Toll Bridge Investing

The perfect business model

Disclaimer: Asian Century Stocks uses information sources believed to be reliable, but their accuracy cannot be guaranteed. The information contained in this publication is not intended to constitute individual investment advice and is not designed to meet your personal financial situation. The opinions expressed in such publications are those of the publisher and are subject to change without notice. You are advised to discuss your investment options with your financial advisers. Consult your financial adviser to understand whether any investment is suitable for your specific needs. I may, from time to time, have positions in the securities covered in the articles on this website. This is not a recommendation to buy or sell stocks.

The Ambassador Bridge

In 1979, the American entrepreneur Matty Moroun purchased the Ambassador Bridge for US$30 million, buying a large stake from Warren Buffett, who had also expressed an interest in it.

This was the deal of the century. US$30 million was nothing compared to the potential profits of owning one of the only border crossings between the United States and Canada.

The bridge is now earning over US$60 million per year, as there are few substitutes in the immediate vicinity. There are almost 6.5 million border crossings annually, accounting for 25% of all trucks entering and exiting Canada.

And in addition, passenger tolls rose from US$0.75 to US$10 today. In real terms, the tolls have increased roughly three times. The pricing power has been almost unrestricted.

Later on, Buffett commented that a business like the Ambassador Bridge is almost the perfect business model:

"In an inflationary world, a toll bridge would be a great thing to own because you've laid out the capital costs. You built it in old dollars, and you don't have to keep replacing it."

In other words, zero capital requirements and a growing annuity that could potentially last forever.

The problem with "economic moats"

When most of us think about business quality, we borrow Warren Buffett's concept of an "economic moat":

"A truly great business must have an enduring ‘moat’ that protects excellent returns on invested capital."

The idea is that he wants to buy a great business and make sure it stays great. A valuable castle needs a "moat" to protect it from potential invaders.

In Buffett's writing, he mentioned some sources of such moats, including owning a valuable brand name, network effects, switching costs, economies of scale, and regulation.

The problem with the economic moat concept, however, is that it doesn't necessarily predict future returns. The return from any investment must necessarily come from either:

- Higher revenues

- Higher margins

- Lower share count

- Higher valuation multiple

- Dividend yield during the period of ownership

The moat concept doesn't really predict any of these. Moats tell you whether returns will be protected on the downside, but they don't tell you much about the direction and acceleration of demand. For that, we need to compare the product or service with its substitutes.

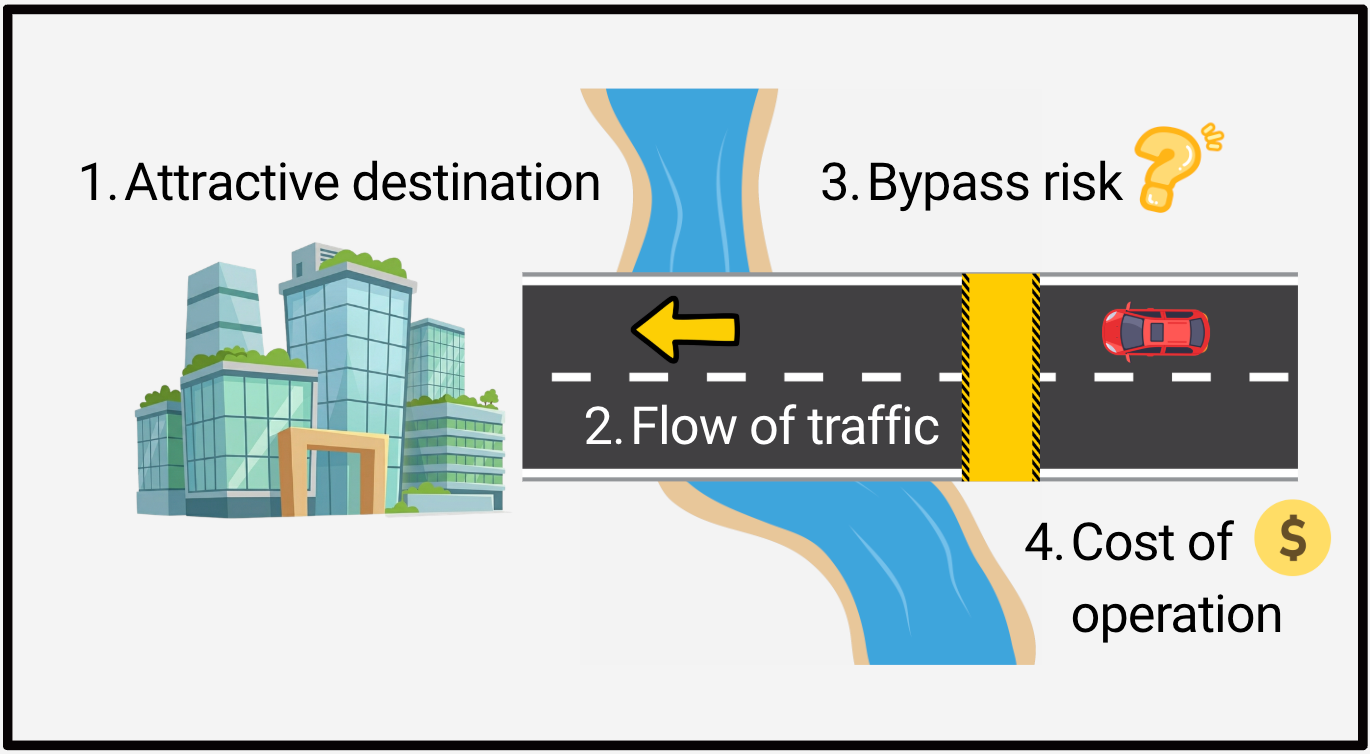

The Toll Bridge Investing Model

Instead, I propose what I call the Toll Bridge Investing Model:

According to this model, an investment can be seen as having four component parts: an attractive destination that a flow of traffic is moving towards, potential substitute roads, and the cost of operating the toll booth.

While Matty Moroun's Ambassador Bridge might have been the ultimate asset, the model can be generalized to any business. Simply judge any investment by how it fits the profile of a scarce, unavoidable chokepoint that benefits from an ongoing flow of traffic.

Let's discuss each of the four parts:

- First, there needs to be an attractive destination. By purchasing the product or service, you'll get somewhere. They can be functional, serving a specific problem, like taking you to Canada. They can entertain by offering something novel that evokes excitement. They can offer a sense of community, as in social media apps. They can reduce risk through well-known brand names. They can signal status, as in Veblen goods. The buyer will usually be able to tell you why he's attracted to it.

- Second, we'll need traffic. The flow of traffic can accelerate due to innovations, new consumer preferences, improved infrastructure, and other factors.

- Look out for bypass risk. Can the car bypass the chokepoint somehow? In other words, are there substitutes to the toll bridge that get customers to the same destination?

- Finally, consider the operational costs. A toll booth costs almost nothing to operate. But if variable costs are high, the chokepoint might not be worth much. Or if the bridge requires a concession from the government, then its bargaining power will be limited.

Toll bridge investing in practice

If this sounds theoretical, let me provide a few examples of companies. These all fit the profile of a scarce, unavoidable chokepoint in an ongoing flow of traffic:

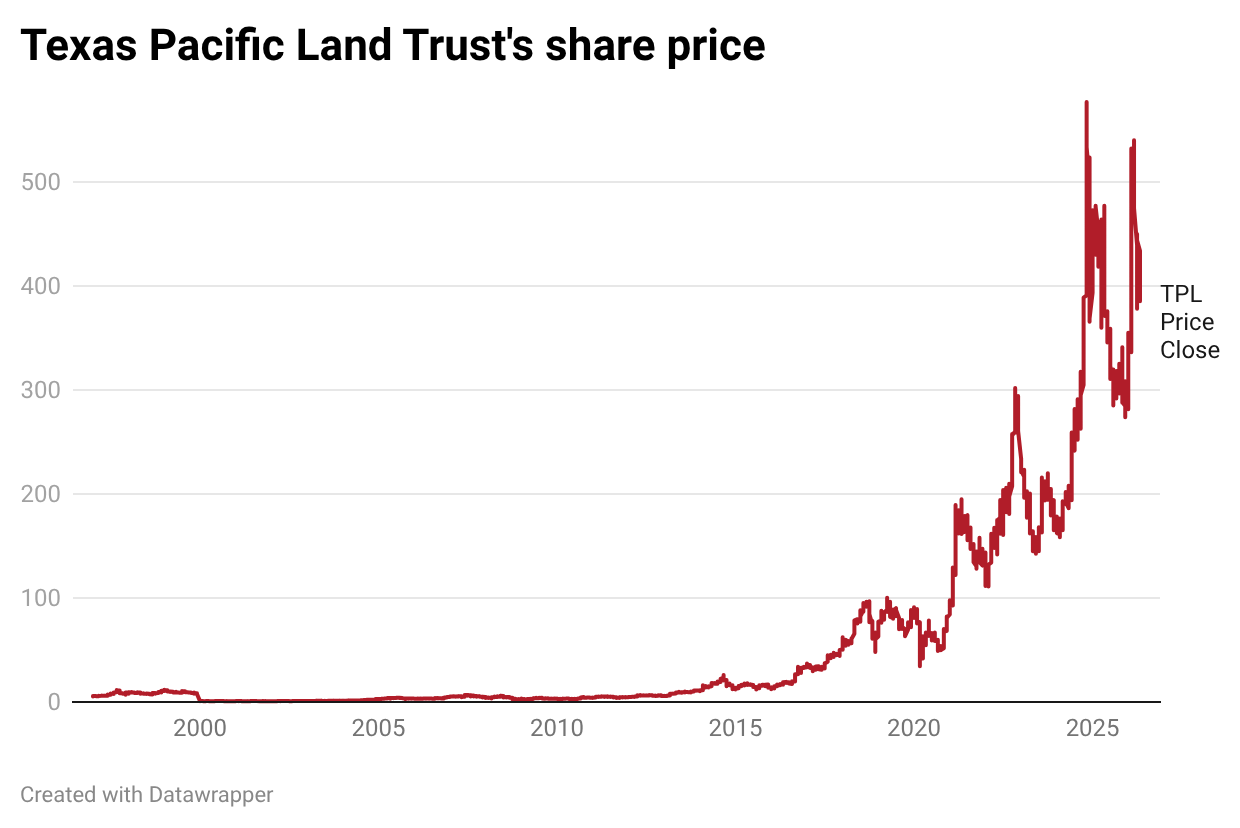

Texas Pacific Land Trust (TPL US – US$27 billion) is a remnant of an US railroad that went bankrupt in 1888.

Thanks to this history, it happens to have accumulated 873,000 acres of land in one of the most oil-rich areas of the world: the Permian Basin.

Now, we all know how attractive oil is: it has an unbeatable energy density, is stable at room temperature, is easy to transport and can be used for a variety of applications, including plastics, textiles, medicines, asphalt, gasoline, etc.

What caused traffic to speed up was the invention of horizontal drilling and fracking. Suddenly, crude oil and natural gas trapped in shale deposits became unlocked. Wildcatters then flocked to the Permian Basin to lease land from Texas Pacific Land Trust, and later even buy water from it.

Since Texas Pacific Land sits on freehold land, there's no way to reach the oil & gas sitting on its acreage without it. In other words, the bypass risk is minimal.

Finally, the cost of selling rights to its land or collecting royalties is virtually zero.

These factors have made Texas Pacific Land one of the prime beneficiaries of the fracking boom. And a perfect example of a toll bridge business model in practice.

Another example is Europe's Amadeus IT Group (AMS SM – US$27 billion). This company is the world's largest global distribution system for airline tickets, serving as a middleman between buyers and sellers. Every time a travel agent books a flight, Amadeus takes a small cut.

In this instance, the attractive destination is where the plane physically lands. We'll want to travel for business, or to bring our families on vacation.

The flow of traffic was primarily sped up by the invention of the jet engine in the 1930s, and popularized after the Second World War. But the cost of air travel has continued to decline as technological innovations have advanced. Today, low-cost airlines have brought down ticket prices to almost nothing.

While airlines could in theory bypass Amadeus, network effects give it an edge in practice. Travel agents will want to search and book across hundreds of airlines simultaneously. Amadeus sits on that database.

Finally, the cost for Amadeus to arrange another transaction is virtually zero.

And so, as you can imagine, Amadeus has performed quite well, except for certain periods when air travel was restricted. Despite technological innovation, it remains a toll for air travel bookings globally.

A third example is the monopoly stock exchange Hong Kong Exchanges and Clearing (388 HK — US$64 billion) ("HKEX").

The exchange is one of the key ways for Chinese companies to access foreign capital. And its Stock Connect program is the primary way that overseas investors are able to get exposure to equities listed in Shanghai and Shenzhen. That's what's attracting investors to HKEX.

While Chinese indices have not performed that well, Hong Kong Exchanges has benefitted from the rising market cap of Chinese equities, catalyzed by the Deng Xiaoping's reforms and other permissible regulation. This has caused the flow of traffic, measured in terms of dollar trading volumes, to rise.

There's very little bypass risk: HKEX is the sole stock exchange, derivatives exchange, and clearing house in Hong Kong. While Chinese companies can access foreign capital in the US, it seems like that window is finally closing. And while foreign investors can invest directly in Shanghai and Shenzhen stocks, they need a scarce QFII license to do so. So the Stock Connect program remains almost a monopoly.

Meanwhile, the cost of arranging yet another trade is minimal. Which explains why its gross margins are currently 97%. It's the toll bridge for capital flowing in and out of China.

Toll Bridge-adjacent business models

The Toll Bridge Investing Model can be generalized to other businesses as well. In my view, every company has some degree of toll bridge characteristics.

For example:

- Enterprise software is so embedded in companies' daily operations that it's not practical to migrate away from it, even if it could, in theory, be replaced. Examples include Australia's Xero. The software helps companies solve practical problems, such as creating financial statements or managing customer relationships, so it's a "destination" worth paying for.

- Testing & inspection companies like Taiwan's Sporton have an edge in approving electronic devices for import to the United States. Customers could, in theory, switch to another testing provider, but the cost is small relative to the shipment value. So these testing & inspection companies tend to act as chokepoints in the global trade of consumer electronics devices.

- Razor-and-blade models, such as ResMed's sleep apnea machines, ensure that once the installed base has been built (the bridge), consumables such as face masks (tolls) will continue to be sold with no practical alternatives.

- Distribution bottlenecks, such as Haad Thip's control of Coca-Cola beverage distribution in southern Thailand, or Ginebra San Miguel's control of the Luzon gin market.

- Data-driven lock-in, such as when a credit reporting company like NICE Information Service accumulates data on millions of borrowers, makes switching to another credit score provider unlikely.

- Standard-setters such as Nvidia, through its CUDA programming language, benefit from having engineers learn the code and incorporate it into their products.

The emphasis here is on businesses that serve as practical chokepoints. With enough effort, any business can be bypassed. But sometimes, the bridge solves the problem neatly, or finding the closest alternative bridge incurs real or perceived costs. Talking to customers will help you understand how likely they are to try to bypass your Toll Bridge.

What can go wrong?

The return from any investment must come from higher revenues, higher margins, a lower share count, a higher valuation multiple, or dividends during the period of ownership.

A key risk is that revenues decline due to lower traffic volume. There could be technological shifts that have made the destination a lot less attractive. Perhaps lower battery costs has made internal combustion engines less useful than before. Perhaps a credit reporting company suffers from a decline in mortgage lending. Or perhaps the airline ticket industry suffers from a drop in airline traffic due to a pandemic like COVID-19.

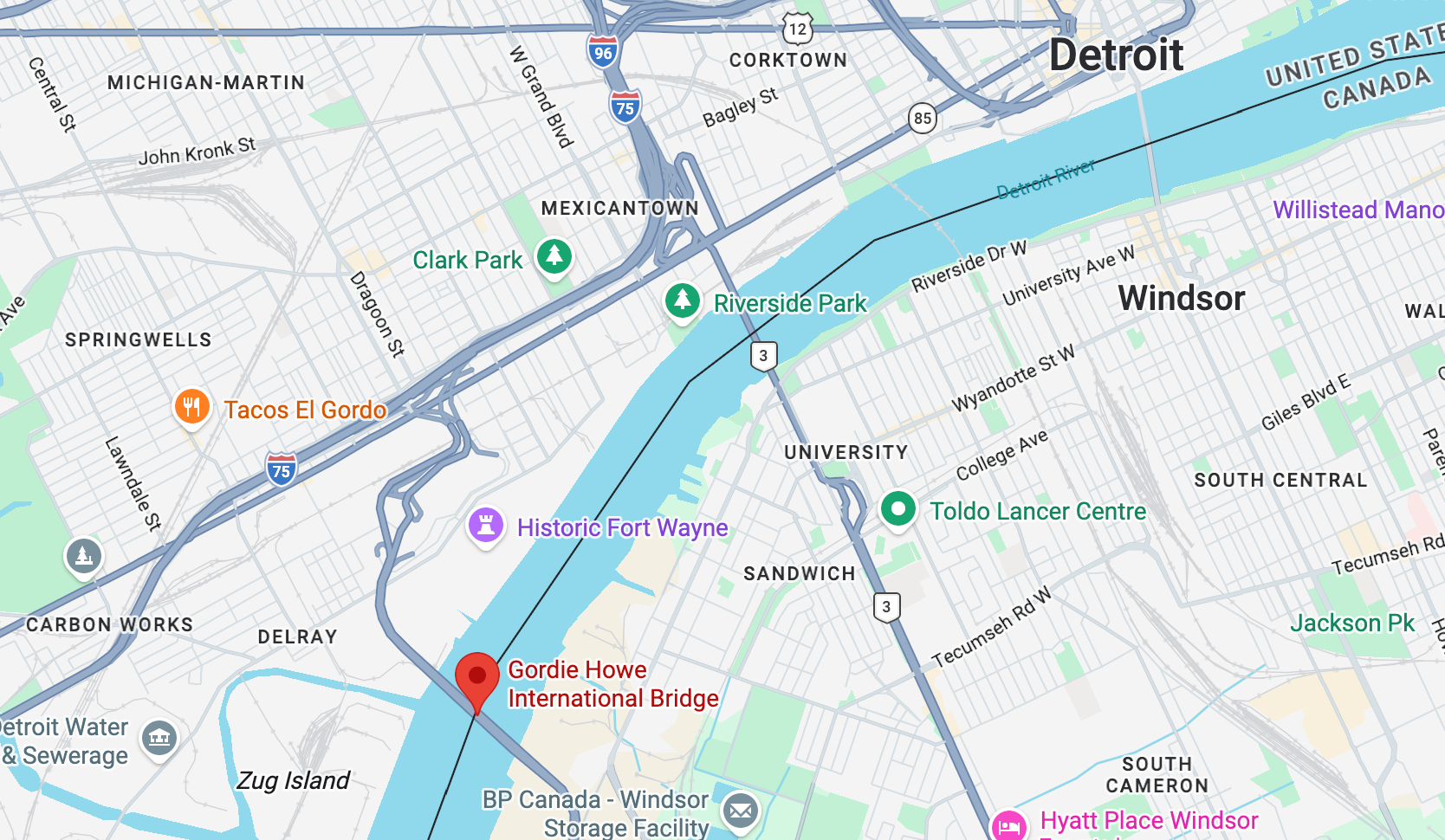

The bypass risk can also change. Even the Ambassador Bridge seems to be facing tougher competition these days, with the Gordie Howe International Bridge opening in 2026 and charging just half the Ambassador Bridge's toll rates. Asking buyers why they choose one bridge over another will help you understand their psychology. Then there's the question of who actually signs the cheque. Finally, do they consider the toll fee to be significant or a rounding error in the grand scheme of things?

There's always a risk of government interference. Governments can easily cap rates, as the Chinese government did for its toll roads during COVID-19. Or require operators to pay a recurring concession fee to the government, taking away some of the economics of the business.

Finally, the strongest toll bridge won't help unless you're actually getting rewarded as an investor. For that, you need dividends on top of well-timed share buybacks. A toll bridge can easily become a value trap if it never shares the economics with minorities.

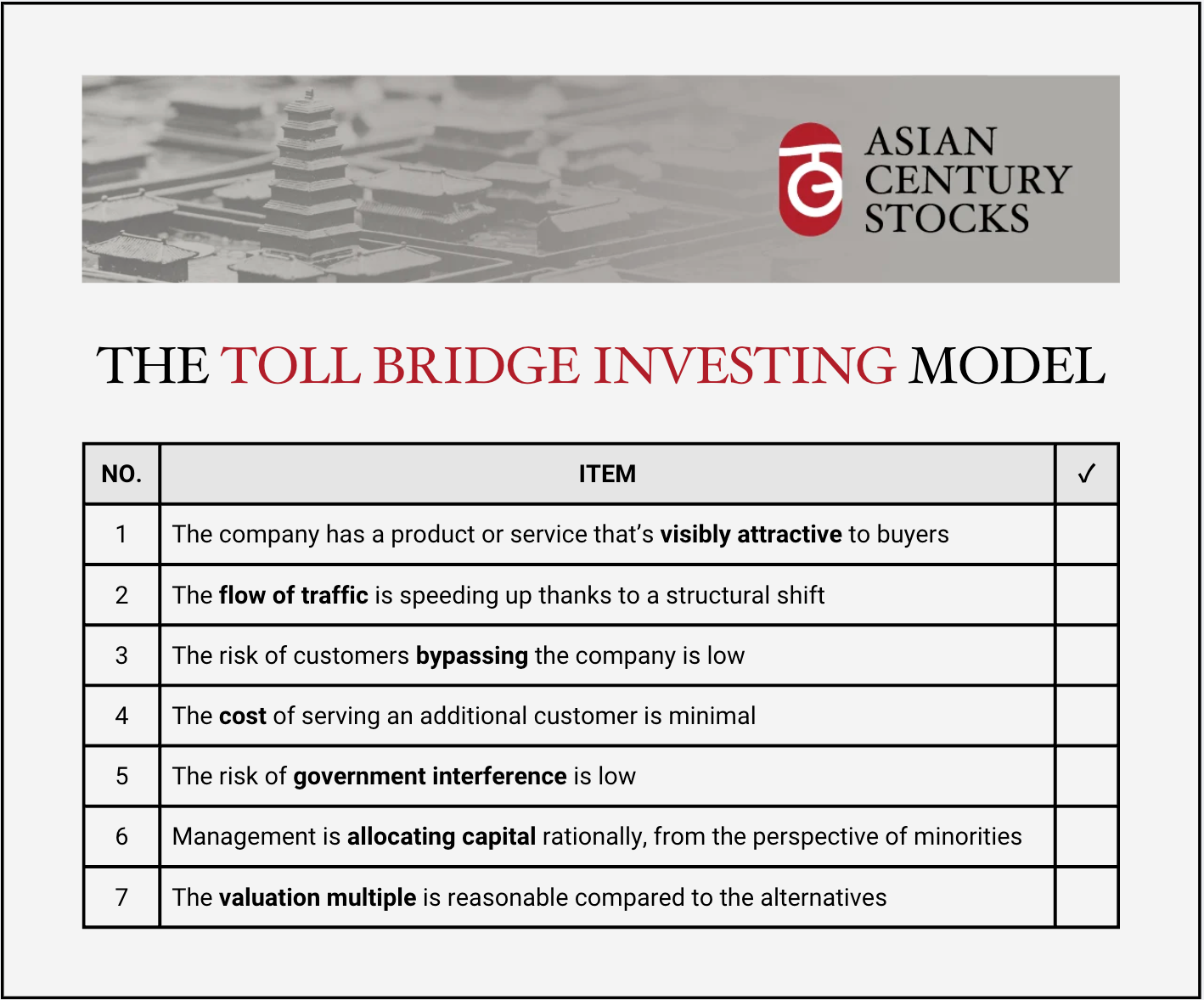

The Toll Bridge Checklist

I've put together a checklist to think through how well a business fits the profile of a toll bridge that can't easily be bypassed:

Conclusion

Matty Moroun purchased the Ambassador Bridge for US$30 million. It's now worth several billion US Dollars. This is a perfect example of a business model: owning a scarce, unavoidable chokepoint and benefiting from an ongoing flow of traffic.

On the other hand, the opening of the new nearby Gordie Howe International Bridge underscores the need to remain vigilant about substitutes that may pop up along the way.

In this post, I've argued that the business model for operating a toll bridge can be generalized to other industries. For example, Texas Pacific Land, Amadeus IT Group, and Hong Kong Exchanges & Clearing carry some of the same characteristics.

I picture that the best investments will be found where there's no viable alternative. Where the costs of serving another customer are practically zero. And where traffic speeds up due to a technological shift that has made the destination much more attractive. Where the government is permissive. And where management acts in the best interests of all shareholders.

If we find such a business, we might end up with a long-term winner.