Five Companies on my Radar

Link REIT + four more

Hi! Welcome to a subscriber-only edition of Asian Century Stocks – a newsletter about Asian value stocks. For a complete list of all previous posts, check out the Table of Contents.

I spent much of the past week moving houses, so the deep dive that I hoped to present to you is not as polished as I had originally hoped for.

Instead, I've decided to give you a rundown of the five companies that are currently at the top of my watchlist.

Link REIT (823 HK)

The first one is a real estate investment trust that I originally wrote about in early 2025: Link REIT (832 HK — US$13 billion).

A friend of the publication over at Smartkarma made the case for the REIT a few days ago. In short, it owns 130 retail properties in Hong Kong, 12 in Mainland China, and another 12 overseas. Its assets are mostly neighbourhood malls, with a large exposure to tenants providing daily services, including grocery stores, wet markets, restaurants, parking garages, etc.

The REIT is unusual in that it's internally managed. Unlike most other REITs, it doesn't have a sponsor injecting assets into it. Instead, it was created when the Hong Kong government decided to carve out all public housing retail properties into a single entity. The malls are truly unique, interacting with 2 million Hong Kong residents daily.

As I explained in my original deep dive, Link's distribution per share track record was very impressive. From its IPO in 2005 to the COVID-19 pandemic, Link's distribution per share rose at a 10% compound annual growth rate, thanks in large part to ongoing asset enhancement initiatives.

However, in the late 2010s, its growth increasingly relied on debt. It was then hurt by Hong Kong's 2019 pro-democracy protests, then COVID-19, and then the 2020 National Security Law, which caused 4% of the population to move overseas. In addition, it faced headwinds from a crackdown on daigou purchasing agents, which led to a decline in the number of Mainland shoppers in Hong Kong. Finally, Link has been hurt by the success of e-commerce companies like Taobao and Pinduoduo.

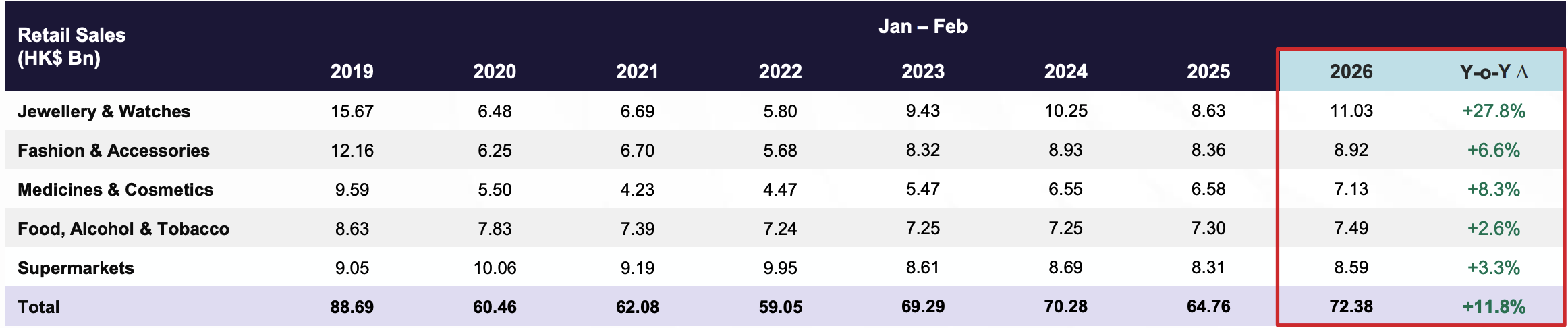

However, positive news is starting to emerge. First, Hong Kong's retail sales has surprised to the upside this year, including in the key supermarkets category:

Second, supermarket chain Wellcome recently reported positive growth in Hong Kong food sales in the first quarter of 2026. Meanwhile, 7-Eleven Hong Kong reported like-for-like growth of +3% in the same quarter.

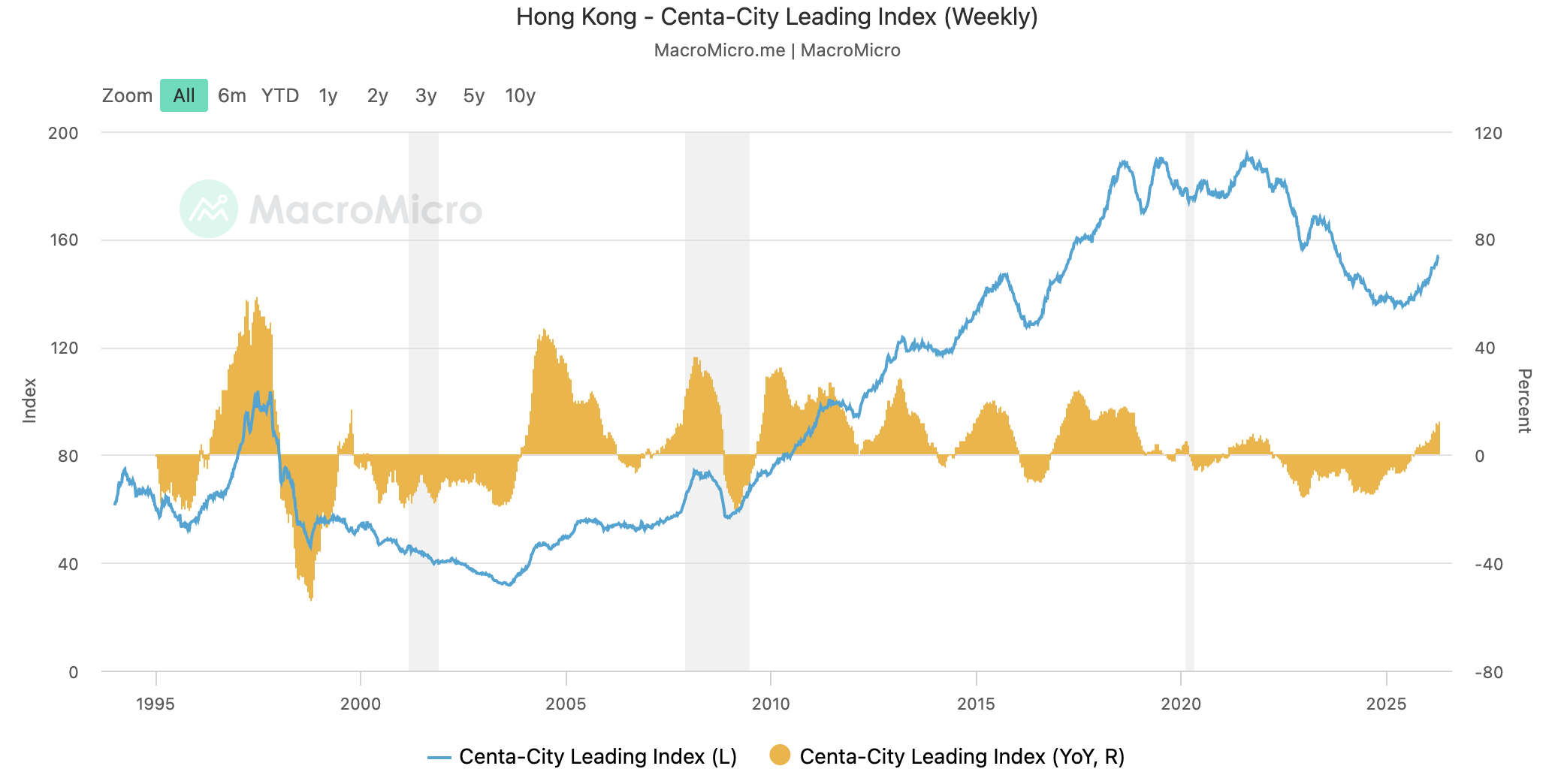

Third, Hong Kong's residential property market is finally recovering:

That's perhaps thanks to Hong Kong's Interbank Offered Rate halving from 5.0% at the peak in 2023 to just 2.5% today.

Fourth, we've recently had a shift in management. CEO George Hongchoy retired in late 2025. I think he was behind Link's aggressive overseas expansion. Many of the properties purchased in the UK and Australia were transacted at record-low cap rates and caused Link REIT to accumulate debt. The 2023 rights issue diluted minorities. So while George has a strong reputation, it seems Link's capital allocation deteriorated in the late 2010s.

The new interim CEOs, John Saunders and Kok-Siong Ng, both come from investment management and finance backgrounds. And it seems like they understand capital allocation.

Since they took over, we've seen a large number of positive news stories out of Link:

- The divestment of Thomson Plaza in Singapore for SG$250 million at 1.2x book value — demonstrating that many of its properties can be realized at book value.

- The launch of a HK$200 million cost-saving program, which should help margins from FY2027 onwards.

- Public statements that they'll avoid diworsification (a Peter Lynch term), instead doubling down on community malls and car parks in Hong Kong and other parts of Asia-Pacific — exactly what Link does so well.

- The move to an asset-light fund management model, allowing Link to earn management fees without the need to deploy capital. They're essentially following the CapitaLand playbook. On LinkedIn, Link now calls itself Link Asset Management — probably a sign of what's coming.

While the REIT is now focused on paying down debt, share buybacks will probably be back on the table soon. The new management team has said that if their own stock yields, say, 7%, it will be difficult to justify acquisitions at cap rates much below that. This type of mindset is rare in Asia and should be encouraged.

Finally, Link is likely to be included in the Hong Kong Connect program as early as the second half of 2026, allowing Mainland Chinese to invest in the company. On the Mainland, retail REITs typically trade at 3-5%.

Link REIT itself trades at a headline dividend yield of 6.5%. The Price/Book ratio is currently 0.65x, below the historical multiple of 1.0x. Pre-COVID, Link consistently traded at a yield below 5%.

Finally, I note that in January 2026, non-executive director Keith Griffiths purchased US$375,000 worth of Link shares. Not a huge amount, but it coincided with the shift to a new management team.

More details:

- The 16 March 2026 operational update

- The 20 November 2025 interim report presentation

The rest of this post covers four more names. Subscribe to unlock:

Nitori (9843 JP)