The toll booths of lending

Asia's publicly listed credit bureaus

Disclaimer: Asian Century Stocks uses information sources believed to be reliable, but their accuracy cannot be guaranteed. The information contained in this publication is not intended to constitute individual investment advice and is not designed to meet your personal financial situation. The opinions expressed in such publications are those of the publisher and are subject to change without notice. You are advised to discuss your investment options with your financial advisers. Consult your financial adviser to understand whether any investment is suitable for your specific needs. I may, from time to time, have positions in the securities covered in the articles on this website. This is not a recommendation to buy or sell stocks.

We're living in an uncertain world.

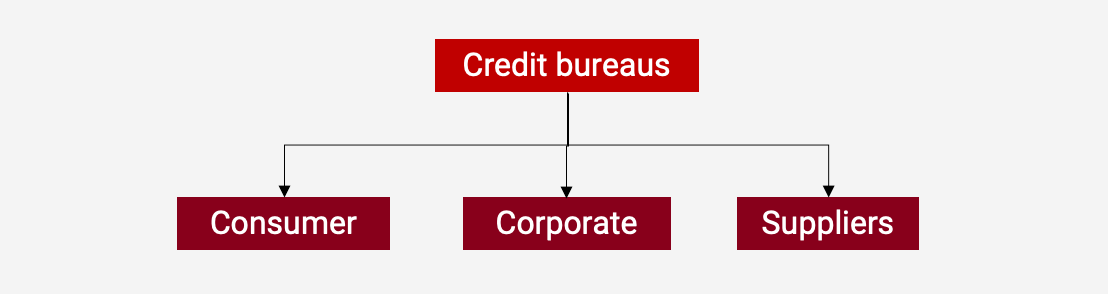

To manage risks, banks and companies gather information on their counterparties. And one way to do so is to buy data from so-called "credit bureaus", also known as "credit reporting agencies".

These credit bureaus gather information on borrowers' creditworthiness. These include consumers, corporate borrowers, and trade counterparties. The data is then used to support lending decisions, ensuring that each lender is comfortable with their exposures.

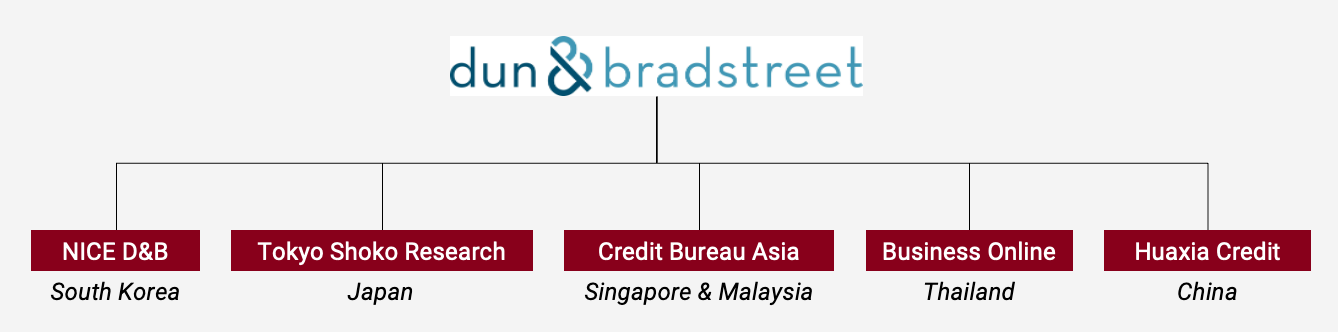

One of the current giants of the industry, Dun & Bradstreet, was set up in 1841 to provide credit information to its subscribers. Suppliers wanted to know whether they should sell on credit. And it quickly became a major business. Fun fact: four US presidents worked at Dun & Bradstreet: Abraham Lincoln, Ulysses Grant, Grover Cleveland and William McKinley.

In Asia, the first credit bureau was Tokyo Shoko Research, founded in 1892, soon after the Meiji Restoration. Teikoku Databank was set up shortly thereafter, and these two continue to dominate the Japanese credit bureau industry. Taiwan's credit bureau industry developed in the 1960s, and Korea's in the 1980s. More recently, it's become more developed in Singapore and Malaysia, too.

