Misto (081660 KS)

Titleist and FILA at 9.1x P/E

Hi! Welcome to a subscriber-only edition of Asian Century Stocks – a newsletter about Asian value stocks. For a complete list of all previous posts, check out the Table of Contents.

Disclaimer: Asian Century Stocks uses information sources believed to be reliable, but their accuracy cannot be guaranteed. The information contained in this publication is not intended to constitute individual investment advice and is not designed to meet your personal financial situation. The opinions expressed in such publications are those of the publisher and are subject to change without notice. You are advised to discuss your investment options with your financial advisers, including whether any investment suits your specific needs. I do not hold a position in Misto Holdings at the time of publishing this article. To reiterate, this post and the presentation below are for informational and educational purposes only—not a recommendation to buy or sell shares.

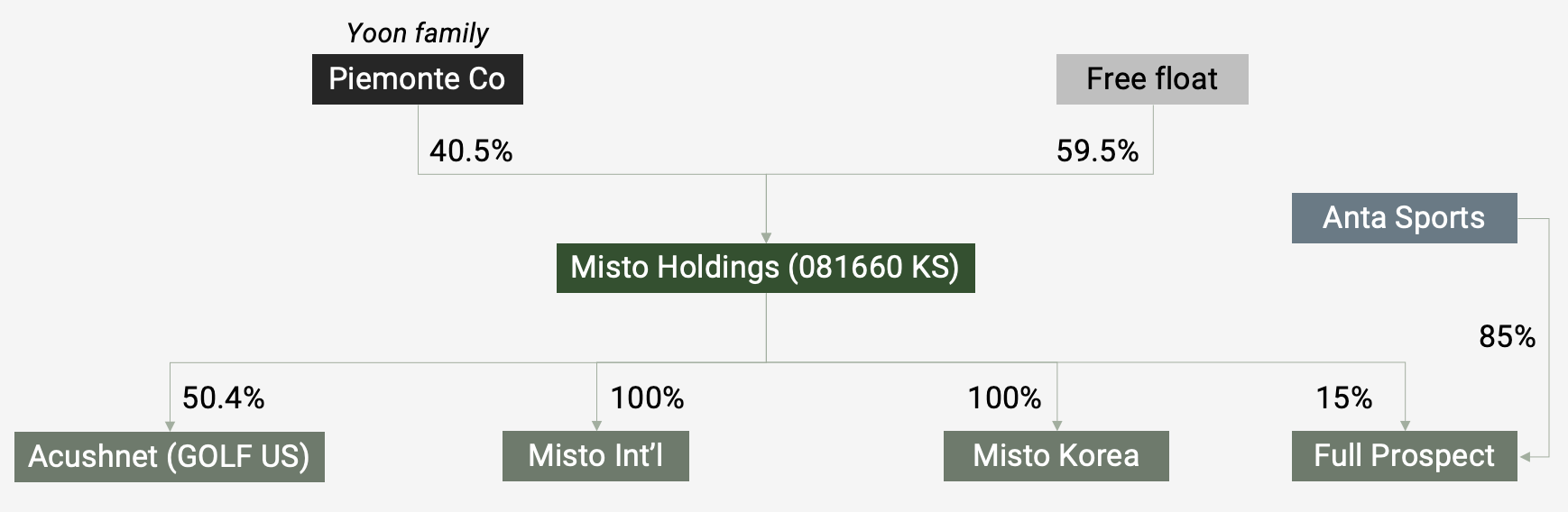

Few people know that the golf brand Titleist and the fashion brand FILA are actually controlled by the Korean company, Misto Holdings (081660 KS — US$1.4 billion).

It was created by superstar Korean entrepreneur Gene Yoon back in 1991. Initially, it served as FILA's distributor in South Korea. But after FILA encountered financial difficulties in the mid-2000s, Gene teamed up with a private equity firm to take the entire global FILA business private. And he's been running it ever since.

In 2011, Gene used the same playbook to acquire a stake in the US golf equipment company Acushnet – the owner of the famous Titleist brand.

In the late 2010s, the FILA brand had a resurgence, as consumers took a liking to retro-style shoes. However, the fad proved short-lived, and FILA lost market share to more fashion-forward brands such as Hoka, On, and ASICS.

After the share price came down, Gene took advantage of the low price to increase the family's stake from 20.1% to 40.5%. And the family is now firmly in control of a business that owns 50.4% stake in Acushnet, along with a 100% stake in FILA's global, ex-China business.

Ihina, Misto runs its business through a 15%-owned joint venture called "Full Prospect", together with local partner Anta Sports. In addition, Misto receives a 3% royalty fee on any revenue generated in China. This set-up has been enormously successful, with FILA now being the third-most-popular foreign sportswear brand in Mainland China.

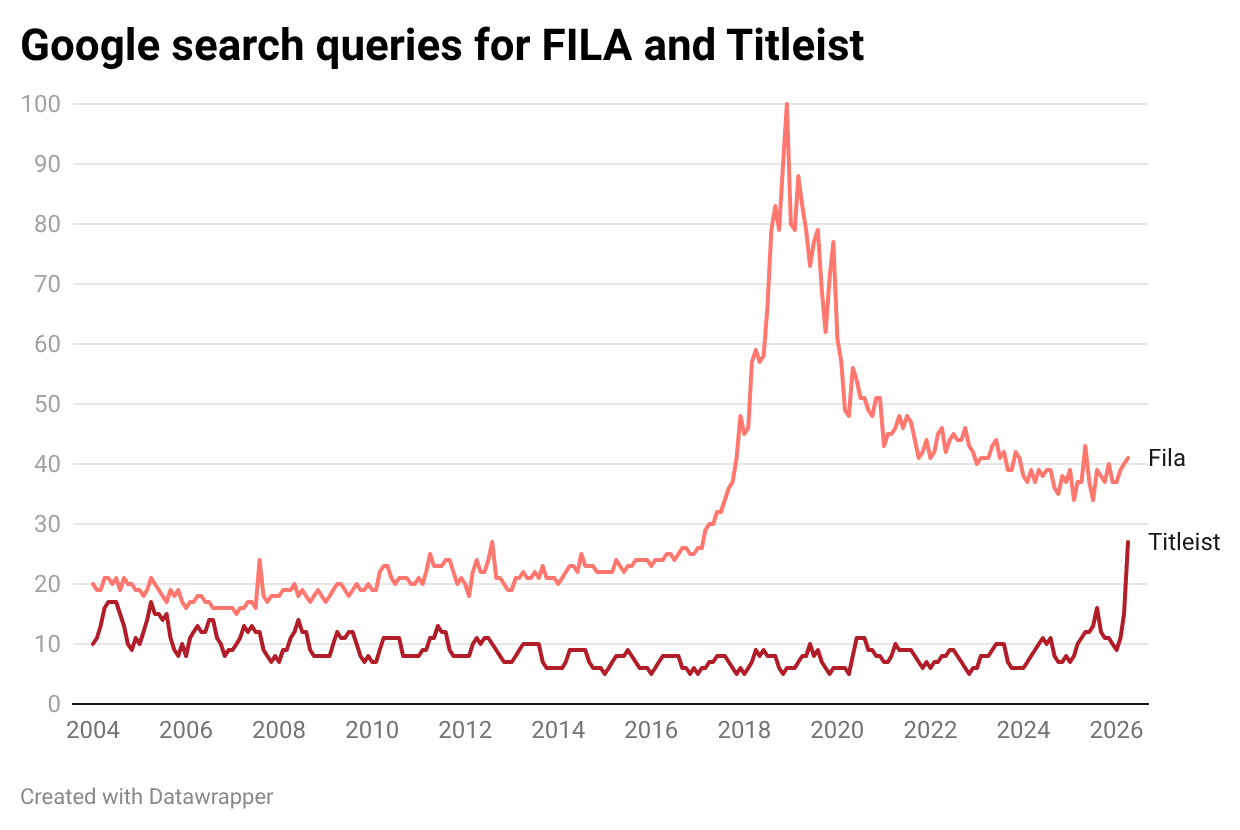

In any case, it looks like Misto's fundamentals are turning positive. Our friends at TickerTrends recently made the case that consumer interest in Acushnet's brand Titleist has turned up and that it's gaining market share from Callaway. This improvement could be related to new product releases, such as the T-Series irons or the success of Titleist ambassador Rory McIlroy.

FILA's 1990s-style "ugly-chic" sneakers have been out of fashion for a while now. But from early 2026 onwards, I've been encouraged to see low-profile, slim silhouette sneaker releases such as the Ritmo Sleek and GLIO models. These are a clear step in the right direction.

An index of Google search queries for the keyword "FILA" bottomed out in early 2026 and seems to be improving, on the margin.

Perhaps even more important is the fact that Gene has finally stepped down. He's been a master deal-maker, but also unable to grow the key FILA brand internationally. With his son Kevin Yoon taking over, I am hopeful that he can bring new life to the business.

The major shift we've seen recently is the December 2025 cancellation of 7 million treasury shares, equivalent to 11.7% of shares outstanding. In addition, Kevin has designed a new Value Up plan that targets capital returns of up to KRW 500 billion per year between 2025 and 2027, roughly 25% of the current market cap.

Today, Misto trades at 9.1x current-year P/E with a clean balance sheet. There is some debt in its US golf subsidiary, Acushnet, but with a very comfortable EBIT interest coverage ratio of 5.1x. A sum-of-the-parts valuation of Misto with a 25% holding company discount puts the intrinsic value per share at KRW 86,000 – more than double the current share price.

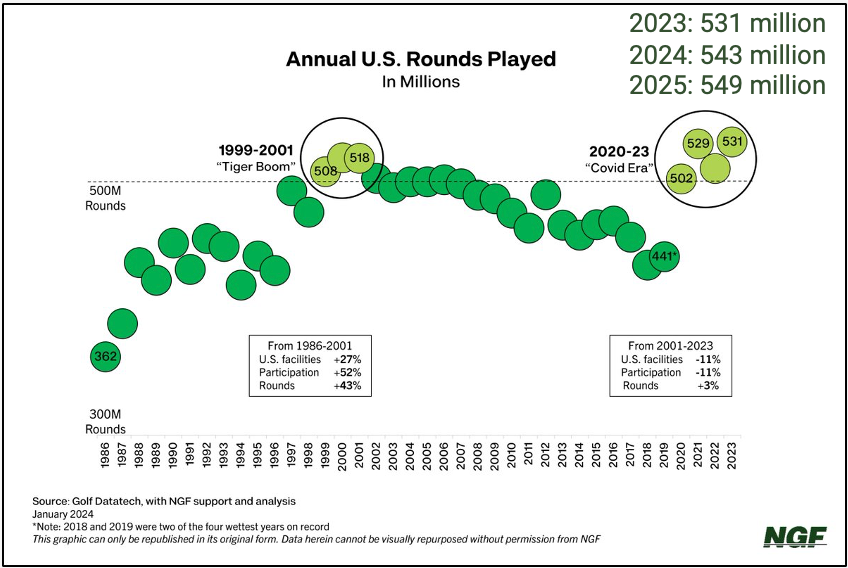

A question mark for some investors is whether the recent increase in golf rounds played in the United States will eventually revert to pre-COVID levels, hurting Acushnet's golf ball business.

On the other hand, baby boomers are now retiring, and golf is an obvious leisure activity for increasingly health-conscious Americans. And it seems like Titleist is now gaining market share.

Another question mark is the succession risk. Kevin seems to be focused on improving Misto's capital allocation. But on the other hand, he recently acquired an expensive new headquarters building in the fancy Gangnam district in central Seoul. Some are now questioning his priorities.

I've spoken to investors and noticed that there's not much excitement about Misto so far. While Interactive Brokers has opened up access to Korean equities, most international investors remain focused on momentum stocks.

So whether there'll ever be any excitement about Misto will probably depend on the success of FILA's ongoing turnaround. And that turnaround is still early in the making. But it's certainly one I will track closely over the next one or two years.

NOTE! This was just a summary of the actual deep dive. To view the full PowerPoint presentation, click the link below:

Further material:

- Misto's 2025 annual report

- Misto's March 2026 Value-up plan

- Substack writer Alex Morris's take on Acushnet ($)

- A 2022 write-up by Sextant on Value Investors Club ($)