Book review: The Money Miners

A review of Trevor Sykes book about Australia's 1968-70 mining bubble. Estimated reading time: 28 minutes

Disclaimer: Asian Century Stocks uses information sources believed to be reliable, but their accuracy cannot be guaranteed. The information contained in this publication is not intended to constitute individual investment advice and is not designed to meet your personal financial situation. The opinions expressed in such publications are those of the publisher and are subject to change without notice. You are advised to discuss your investment options with your financial advisers. Consult your financial adviser to understand whether any investment is suitable for your specific needs. I may, from time to time, have positions in the securities covered in the articles on this website. This is not a recommendation to buy or sell stocks.

Summary

- I read Trevor Sykes book The Money Miners recently. It’s a book about Australia’s 1968-70 speculative mining bubble. Consider it a historical reference book about a bygone era.

- I realize this is a wonky subject. But then again, there is almost nothing out there in the public domain about past mining stock bubbles. So consider this a rare glimpse into an obscure topic.

- The book discusses a number of key events during the boom and subsequent bust, including how the tungsten mine of Attunga were tampered with, the nickel find that caused the share price of early-stage exploration company Poseidon to rise 350x in just six months, how uranium miner Queensland Mining deceived the market and the rise and fall of investment house Mineral Securities.

- If there’s any lesson from the bubble, it’s the importance of not getting swept away by the crowd and being aligned with insiders and promoters, the difficulty of valuing mineral resources and finally, being careful of companies that are reliant on markets for their funding.

Bronte Capital’s John Hempton has said that one of his favorite books is The Money Miners by Trevor Sykes.

That book is a first-hand account of the great Australian mining boom from the late 1960s to 1970. At that time, speculative fever took over the nation. Many hundreds of millions dollar were gained and subsequently lost.

I took the book with me on my summer break in Europe. And here are my key takeaways from the book - my attempt to distil the knowledge into a single post. Enjoy!

TABLE OF CONTENTS

1. A short history of mining

2. First discovery of nickel

3. Mine salting at Attunga

4. Speculation heats up

5. Poseidon

6. The crescendo

7. Uranium in Nabarlek

8. The collapse of Mineral Securities

9. The aftermath

10. Conclusion1. A short history of mining

Australia’s mining industry began with the discovery of gold close to Adelaide and Melbourne in the late 1840s. People from around the world flocked to Australia, hoping to strike gold and get rich. You could say that the nation was almost built on the back of the mining industry.

By the 1850s, 40% of the world’s gold came from Australia.

In the subsequent decades, mining became increasingly complex. A greater variety of resources were mined and at increasing depths. This shift necessitated the purchase of machinery and the construction of infrastructure. And to fund that spending, mining companies were formed. They issued capital and the shares were then bought and sold in local exchanges in mining towns across Australia.

For example, in 1883, seven men got together to fund a mine in Broken Hill in New South Wales. There was considerable excitement about the discovery of silver and lead in the area. Famously, one of the men lost his 1/14th share of the Broken Hill mine in a poker game to a stranger passing by. The Broken Hill mine later became known as BHP, which is now one of Australia’s largest companies. The shares lost in the poker game are now worth about US$9 billion.

The second gold rush started in 1893 when gold was found in Kalgoorlie, Western Australia, roughly 600 kilometers west of Perth. This time, the boom attracted not only British and Chinese, but also low wage workers from Italy and the Balkans.

During the 1890s gold rush, mines were increasingly located deep underground and owned by corporations. For that reason, miners were less likely to be prospectors themselves, but rather low-wage workers from, say, Italy and the Balkans just trying to eke out a living.

The industry benefitted greatly from the 1898 construction of a water pipeline from Perth to Kalgoorlie. A series of pumping stations helped get the water uphill into the desert, alleviating the water shortages that had beset early Kalgoorlie mines.

There was a short gold rush during the Great Depression when Australia’s currency was taken off the gold standard in 1929 and devalued against the British pound. Gold prices rose and the mining industry saw a temporary resurgence.

Another key event in the industry was when prospector Lang Hancock flew his aircraft across the desert of Western Australia in 1953. He suddenly encountered a severe storm and was forced to descend below the clouds. On his descent, he happened to see a massive wall of iron ore stretching as far as the eye could see.

Hancock’s discovery would become the Pilbara iron ore deposit, found to have 20 billion tons of high-grade iron ore.

Hancock was smart enough to sign a royalty deal with Rio Tinto that gave him a piece of the profits - an income stream that’s lasted to this day. His daughter Gina Reinhart now has a net worth of US$31 billion, now one of the richest women in the world.

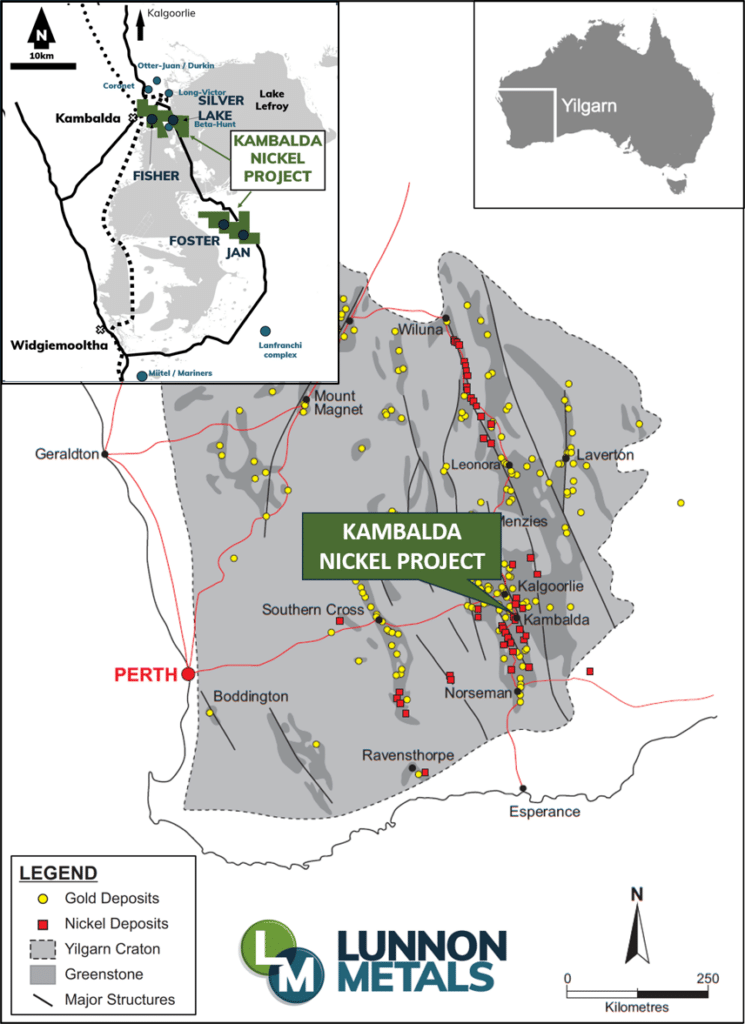

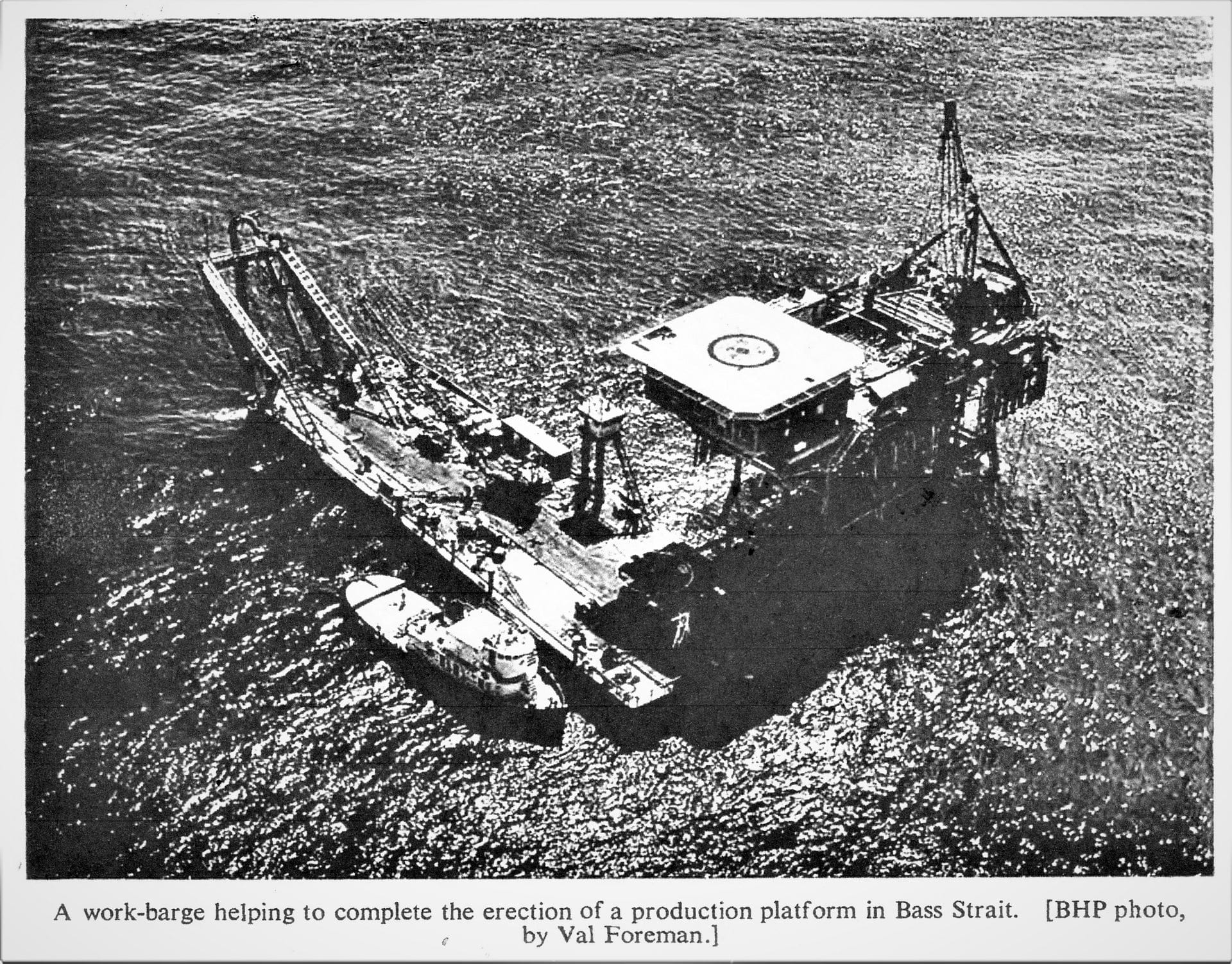

In the 1960s, the mineral sands industry grew rapidly. BHP found oil together with Esso in the Bass Strait in 1966. And then, a small company called Western Mining Corporation struck nickel on the shores of Lake Lefroy in Kambalda - Australia’s first-ever discovery of nickel.

The boom in the nickel industry is the subject of Trevor Sykes book. It sparked one of the greatest financial bubbles in history, or certainly in Australia.

2. First discovery of nickel

“Nothing in the financial world ignites public imagination more fiercely than the sudden discovery of a precious new commodity.”

Western Mining Corporation was formed during in 1933, focusing primarily on gold during the depths of the Great Depression. But in the subsequent decades, its fortunes fluctuated and it became known as the company “going nowhere”.

In the 1950s, a geologist at Western Mining started taking samples down south from Kalgoorlie in an area called Kambalda.

The samples from Kambalda were not tested at the time. But ten years later, one of them was sent in for “assay” - the testing of an ore to see how much metal it contains - and found to contain 0.7% nickel. This was a high enough grade to make a mine economically viable.

Western Mining Corporation announced its nickel discovery in 1966 and began serious exploration. It was to become Australia’s first-ever nickel mine.

The timing of the discovery was fortuitous. Nickel had initially been used for tableware, but later on, other uses were found in stainless steel, aerospace, and the munitions industries. Importantly, this was the time of the Vietnam War, which had sparked demand for nickel. Meanwhile, the supply of nickel had been restricted due to the under-capacity of existing mines. This supply and demand picture created the perfect conditions for a sustained rally in the price of nickel.

3. Mine salting at Attunga

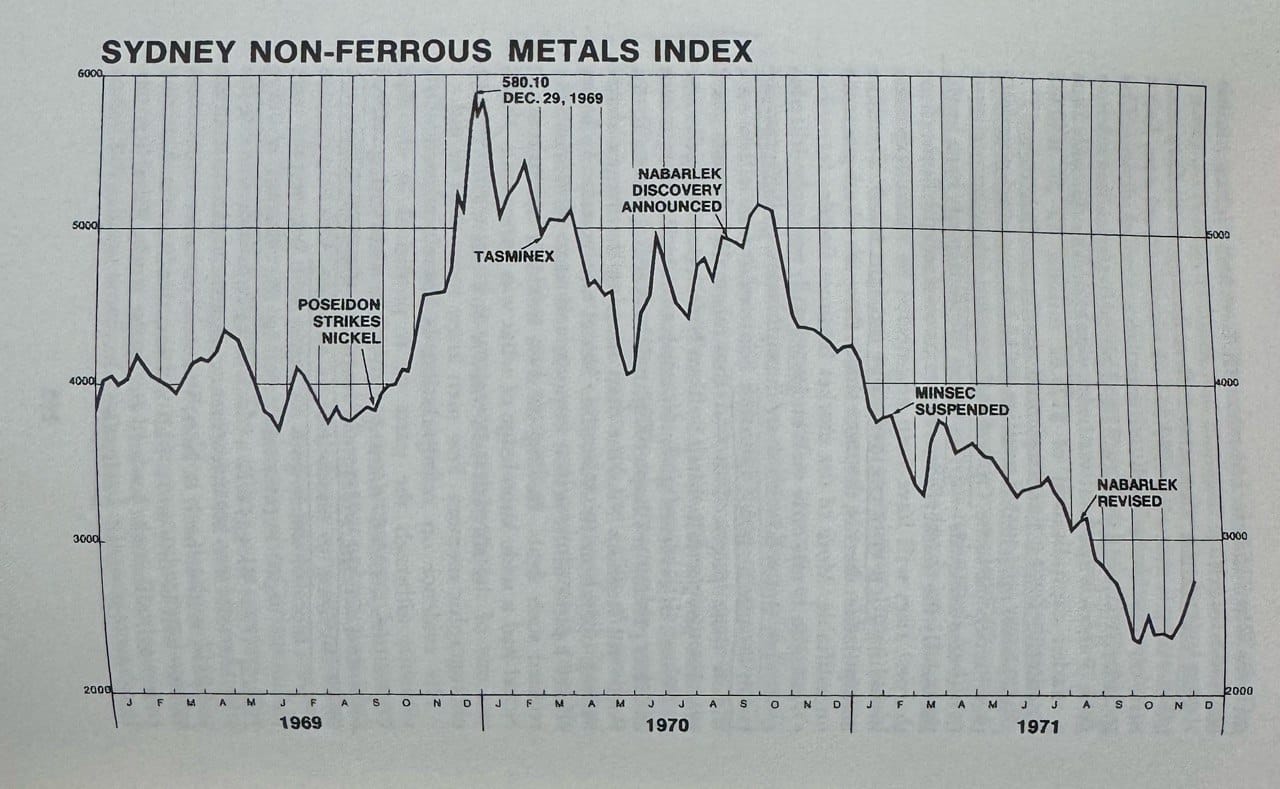

The mining index started rallying in 1968, gaining 70% in a single year:

The economy was stronger than ever, with low unemployment and optimism in the air.

It was at this time that a sleepy Tasmanian tin miner called Endurance Mining caught the attention of speculators across the nation. A couple of Sydney entrepreneurs took over the company and started looking for ways to make money.

In New South Wales, a geologist had just taken a sample from an area called Attunga and sent it in for assay. The results were promising, with an average grade of 1.44% tungsten oxide over a total depth of 600 feet. Endurance Mining took notice and purchased an option on Attunga.

The market became excited about the prospects of a potential tungsten mine. Endurance’s share price rallied from AU$1 to AU$10 in a short period of time, with the market cap hitting AU$15 million at the peak. The turnover of the stock was enormous, with small retail investors trying to get in on the deal.

In February 1969, the company’s geologists confirmed 500,000 tons of tungsten ore with an average grade of 1.4%. One of the directors said how promising the discovery was:

“We don’t need a geologist to prove there’s a million tons of ore under this hill - you can see it.”

Endurance then acquired the whole of Attunga Mining’s issued capital through a merger of equals.

But something was afoot. Right after publishing the February assay result, directeors started selling shares worth more than AU$5 million AU$75 million in today’s dollars. This marked the peak in Endurance’s share price.

The problem with the assay was that the positioning of the drill holes and their angles created a false picture of the ore body. In other words, the data didn’t provide an accurate picture of the discovery.

By June 1969, when the share price had already dropped 90%, the news hit the market. Three separate laboratories confirmed that the grade had been grossly exaggerated. Instead of 500,000 tons, Attunga only had 13,600 tons of tungsten ore, with grades ranging from 2.2% to 3.0%.

It later turned out that someone on the inside had tampered with the February assay. The person had added tungsten to the sample in a practice called “mine salting”, which involves sprinkling metal over an orebody to make the grade seem higher than it really was.

So Attunga proved to be a big scam, one of many that would plague that bull market of the late 1960s.

4. Speculation heats up

BHP made further discoveries in 1968, and its share price almost doubled that year, bringing the rest of the oil board with it. Investors became enthusiastic about oil stocks.

Dr Lewis Weeks - the discoverer of the Bass Strait oil field - estimated that Australia’s oil reserves amounted to 2,500 million barrels of oil, 50% more than previously thought.

The news of BHP’s oil find caused excitement in the market. Soon after BHP’s rally in 1968, dozens of blank check companies were formed to explore for oil & gas. These would merge with actual exploration companies and enable vendors to sell their shares to the market.

It was during this time that speculators became enamored with IPOs. They would buy shares in floats and then sell shares quickly after listing. Many of them would pop upon listing, creating significant gains for the ones participating. Among retail investors, there was intense competition to be on a broker’s “float list” — getting the first call to buy shares. In reality, however, the largest quantities of shares tended to be reserved by the brokers’ own families, employees, and friends.

The free market price of nickel started rising from early 1969 onwards, from £1,500 per ton in January to £2,000 by March.

After a nickel miner strike in Canada, the free market price skyrocketed to £4,250 per tonne and eventually £7,000. The nickel rally was on.

5. Poseidon

“It’s easy. You can breathe, can’t you - you can make money.”

The company that came to be associated with the nickel boom the most was a small Kambalda miner called Poseidon.

The name came from a racehorse that might have been the best three-year-old to ever race in Australia - winning three separate competitions in a single year in 1906. Later on, when a group of Italian miners worked on a claim in Tennant Creek in the Northern Territory, they named it “Poseidon” in memory of the racehorse.

Poseidon was initially trying to extract wolfram in a Northern Territory mine. But by 1966, it was destitute, losing tens of thousands of dollars yearly. At that time, a man called Boris Ganke offered to buy 70,000 shares of Poseidon at AU$2.5-3.0 cents each, ending up with 100,000 shares.

Another mining engineer with the name of Norm Shierlaw formed a syndicate that separately bought 400,000 shares in Poseidon. Shierlaw was a veteran prospector who had traded on the Kalgoorlie Stock Exchange back in the day.

He and Ganke became bedfellows in this practically worthless stock with only AU$200,000 in the bank.

Poseidon’s fortunes changed when it hired full-time prospector Ken Shirley - an old friend of Norm Shierlaw. Ken lived in a caravan, living a lifestyle of moving around the bush to make new discoveries. His travels took him to Mount Windarra north of Kalgoorlie. He discovered minerals and pegged 41 claims along an iron formation stretching 11 kilometers.

In April 1969, Shirley sent in samples from Mount Windarra for assay and found 0.5% copper and 0.7% nickel together with associated platinum. The consulting geologists who analyzed the sample called it “very encouraging” and “intensely interesting”.

Rumors started spreading about Windarra. The owner of a butcher shop in a nearby town heard that the guys at Poseidon was up to something. And so he bought 25,000 shares in August for himself and his family.

Shortly thereafter, Poseidon started percussion drilling another kilometer south of Mount Windarra. The geologists saw a change in the color of the sludge coming out of the hole. 30 of the 36 samples contained more than 1% nickel.

They kept these facts to themselves, but somehow the news found their way to the stock exchanges, with the share price slowly creeping upwards from AU$1.2 to AU$1.5. When asked by the stock exchange why the stock had risen, the board said that they were “unable to explain the sharp increase in the price of the shares”.

But secretly, Shierlaw was scooping up Poseidon shares himself, at times soaking up half of the turnover at the Adelaide Stock Exchange. Meanwhile, the Chairman of the Perth Stock Exchange heard about the rumors and bought 2,100 shares for himself. At this time, the price had already risen to AU$2.0 per share.

On 29 September, Poseidon’s directors made their first public announcement about the discovery at Windarra. It said that the second drill hole had encountered nickel and copper but didn’t mention anything about the grade.

Just a few days after, on 1 October, they issued a more comprehensive statement showing 3.6% nickel at depths of 145-185 feet. This meant that Poseidon had struck nickel - the biggest nickel discovery in the history of Australia.

The announcement sparked a massive rally in the price of Poseidon. On 2 October, speculators flooded the Sydney Stock Exchange building after hearing about Poseidon in the press. Many of them were unable to reach the trading floor. On that day, on of the boards collapsed but prices continued to be updated on it will the staff refastened the ropes. Speculators didn’t want to miss an opportunity to buy.

In Melbourne, the trading floor was packed as well. Speculators had to bring binoculars to be able to see what prices were quoted. Some allegedly started using walkie-talkies to relay information to friends in nearby telephone booths from which orders could be made.

With some investors left out of the Poseidon rally, they scrambled to find “the next Poseidon” by looking at the companies that owned claims in nearby areas. Such claims are acquired through so-called pegging when physical pegs mark out the boundaries of a new mining lease. Once pegged, the owner must make minimum capital expenditures to maintain it.

Brokers pushed the theory of the so-called “nickel shield”: that the entire area is full of nickel, so whoever managed to get claims before others could potentially get rich.

The rush for leases around Windarra caused prospectors to peg new claims over others. Some were pulling out their rivals claim pegs and throwing them away. When Poseidon had announced its drill result there had only been three mining groups in the district. One month later, there were 20.

For example, Victoria-based miner Bendigo acquired mineral tenements adjoining Poseidon. Once the news hit the market, its share price nearly doubled from AU$90 cents to AU$1.6. Insiders quickly flooded the market with a block of shares priced at AU$1.5 each. Stories like these were commonplace.

To separate fact from fiction, investors started touring mines through a new charter aircraft industry. For AU$1,975 or around AU$30,000 in today’s money, companies like Bizjet would take you on a five-day tour of selected mine sites across the country. Flying over a new discovery was often enough to get a glimpse of potential mineralization. And it was faster and more comfortable than travelling across the bush.

You also saw the rise of newsletters like “Mineral Exploration in Western Australia”, which offered paid subscribers access to on-the-ground research on new mineral discoveries. The newsletter cost AU$1,000 per year, about AU$15,000 in today’s money. The authors would fly over the mines of listed companies or go look for black sludge coming from drill holes.

By mid-October, Poseidon’s share price had reached AU$23, up almost a thousand times since Boris Ganke initially bought his shares. The next morning, in early trading, one operator shouted across the floor: “Buy Poseidon at AU$30”. And suddenly, the price shot up to AU$31, up another eight dollars above its previous price.

The volume of trading in October 1969 was immense, reaching 30 million shares per day, causing the Sydney Stock Exchange computer to break down. This was a massive number. Even the much larger New York Stock Exchange didn’t handle more than 10 million shares per day at the time.

The magazine cover indicator also reared its ugly head, with The Economist writing a headline about the mining boom that said: “Australia: a Beaut of a Boom”.

Part of the contributing factor to the boom was the rise in margin trading. It was made worse by the fact that there was considerable time before a cash settlement would occur. In the intervening period, the speculator essentially had more margin to play with before he needed to part with his cash, thus multiplying the leverage.

On 19 November 1969, Poseidon made an announcement confirming the strike length and width of the discovery. But strangely enough, it didn’t give any details about the assays from the drill holes. Despite the lack of information, the market took the report positively, causing Poseidon’s share price to rise further to AU$55.

Broker research departments issued reports, dreaming and imagining what Poseidon could be worth. These valuation exercises went along these lines:

- If the strike length was 1,500 feet, the width was 65 feet, and the depth was 500, that meant a total orebody of 48 million cubic feet, assuming the orebody is a neat rectangular block

- The orebody contained 13 cubic feet to the ton, which meant about three million tons of ore

- With an average grade of 2.0-2.5% nickel, the orebody could contain about 70,000 tons of nickel

- At an average price of AU$5,000 per ton, the orebody could be worth AU$350 milllion

- There will also be costs involved, including for labor, equipment, finance, infrastructure, etc. Say around AU$200 million.

- Over a mine life of 15 years, you could then calculate an income stream over time of the remaining AU$150 million worth and figure out that you could get earnings of AU$10 million per year

- Capitalize that number, and you could have justified a share price of AU$60 for Poseidon. Others, like Panmure Gordon in London, ended up with a value of AU$380/share.

Using a forward P/E multiple against expected earnings from Mount Windarra, the price didn’t seem so high. And speculators therefore felt comfortable bidding up the price to even higher levels.

6. The crescendo

“The rising flurry of new flotations has always been one of the signs of the closing stages of a particular boom market”

The speculation in mining stocks reached a crescendo around Christmas of 1969. Early in the morning each day, investors would line up outside brokerage offices in the hope of being able to put in an order. Phone lines to brokerage offices were overwhelmed and there was almost no way to get through.

At Poseidon’s annual meeting in December 1969, long queues also formed outside the event. When the doors opened, 500 people rushed into the building. But due to a lack of seats, about 200 of them had to stand at the back while the meeting went on.

At the AGM, a discussion started about a potential rights issue to fund future capital expenditures. Instead, a share placement was proposed to a select number of individuals at AU$5 per share - a massive discount to the then-prevailing share price of AU$100 - suggesting severe dilution without raising much capital.

This was a huge problem because Poseidon had struck nickel but not enough capital to actually develop the mine.

A geologist speaking at the AGM mentioned that the zone in which the drilling had taken place indicated four million tons of ore. Participants flooded out of the meeting trying to calculate what 2.4% times 4 million tonnes might imply in terms of nickel resources. Enthusiasm boiled over.

Investors rushed out of the AGM to public telephone booths to call their brokers. At the start of the AGM to the end, the share price ran from AU$112 to AU$130. Once the press caught wind of the story, the price rallied further to AU$185.

No one rang a bell at the top of the market, but some lone voices expressed concern about how far the market had run:

- A London stock broker called R. Davie said that “A lot of Australian stocks, to put it mildly, are highly suspect”.

- Melbourne firm A Holst & Co predicted that in a few years’ time, the majority of present “gambling stocks” would be bitter memories to those who continued to hold them.

In February 1970, Poseidon reached a market capitalization of AU$700 million, or about AU$10 billion in today’s money. This represented about 3x the market cap of the Bank of New South Wales. And one-third the value of BHP, even though Poseidon hadn’t even begun developing any mine.

Right around that time, Poseidon insiders, such as the consulting geologist firm Burrill Investments, began selling their shares in the company.

A geologist told brokerage firm Patrick & Co that he thought the stock was grossly overvalued and that Poseidon was facing very serious water problems, which would cost a fortune to rectify. Following his advice, Patrick advised its clients to start selling the stock.

Poseidon’s stock price peaked at around AU$280 per share. The market was waiting for Poseidon to announce how it would fund the development of its mine in Windarra. Yet nothing was announced. Meanwhile, the share price started declining.

By the end of February, almost all other speculative stocks on the board had also fallen significantly, with some losing half their value.

What led to this sudden change in sentiment?

- A major contributing factor was that nickel prices peaked and started declining from late 1960s onwards. The higher prices would eventually provide an incentive to search for new orebodies. Mines started coming online in a number of new number of new countries. World production of nickel skyrocketed.

- At the tend of 1969, there were 145 mining stocks listed in Sydney, compared with just 86 at the start of the year. And there were another 100 more mining companies queuing up to float and eventually list on the exchange. Supply eventually met the demand for scrip.

- Another factor was higher capital costs as Australian interest rates rose sharply

- Yet another factor was rising inflation as the operating costs of a mine shot up

It didn’t help that Poseidon’s eventual grade was almost half what was originally reported, with the grade falling from 3.6% to 2.4%. Combine that with much lower nickel prices and sharply higher development costs, and you have all the ingredients of a boom turning to bust.

7. Uranium in Nabarlek

“Profit making is neither illegal nor immoral. The means of achieving it can be.”

After falling in the early parts of the 1970s, the non-ferrous metals index finally rebounded temporarily. The Western Australian government imposed a ban on pegging in February 1970 due to excess paperwork, and that ban was finally lifted in June 1970.

Around this time, the mining world was astounded by a statement from the Chairman of Queensland Mines that his company had discovered 55,000 short tons of uranium oxide in Nabarlek in the Northern Territory. This would qualify Nabarlek as the world’s richest deposit of uranium.

The work in Nabarlek began in April 1970, with an airborne survey showing a cluster of strong anomalies. 12 foot trenches were dug, revealing signs of uranium oxide including one area with 72% uranium oxide. This was a phenomenally rich find. But the information was kept secret and not released to the public.

In August, Queensland Mines’ directors visited Nabarlek and were impressed by it. And the share price started creeping up. The Sydney Stock Exchange asked the directors if they knew the reason for the a share price spike. And on 1 September, Queensland Mines replied that they had found reserves of 55,000 short tons of uranium oxide.

The stock moved exponentially higher. From a low of AU$7.2 in August, the share price of Queensland Mines rose to AU$11.2 in early September and then to AU$43 by the end of the month.

The problem was that the 55,000-ton estimate was not based on assays but simply extrapolated from a single sample which happened to have 70% grade uranium oxide. The number would prove to be highly misleading.

Japanese trading companies Mitsui and Mitsubishi did their own surveys and found that Queensland Mining’s estimate was wildly inadequate. Brokers sent their own geologists, too, and couldn’t believe the number reported.

It took an entire year until August 1971 before Queensland Mines admitted that the reserves were not expected to exceed 9,000 tons of ore, 1/6th of that originally estimated. While they knew that the initial estimate was wrong, they had resisted correcting the mistake on the grounds that it would destroy confidence in the company and the prospects of negotiating a sales contract.

As it turns out, the Chairman of Queensland Mines had made AU$290,000 selling shares in the company to the public while those inaccurate numbers remained in the market. In today’s dollars, those profits would be worth around AU$4 million.

8. The collapse of Mineral Securities

“Those who controlled Minsec wrote their own death warrant in classic terms.”

The downfall of Queensland Mining brought down one of the most renowned investment companies of that era: Mineral Securities, also known as “Minsec”. It was formed by geologist Ken McMahon and run by director Tom Nestel. During the bubble, Minsec became the heaviest share trader in the entire country, building a large portfolio of mining shares.

Tom Nestel was a Yugoslav that was widely seen to have a golden touch when it comes to picking stocks. He could be rude at times and didn’t like small talk. But his colleagues respected his abilities.

When Minsec was formed in 1965, it was capitalized with only AU$300,000. However, through trading profits, it amassed an 8 figure portfolio and eventually moved on to acquiring controlling positions in larger mines.

When Poseidon struck nickel in 1969, Minsec was initially short the stock and then flipped long once they realized the extent of their mistake. During the short four months of the rally, Minsec made an AU$12 million profit, and much of it from Poseidon.

However, as the market peaked in February 1970, Minsec had become too big in relation to the market itself, operating with immense leverage. When the market topped, it became almost impossible to find blocks of buyers. Liquidity dried out. Minsec was stuck.

Minsec survived the early 1970s slump. But by mid-year, Tom Nestel became positive and Minsec doubled-down on its holdings, hoping for a rebound. It bought more shares in Poseidon. It also accumulated a large AU$17 million stake in Queensland Mines after the discovery of Nabarlek.

All this buying caused Minsec to run short of cash. It found it difficult to finance its manic pace of buying. Their solution was to take on more debt. The problem was that none of Minsec’s holdings paid any dividends, so it had to finance interest payments by trading profits. The problem was exacerbated by the fact that Minsec borrowed through the money markets, with many of its loans callable at a moment’s notice. The debt kept rising:

As the value of its portfolio began dropping, Minsec became desperate. It sold a stake in mining company Robe River to a fellow brokerage firm, which then resold the stake to Minsec’s own subsidiary. By doing so it essentially marked up value of its stake, creating a fictious profit in the process. Minsec also directed its mutual funds to buy shares in Minsec itself. But it was too late.

In late 1970, news spread that Minsec had borrowed AU$31 million to buy AU$35 million worth of shares in a weakening market. Brokers started asking their clients to sell their shares in the company. As prices kept dropping, lenders asked Minsec to put up more collateral for its loans. And finally stopped lending altogether. Minsec finally defaulted on its obligations. The company was suspended from the Sydney Stock Exchange on 4 February 1971, never to return.

Even as the company dug itself deeper into its debt hole, Tom Nestel kept hoping for a rebound. He bought shares in Minsec in his personal account all the way until late January 1971. When asked why he was buying shares in a failing company, he replied:

“I had confidence in the company and its future. I still believed in the philosophy that had carried the company along so successfully.”

What he did not realize was that the rules of the game had changed. What had worked in a bull market did not work so well once the value of the portfolio declined and lenders lost confidence. Minsec was a bull market phenomenon.

9. The aftermath

“I saw bank booms, land booms, silver booms, Northern Territory booms, and they all had one thing in common - they always burst.”

In author Trevor Sykes’ own words, the collapse of Minsec set off one of the greatest panics in Australian history.

Word got out that Minsec had borrowed AU$70 million in short-term money from money markets, with many of those loans callable at any point in time. After interest rates rose and share prices evaporated the value of Minsec’s portfolio, lenders wanted their money back.

After Minsec’s default, lenders took over collateral and sold that collateral on the market, causing prices to fall further.

Then the lenders became targets themselves. Many of them had borrowed in the short-term money markets, causing runs and a sudden loss of trust. Brokerage firms such as Patrick & Co failed as well, after their proprietary trading led to losses and customers default on purchase orders. It became a domino of failing businesses. Eventually, the prime minister had to step in and provide lending support.

Looking back at the failure of Minsec, author Trevor Sykes believes that their mistake was that they had:

- Borrowed short and invested long

- Investe in equities in a falling market

- Bought shares they couldn’t finance through their cash reserves

- Had allowed their leverage to rise to unreasonable levels

In his view, very few of the participants in the mining boom were outright thieves. They were just optimists and gamblers who were willing to take risks.

Looking back at the 1969-70 mining boom, not a single major deposit was discovered. Though it is true that the AU$850 million raised during the boom did help fund the development of new mines.

In the subsequent five years, Poseidon turned out to be a massive disappointment to investors. It soon realized that it would need AU$50 million to develop its Windarra mine, yet it only had AU$2 million left in cash and liquid assets. The solution was to team up with Western Mining Corporation, which took a 50% stake in the project.

But Poseidon incurred debt in the process. It tried to deal with its debt problems by its stake in the mine. But nobody wanted to buy it. And so in 1976, Poseidon defaulted on its debt and was delisted from the Australian exchanges.

During the bankruptcy, Poseidon’s 50% interest in Windarra was sold to Shell Australia for AU$30 million. But by that time, nickel prices had declined so much that Windarra had become only marginally economic. With these lower nickel prices, Shell saw no way of making the mine financially viable and it therefore shut down Windarra in 1978. The Poseidon dream was gone.

Perhaps the biggest lesson from the bust was that most exploration companies fail. The book quoted one study from Ontario Canada on mining claims between 1907 and 1953. About 6,600 mining companies had been formed during those 46 years, but only 348 reached production stage. Out of those, 294 failed to show a taxable profit. And only 54 companies ended up paying a dividend. In other words, the success rate was less than 1%.

10. Conclusion

Australia’s late 1960s mining boom was a period of mass hysteria and speculative excess. Insiders made fortunes, and retail investors were mostly left with the carcasses.

Exploration companies are valued based on the quality of their resources. But it’s not enough to take management numbers at face value. It’s probably worth getting a second opinion. And err on the side of caution, given the large number of assumptions that go into the value of a discovery.

I’d also avoid blank-check companies and investment vehicles. They tend to serve promoters rather than their investors, as we saw in the case of Minsec’s mutual funds.

Finally, I’d be mindful of what George Soros calls “reflexivity”. If miners are reliant on the market to raise capital for development, then a high share price can increase the likelihood of taking a mine to completion. But if the share price drops, it can get difficult, as we saw with Poseidon.

Reflexivity also matters for companies with leverage, especially those relying on short-term funding that has to be rolled over. If there is a sudden loss of trust, then the company might have to liquidate assets to fund debt repayments. Such forced selling can quickly cascade into bigger losses.

The book was illuminating, highlighting the dangers of getting involved in early-stage exploration companies. If there’s any lesson to be made, it’s the importance of not getting swept away by the crowd. And not get taken advantage of by insiders, who are often just as keen on mining for money in investors’ pockets as they are on mining for actual metals in the field.

Thank you for reading 🙏

If you would like to support me and get 20x high-quality deep-dives per year and other thematic reports like this, try out the Asian Century Stocks subscription service - all for the price of a few weekly cappuccinos.