On the corporate side, credit bureaus collect all sorts of data on private businesses: business registration numbers, legal addresses, ownership data, the executive leadership, name changes, etc. And more importantly, they collect data on revenues, profitability, and leverage from public filings, interviews, payment data, etc. They also cooperate with debt collectors to understand whether each business has had payment issues in the past.

All this data then ends up in credit reports, which you can purchase for US$150 each. Historically, these credit bureaus made money by selling credit reports a la carte. But today, the entire industry has moved towards subscriptions that generate much higher-quality, recurring, and sustainable revenue. If you're an ongoing subscriber, you'll get alerts if there are any changes to the creditworthiness of any particular counterparty.

The global market leaders on the corporate side include Dun & Bradstreet, Experian and Equifax:

Dun & Bradstreet, in particular, owns the DUNS number: an identifier that allows you to check a company's creditworthiness. If you want to deal with a multi-national, or sell to the US government, or become a developer for the Apple software ecosystem, you'll need a DUNS number. It's almost become a prerequisite for international trade.

Several local credit bureaus in Asia have therefore cooperated with Dun & Bradstreet through various joint ventures, as it gives customers access to data on international counterparties:

Buyers of corporate credit data tend to be small- and medium-sized enterprises that want to know whether they extend favourable credit terms to their counterparties. Or banks that want to know how to extend credit to. The local Asian credit bureaus have almost impenetrable market positions, as they've gathered detailed information on millions of businesses. And the reports can be purchased for very little money, while costing almost nothing to produce. No serious lender would skip a US$50 credit check before extending a half-million loan.

The consumer side has an even stronger moat. The global leaders within this niche include Experian, Equifax and TransUnion:

And because collecting consumer data is sensitive, it is highly regulated and therefore protected. The buyers of credit data tend to be financial institutions that want to know whether to extend a mortgage or consumer loans.

There are clear network effects: in many cases, credit bureaus get data on consumer borrowers from their bank customers, who willingly provide the information in exchange for data on other banks' borrowers. So the bureaus almost become central exchanges that become difficult to displace.

On the other hand, the heavy regulation also means that pricing power tends to be limited. So it's a scale business, with significant operating leverage if credit growth for whatever reason starts to accelerate.

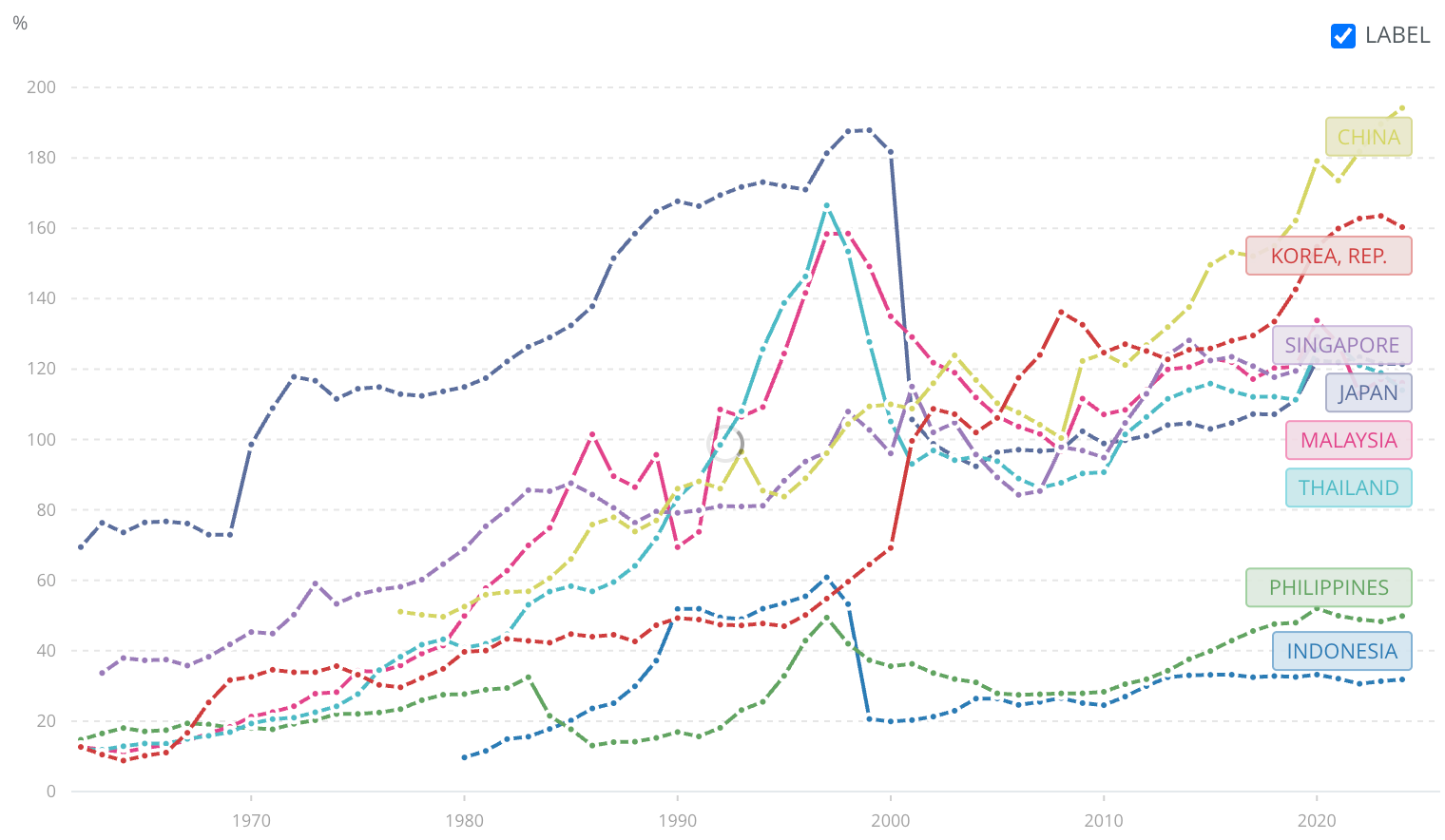

And this is the exact bull case for Asia's credit bureaus: the credit penetration in this part of the world remains low, especially in emerging Asian nations like Indonesia and the Philippines:

Several of these countries have had significant informal economies, with unbanked individuals only recently opening bank accounts. That should mean natural growth for the credit bureaus operating in the region.

Another bull case is that fact that standardized credit scores haven't become popular yet. Americans use FICO scores to judge consumer creditworthiness, and PAYDEX scores to judge corporate creditworthiness. But outside of South Korea, such credit scores are rarely used in lending decisions, perhaps because of a lack of data. And that's bullish for the providers of more sophisticated scoring models, especially on the consumer side.

A complicating factor is that some countries, such as China, the Philippines and Malaysia, have state-backed public credit registries that compete directly with the private bureaus. Although when it comes to credit scoring models, there's still room for the private sector, as we've seen in Malaysia, where private-sector credit bureau CTOS Digital now reigns supreme.

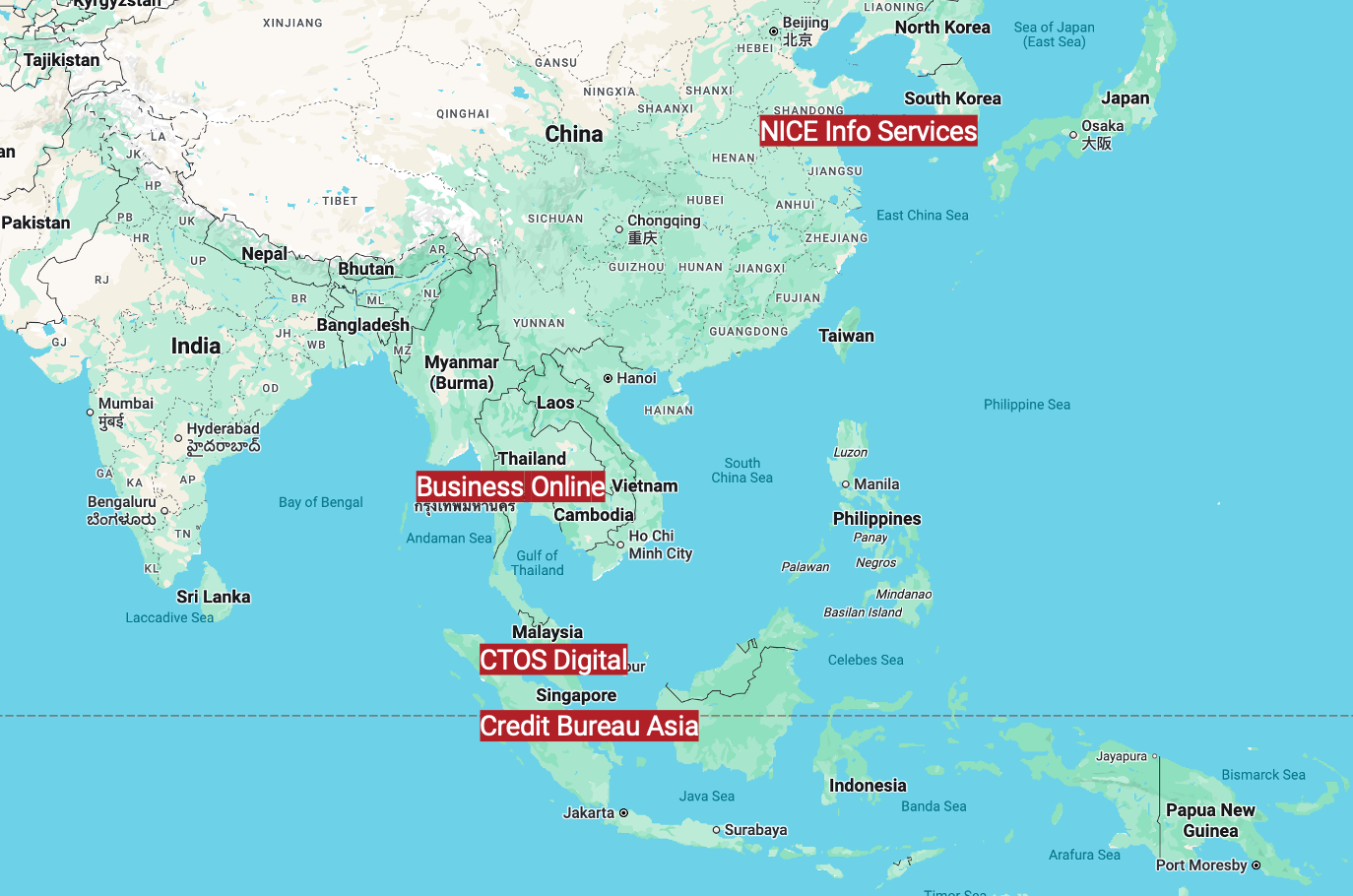

Here's a map of the four biggest publicly-listed credit bureaus in Asia:

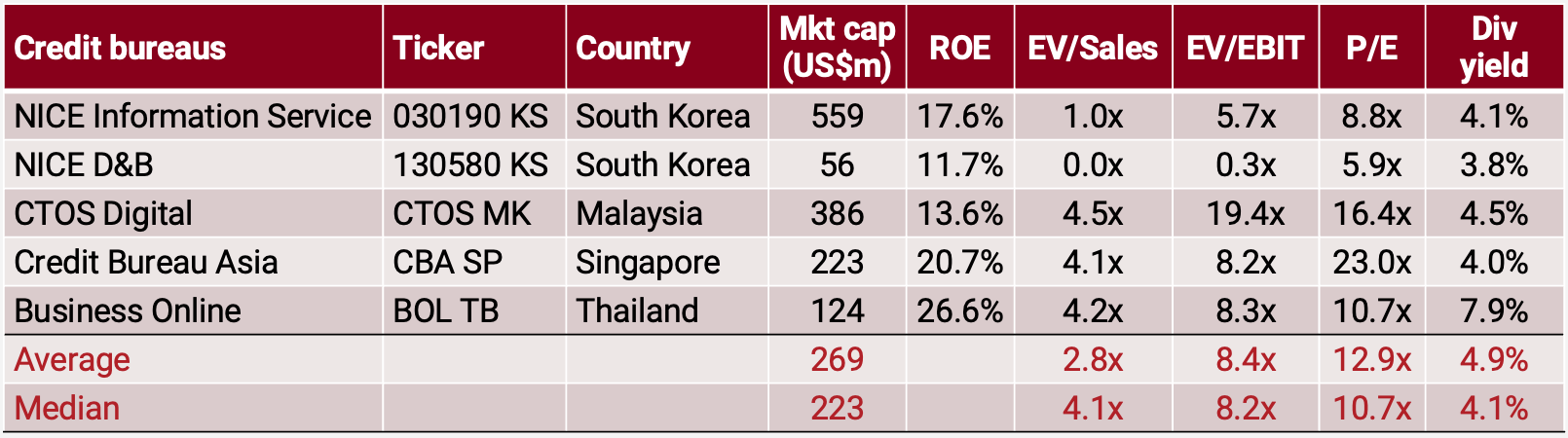

These are all small caps, but still worth paying attention to. Let's start with Singapore's Credit Bureau Asia (CBA SP – US$223 million):

This consumer-focused credit bureau absolutely dominates the Singapore market. It aggregates credit information from banks, repackages it into credit reports, and sells it back to its key bank customers. The consumer segment represents roughly half of revenues. Corporate business is conducted through a partnership with Dun & Bradstreet, serving SMEs that need credit reports. While the company has new entities in Cambodia and Myanmar, Singapore still accounts for 96% of revenues. What separates Credit Bureau Asia from many others is that it has historically been very generous with dividend payments, paying out at least 90% of profits.

The market leader in Malaysia is called CTOS Digital (CTOS MK – US$386 million), and is similarly focused on the consumer market. The top five Malaysian banks are its biggest customers, and also the major providers of credit data. It also has a corporate business representing more than a third of revenues, also primarily serving SMEs. It's not affiliated with Dun & Bradstreet, however. CTOS also has a direct-to-consumer business where individuals can buy their own credit reports. CTOS apparently has a 71% market share, with 15 million consumer profiles and 8 million business records. Note that CTOS has a 25% market share in Thailand's Business Online. And it also has separate data-scoring operations in Indonesia and the Philippines, using alternative data sources to assess creditworthiness. Finally, CTOS has a license to use the FICO score in the ASEAN region, though it hasn't yet had much success scaling this business. Optimism about CTOS's growth prospects is likely what drove Mobius Capital Partners to take a position in CTOS back in 2024, according to its FY2024 annual report.

CTOS's Thai associate, Business Online (BOL TB — US$124 million), has a more corporate focus. Its core platform, Corpus X, allows customers to check 1.6 million Thai company records. It's used by both local banks and SMEs to understand corporate creditworthiness. In addition, Business Online has a joint venture with Dun & Bradstreet, serving local customers dealing with international counterparts. Business Online's stock price has been hurt by the weak Thai economy since 2023, though it returned to growth in 2025.

In South Korea, you have NICE Information Service (030190 KS — US$559 million). It's a subsidiary of NICE Holdings (034310 KS – US$309 million) that focuses primarily on the consumer segment. It was formed in 2010 through the merger of Korea Information Service and "National Information & Credit Evaluation", hence the name. 70% of revenues come from the consumer credit-scoring business, which calculates a FICO-like "NICE score" for consumer borrowers. The company also has a corporate business, and a debt collecting agency.

Dun & Bradstreet's Korean partner NICE D&B (130580 KS – US$56 million) is a joint venture between parent NICE Holdings and Dun & Bradstreet. Just like its Southeast Asian peers, NICE D&B sells corporate credit information to Korean companies and allows them to access Dun & Bradstreet global credit reports. It's somewhat odd that D&B continues to be a separately listed entity from NICE Information Service, but it is what it is.

I will admit that these companies are all relatively mature. I expect CTOS Digital to grow slightly faster, given Malaysia's low credit penetration and its new Indonesia / Philippines business. The other companies are probably high-single-digit growers.

On the positive side, valuation multiples have now fallen to surprisingly low levels, in some cases below 10x P/E.

Business Online, in particular, has been beaten down, mostly due to macroeconomic reasons beyond its control. And there's a good chance that Thai credit growth will eventually pick up.

The biggest question, in my mind, is to what extent these businesses will be threatened by the advent of generative AI tools. The consensus view is that the consumer is well protected because the data is nonpublic. It's fed into the system by the customers themselves. So CTOS Digital, NICE Information Service and Credit Bureau Asia should probably not be materially affected by generative AI.

There might be a bigger problem on the corporate side, where some of the data comes from the public domain: corporate registries, filings, litigation records, etc. If a competitor can scrape the data effortlessly and offer it at a lower price, then they could certainly lose market share. If so, Business Online and NICE D&B would be at risk.

However, I question that narrative. Even on the corporate side, credit bureaus get at least some of their data from financial institutions and corporations. While some public data is available, it's not always easy to access. And scraping websites was possible even before generative AI. So my personal view is that these credit bureaus will probably not be affected much by AI and will continue to grow at a high single-digit rate, if not higher.

If you enjoyed this post, consider becoming a premium subscriber: