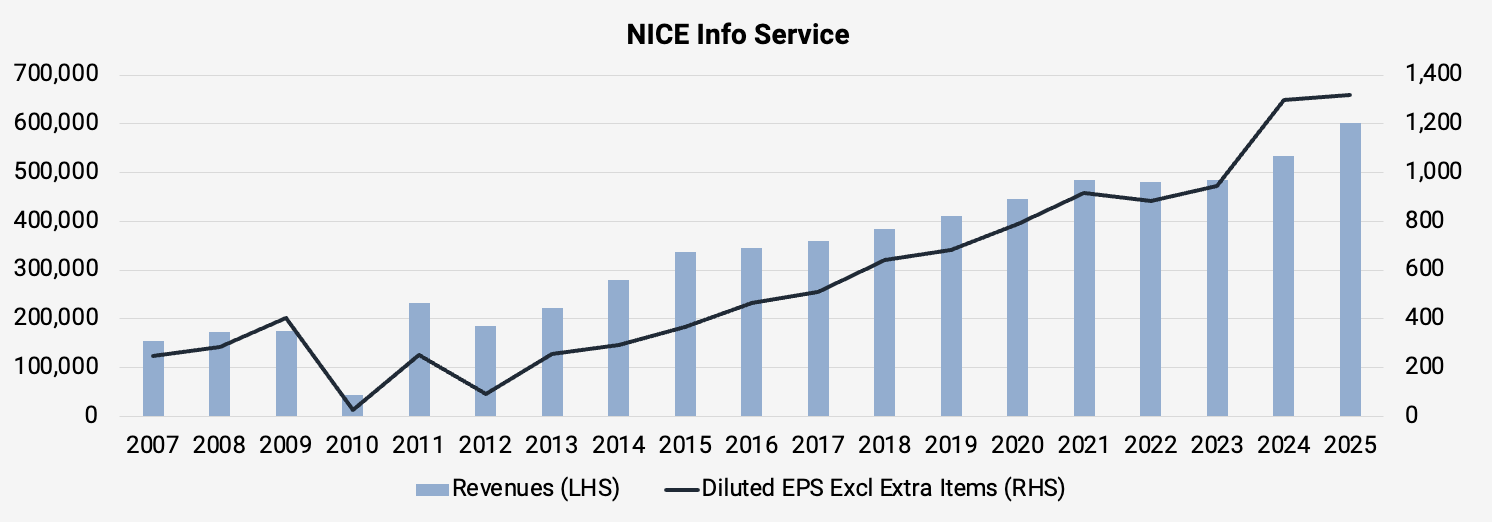

NICE IS's historical track record has been impressive. In the past decade, its revenues have compounded at a 6% annual rate, and its earnings per share at 14%: