Interview: Ruchir Desai

From Asia Frontier Capital

Disclaimer: Asian Century Stocks uses information sources believed to be reliable, but their accuracy cannot be guaranteed. The information contained in this publication is not intended to constitute individual investment advice and is not designed to meet your personal financial situation. The opinions expressed in such publications are those of the publisher and are subject to change without notice. You are advised to discuss your investment options with your financial advisers. Consult your financial adviser to understand whether any investment is suitable for your specific needs. I may, from time to time, have positions in the securities covered in the articles on this website. This is not a recommendation to buy or sell stocks.

1. Hi Ruchir! Thanks for doing this interview. Can you tell us a bit about yourself and your journey to managing the AFC Asia Frontier Fund?

Hi Michael, it is very nice speaking with you. I have been with Asia Frontier Capital since its inception in June 2013, managing our AFC Asia Frontier Fund alongside our Founder and CEO, Thomas Hugger.

I have been in Hong Kong for almost 15 years. I arrived in August 2011 to study for my MBA in Finance at the Chinese University of Hong Kong. After my MBA, I joined Thomas at Asia Frontier Capital because frontier markets like Bangladesh, Pakistan, Sri Lanka, Kazakhstan, and Uzbekistan really excite me. Not only do I get to learn more about various companies and industries, but I also gain a good grasp of the region's macroeconomic and geopolitical trends.

As part of managing our AFC Asia Frontier Fund, I cover markets like Bangladesh, Georgia, Jordan, Kazakhstan, Oman, Pakistan, Sri Lanka, and Vietnam, besides also broadly looking at Iraq and Uzbekistan since we also have our AFC Iraq Fund and AFC Uzbekistan Fund.

Prior to arriving in Hong Kong, I was based in Mumbai, where I am originally from and worked as a sell-side research analyst covering Indian software companies and I also worked at a private equity firm making investments in business process outsourcing companies.

2. Why do you think investors should pay attention to frontier markets, as opposed to investing in, say, the United States or Europe?

That is a great question. The argument for investing in frontier markets is not that an investor should avoid investing in the U.S., Europe, or other developed markets, but rather that frontier markets offer a very good diversification tool.

For example, our AFC Asia Frontier Fund has a low correlation of 0.50 with the MSCI World Index since the fund’s inception. Furthermore, individually, many of our markets have very low correlations with the MSCI World Index – Iraq has a negative correlation of -0.09, while Bangladesh’s correlation is only 0.04. Hence, in our country universe, what happens in Vietnam does not impact Bangladesh, and what happens in Pakistan does not impact Sri Lanka.

In addition to this, the annualized volatility of our AFC Asia Frontier Fund is a low 10.6% since the inception of the fund. This is also low compared to the annualized volatility of 13.6% for the MSCI World Index and 16.7% for the MSCI Emerging Markets Index.

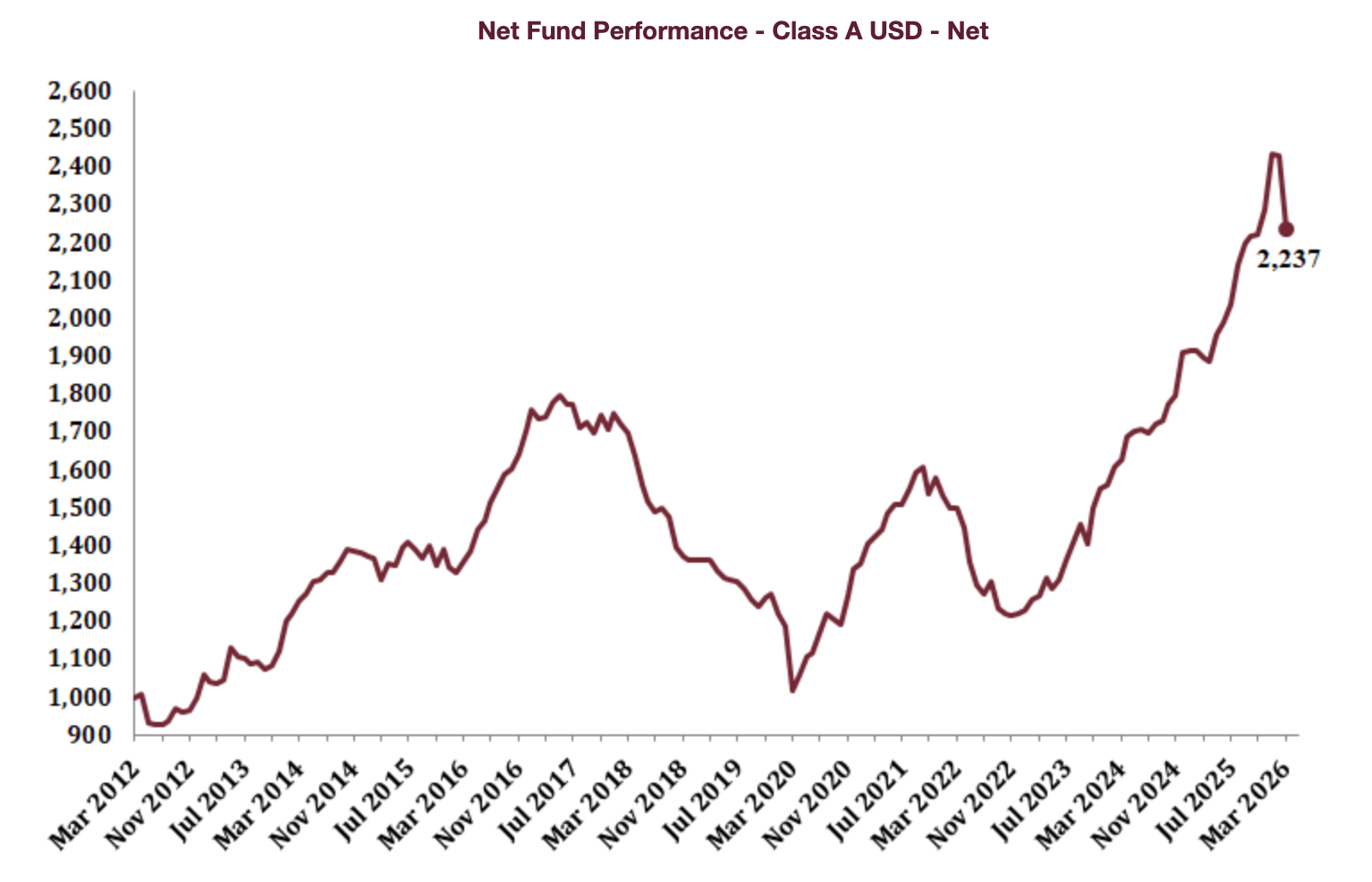

Therefore, frontier markets and our AFC Asia Frontier Fund offer both solid return and sound diversification for any sophisticated investor. The annualized total USD return in the last three years for the AFC Asia Frontier Fund is +20.9%.

3. What are your biggest insights from all these years of investing in Asian frontier markets? What advice would you give to a younger investor who’s just started out picking stocks in frontier markets?

I think the two major insights about investing in Asian frontier markets are that there are many large, well-run companies with sound fundamentals, which are completely ignored compared to large companies in China, India, or Thailand. This gives investors an opportunity to generate an outsized long-term return in Asian frontier markets.

The other key insight especially which I have noticed in the last five or six years, is that any major market correction because of any macroeconomic or geopolitical events is an excellent buying opportunity as companies in Asian frontier countries are used to operating in a challenging environment while the countries itself are very resilient and stock markets in our universe usually bounce back in a very strong way post any market correction.

Hence, I believe that when there is a lot of fear in our markets, it is an excellent buying opportunity – the pandemic in 2022 and the war in Ukraine in 2022 were fantastic buying opportunities, as returns for our AFC Asia Frontier Fund post both events were greater than 20%.

4. How do you think about FX, given that many of the companies you invest in earn revenue in local currencies? What are the metrics you look at to become comfortable with a currency, and how does FX affect the stocks you ultimately pick?

Since it is sometimes not possible or too expensive to hedge currency risk, we begin our investment process with a top-down approach to get our country’s allocation right. We give countries with a stable or improving macroeconomic position a higher weight, and we give countries with a weak or deteriorating macroeconomic position a lower or no weight. In this, we can reduce the risk of currency losses. In the past, we have had very low weightings to Pakistan and Sri Lanka in 2022 and 2023 due to a weak macroeconomic environment, which led to currency weakness.

Since getting the top-down country allocation right, we look at key indicators such as foreign exchange reserves, the current account balance and its impact on currency movements, a government’s budget deficit, inflation, and the interest rate cycle.

5. What are some of the secular trends in frontier markets that you like to bet on right now? And how do you typically express those bets?

Our Asian frontier markets have a lot of structural trends going for them. Our universe of countries has a combined population of almost 770 million people who are young. The median age in our country universe is only 27, and this sizeable young population is growing.

A young, growing population is a very exciting trend for Asian frontier markets as it offers long-term secular growth trends for various industries like consumer goods, financial services, telecommunication, and also for infrastructure development, as the increasing urbanization process in our universe drives demand for better and more modern infrastructure.

In addition to a young, growing population with rising disposable incomes, Asian frontier countries are also benefiting immensely from the global shift in supply chains. The two major beneficiaries of this trend are Bangladesh and Vietnam.

Bangladesh is now the second-largest garment exporter globally, after China, as many garment manufacturers have moved production there due to lower costs and access to a well-established garment export ecosystem.

Vietnam has been one of the key beneficiaries of the trade and geopolitical tensions between China and the U.S. For example, Vietnam’s exports to the U.S. have tripled in size from USD 42 billion in 2017 to USD 153 billion in 2025.

6. What markets do you invest in at AFC? And where do you see the greatest opportunities right now?

Our AFC Asia Frontier Fund is currently invested in 15 countries, with the top 5 country allocation being Pakistan 13.9%, Uzbekistan 13.0%, Sri Lanka 12.6%, Bangladesh 10.6%, and Iraq 9.9%.

Broadly, besides the very favorable demographic backdrop in our markets and many of our countries benefitting from the global supply chain relocation, valuations in our markets are extremely attractive. Bangladesh and Pakistan trade at a P/E ratio of 8.2x and 8.9x, respectively, while our AFC Asia Frontier Fund trades at a P/E ratio of only 7.3x, which is close to its all-time low, while the fund’s NAV is at its all-time high.

More importantly, our markets faced a challenging period between 2017-2023 because of macroeconomic and political headwinds, however all our countries are now on a reform path leading to both political stability and economic momentum which has led to robust returns for the AFC Asia Frontier Fund and we expect this momentum to continue as the governments in our country universe are very focused on achieving stable long term economic growth backed by political stability.

7. Let’s talk about Bangladesh. Sheikh Hasina was ousted in 2024, and the stock market took a beating. What’s your outlook today, and what do you think it will take for stocks to rerate?

Bangladesh is currently one of my top country picks. The country’s economy and stock market have not delivered performance over the last five to six years due to macroeconomic or political issues that have hampered any recovery.

However, valuations in Bangladesh are now at multi-year lows with the index trading at a P/E of only 8.2x compared to 16.0x in 2018/2019. I believe all the important catalysts are in place to drive a sustained re-rating of stocks on the Dhaka Stock Exchange.

Macroeconomic indicators have improved substantially in the last two years in the form of higher foreign exchange reserves, a more stable current account and increasing exports and worker remittance as the Bangladeshi Taka was devalued in 2023 and 2024 taking the currency to a more realistic value.

Much more importantly, parliamentary elections were held in February 2026, leading to the formation of a stable and majority government led by the Bangladesh Nationalist Party (BNP).

In my view, Bangladesh now has both the macro and political platform set for a period of higher economic growth and a strong stock market returns which will be led by both valuation re-rating upwards as well an earnings growth recovery.

8. How has the political situation in Sri Lanka developed since the 2022 debt default? Is the market now investable, in your view?

Sri Lanka, according to me, is now a structural growth story as it has overcome immense political and economic challenges since 2022. Sri Lanka now has a significantly stronger political platform to drive growth. Parliamentary elections were held in November 2024, leading to a sweeping majority victory for President Anura Dissanayake’s party.

This was an inflection point for the country as it now has political stability after many years, and the new government is extremely committed to reforms and not repeating the mistakes of the past.

On the economic front as well, Sri Lanka has made a roaring recovery with GDP growth in 2024 and 2025 coming in ahead of expectations at +5%. Furthermore, the tourism industry is booming, and Sri Lanka recorded its all-time high tourist arrivals of 2.5 million in 2025, and there is a huge scope to grow this number much more, given the tourist attractions in Sri Lanka.

In the last three years, the Colombo All Share Index has generated a total return of approximately +180% in USD terms. Hence, Sri Lanka is not only investable, but its stock market is thriving.

9. At the FatAlpha Value conference in Vietnam, you pitched Pakistani cement company Lucky Cement. What’s the story there, and why do you think it’s attractive at this point in time?

Lucky Cement, in my view, is one of the best ways to play the Pakistan story. Lucky Cement is leveraged to the Pakistani economy in various ways. It is the largest and lowest cost cement producer in Pakistan, it has a joint venture with Kia Motors to assemble and distribute passenger cars in Pakistan, it also has a joint venture with Samsung to assemble smartphones, and it has investments in the chemical and power sector in the country.

Lucky Cement is therefore well-positioned to benefit from greater demand for construction materials, automobiles, and power in the country, as a large and young population drives demand for these products and services. Furthermore, Lucky Cement also has a very profitable cement operation in Iraq and D.R. Congo, where it has, in fact, increased capacity in both countries in the last year.

In my view, this diversified nature of Lucky Cement’s business not only offers a leveraged play on Pakistan’s economy but also offers stable earnings in the event of a slowdown in one of the business segments.

Valuation wise I still see a lot of upside for Lucky Cement as the stock trades at P/E ratio of only 5.2x and its cement business trades at an EV/Ton of USD 44/Ton compared to regional peers who trade at and EV/Ton of USD 175-200/Ton.

Lucky Cement has been a multi-bagger for the AFC Asia Frontier Fund, returning almost +460% in USD terms since 31st March 2023.

This stock pick is also an example of the long-term view we take in our stock picking, letting the story and returns play out.

10. Thanks for doing this, Ruchir! Where can people go to learn more about the fund and the work you do at Asia Frontier Capital?

We have a very informative website, which has information on our AFC Funds, our markets, and our excellent monthly newsletter, which your readers can subscribe to on our website. Our website address is www.asiafrontiercapital.com.

Your readers can also reach me at rd@asiafrontiercapital.com.