Japan SaaS earnings season

No signs of disruption from generative AI

Disclaimer: Asian Century Stocks uses information sources believed to be reliable, but their accuracy cannot be guaranteed. The information contained in this publication is not intended to constitute individual investment advice and is not designed to meet your personal financial situation. The opinions expressed in such publications are those of the publisher and are subject to change without notice. You are advised to discuss your investment options with your financial advisers. Consult your financial adviser to understand whether any investment is suitable for your specific needs. I may, from time to time, have positions in the securities covered in the articles on this website. This is not a recommendation to buy or sell stocks.

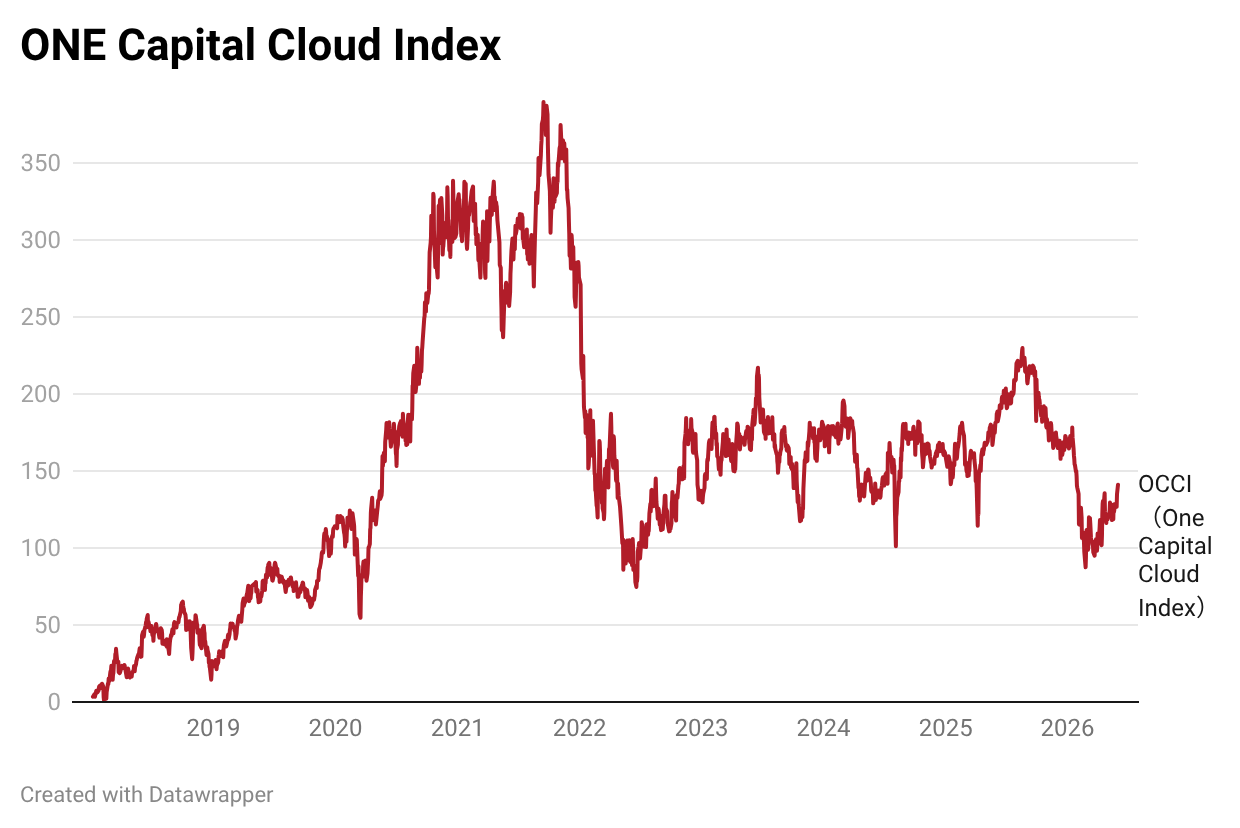

The Japanese software-as-a-service (SaaS) benchmark ONE Capital Cloud Index is starting to show signs of life:

This is despite the negative news flow that continues to weigh on the sector. The index is still down roughly 16% year-to-date, due to fears that software will be disrupted by generative AI tools.

What sparked the sell-off

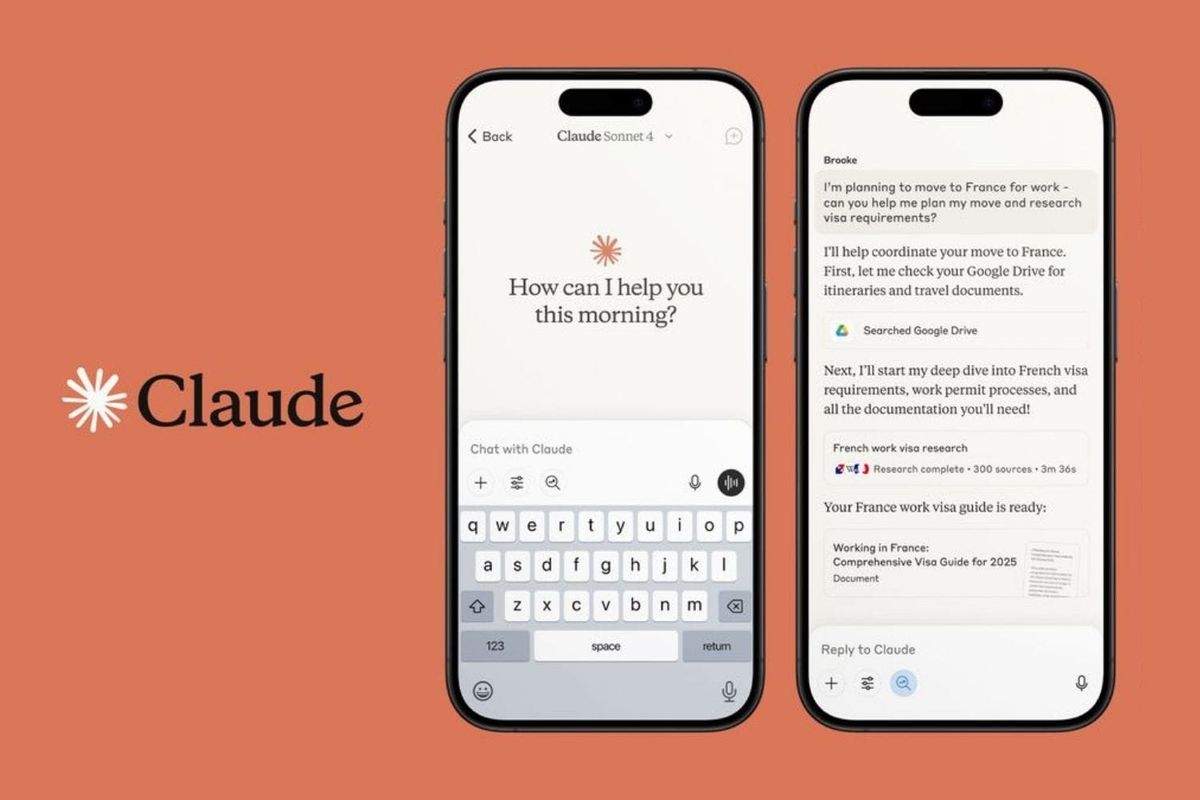

The announcement that initially sparked the sell-off was the launch of Anthropic's Claude Cowork on 12 January 2026:

I described some of the features of Cowork in my guide to Claude:

In short, Cowork is a chatbot that can control your computer. It can create and edit files on your hard drive. It can search the web and complete tasks. And it can autonomously carry out scheduled tasks without your input.

The sell-off accelerated on 30 January 2026 when Anthropic released a set of open-source enterprise plug-ins, including a legal automation suite. The software could now draft legal contracts, generate briefs and templated responses.

Investors felt that Claude Cowork could make corporate workers more productive, threatening the typical seat-based pricing model that has been used for cloud software. Some predicted mass unemployment. If AI agents can take over seemingly any task, why is there a need for traditional software at all?

In Japan, fund managers panicked, apparently told not to touch anything even remotely software-related. People around also sold their software stocks, thinking that the uncertainty had become too high.

The actual evidence of AI disruption is thin

While investors became nervous about Japanese software stocks, their earnings actually came in pretty strong. Here are the earnings reports that I think you should pay attention to:

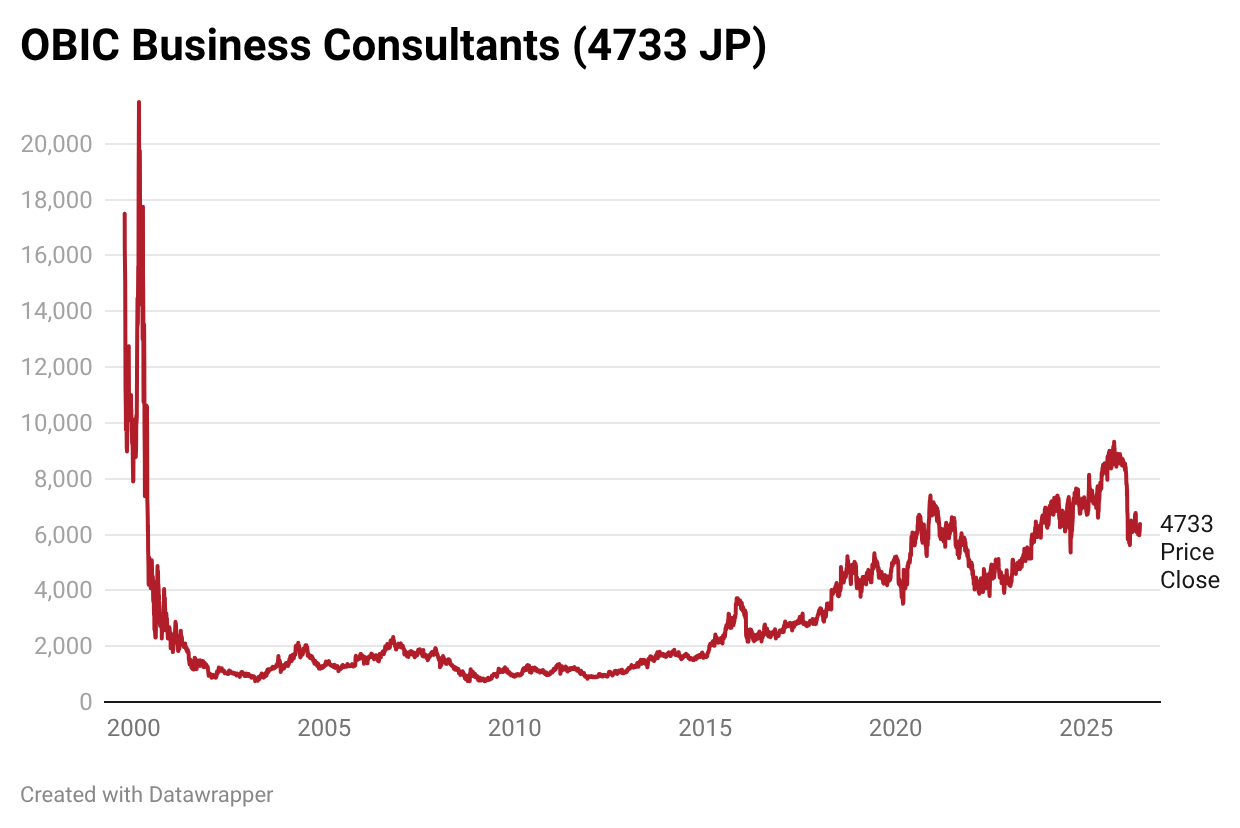

OBIC Business Consultants

Let's start with the bellwether stock OBIC Business Consultants (4733 JP — US$3.0 billion). That company did report a deceleration in growth from +12% in FY2025 to +9% in FY2026 ending March.

OBIC's enterprise resource planning (ERP) system, Bugyo, is used for accounting, payroll, and HR. It's been transitioning from on-premises to the cloud, but that transition has slowed. That's what caused the deceleration in earnings growth – not generative AI tools like Claude.

The stock now trades at 6.3x EV/Sales and 13.5x EV/EBIT. The operating margin is already 50%, so I don't expect much further margin potential.

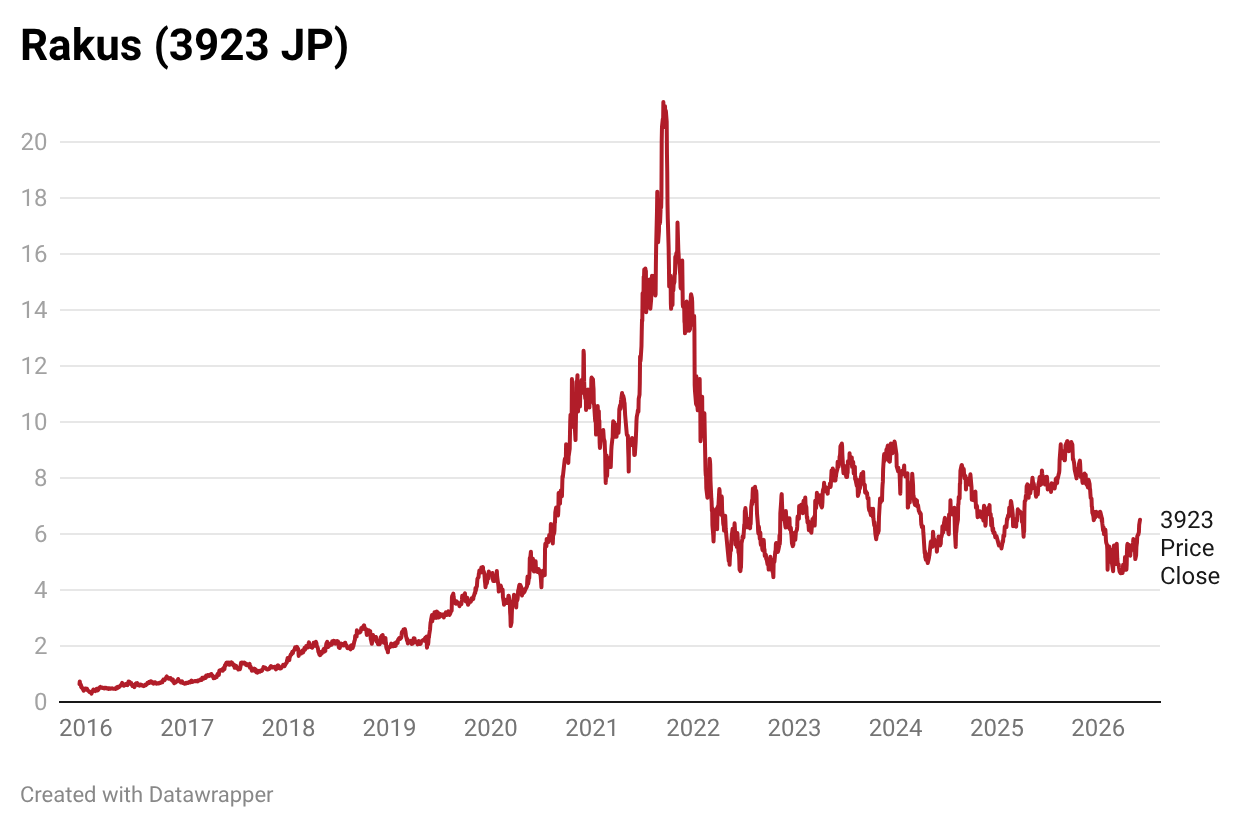

Rakus

Next, we have SME expense claim, invoice management and attendance system software developer Rakus (3923 JP – US$1.8 billion), whose stock price has recovered somewhat:

Rakus's FY2026 top-line growth decelerated as well, but from a high +27% to a still-high +23%. The churn from its core Raku Raku Seisan expense claim software keeps falling, now at just 0.17% per month. The group-wide operating margin hit a very comfortable 29%, up almost eight percentage points compared to last year's level. So this was a strong result. Rakus's FY2027 operating profit guidance is for +18% growth.

The stock now trades at 5.7x EV/Sales, which is high in a Japan SaaS context. There's no official margin guidance, but Rakus targets a "Rule of 50", which means that they want the revenue growth rate plus the operating margin to exceed 50%.

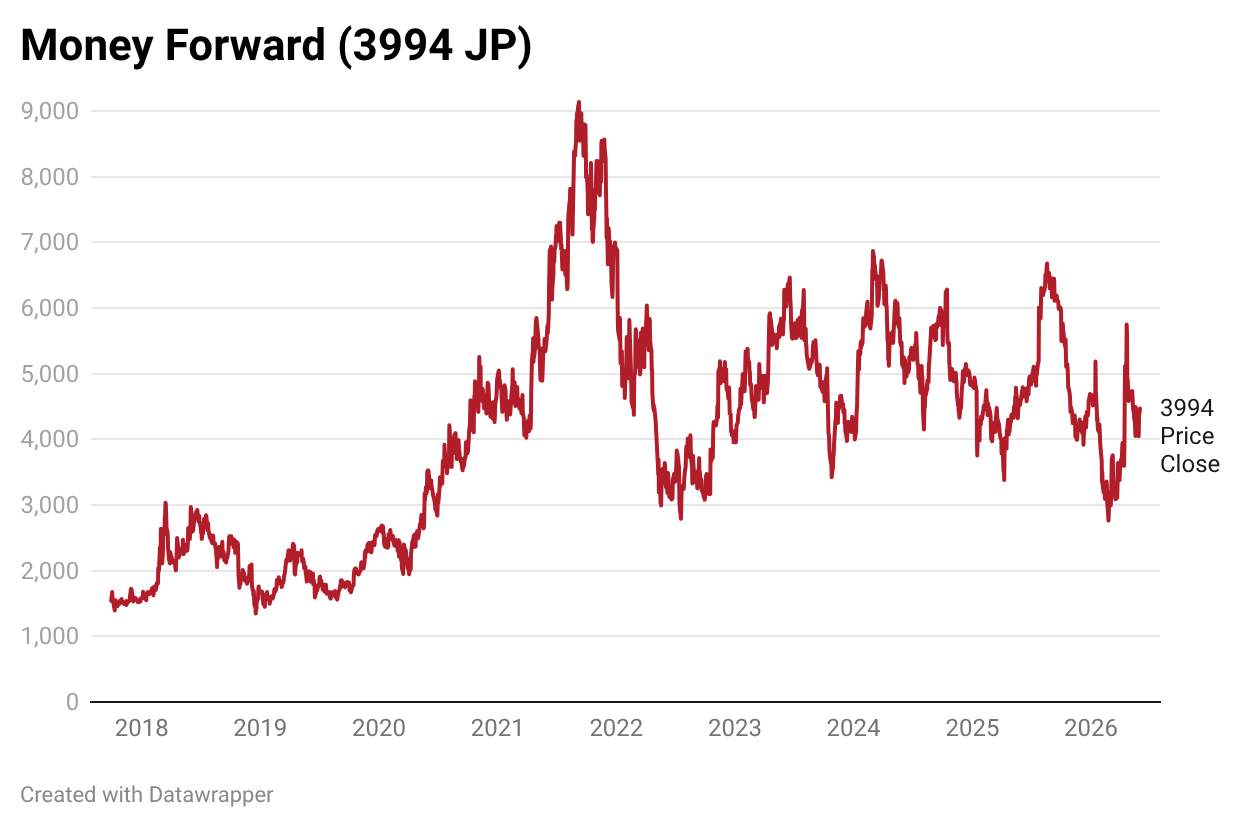

Money Forward

Accounting software company Money Forward (3994 JP — US$1.1 billion) reported an astoundingly strong 1Q2026 report, and the stock price reacted positively:

Quarterly like-for-like revenues grew +42% year-on-year. That was partly driven by the September 2025 price hike. But the number of corporate paying customers also increased rapidly by 21% year-on-year. I think it's the modular structure of its software suite that makes it attractive. Corporate customers can just pick the modules they want, and they're easy to cross-sell.

The market was also very excited about the new Claude-powered autonomous task assistant, Money Forward AI Cowork, which is set to be released in July 2026.

The stock now trades at 3.7x EV/Sales, which is broadly in line with the sector. The growth is higher than that of the average Japanese SaaS stock.

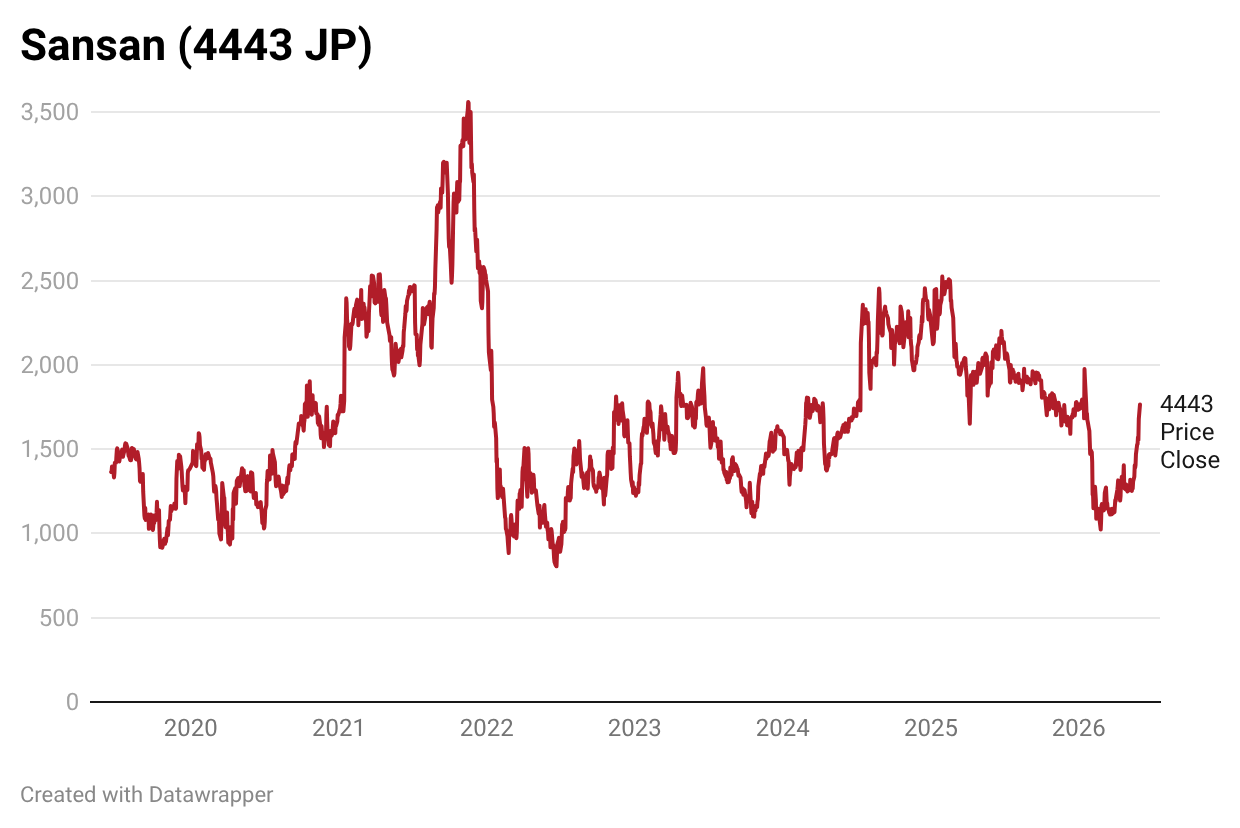

Sansan

Business card management software SanSan (4443 JP — US$902 million) also saw a partial rebound in its share price since the early January slump:

It reported 3QFY2026 numbers in April, beating expectations as well.

The company's net sales rose +25% year-on-year, driven by the business card management tool Sansan and the invoice management tool Bill One. There's been no obviously negative impact from Claude or other generative AI tools so far, and churn rates remained flat during the quarter. Instead, management is arguing that AI tools should increase the value of Sansan's business card database. The full-year growth forecast was upped from +24% to +25%, suggesting momentum in the business. The near-term operating margin target was also revised upwards from 20% to 23%.

The stock now trades at 3.2x EV/Sales, with a very long-term operating margin target of 30%+.

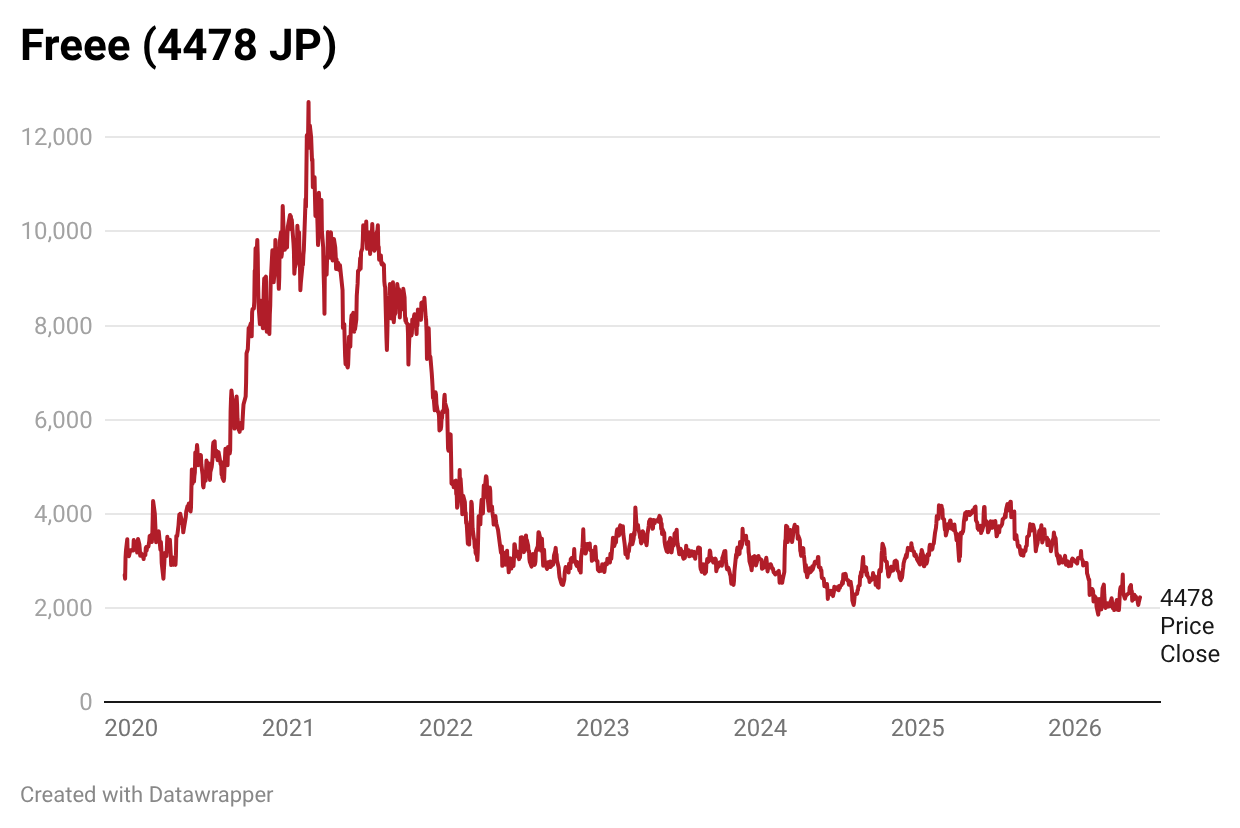

Freee

One disappointment last quarter was the 3QFY2026 result of accounting software company Freee (4478 JP – US$825 million), causing its share price to slump:

I wrote a deep dive on Freee back in late 2025:

Its quarterly top-line growth was decent at +27% year-on-year, but the annualized recurring revenue growth disappointed at just +23% year-on-year. The number of users on the platform rose by +14% year-on-year to 712,000, and ARPU rose by +9%.

Management said that it's now developing tools that will help users navigate the accounting and payroll features through AI prompts. AI will help automate tasks like submitting expense reports from receipts. Like Money Forward, it has developed an integration for Claude that will allow users to access Freee's data more easily.

As a system of record, Freee thinks it will be a net beneficiary of generative AI tools. And that the AI fears had "not yet materialized".

The stock now trades at 2.3x EV/Sales with 30% long-term operating margin guidance.

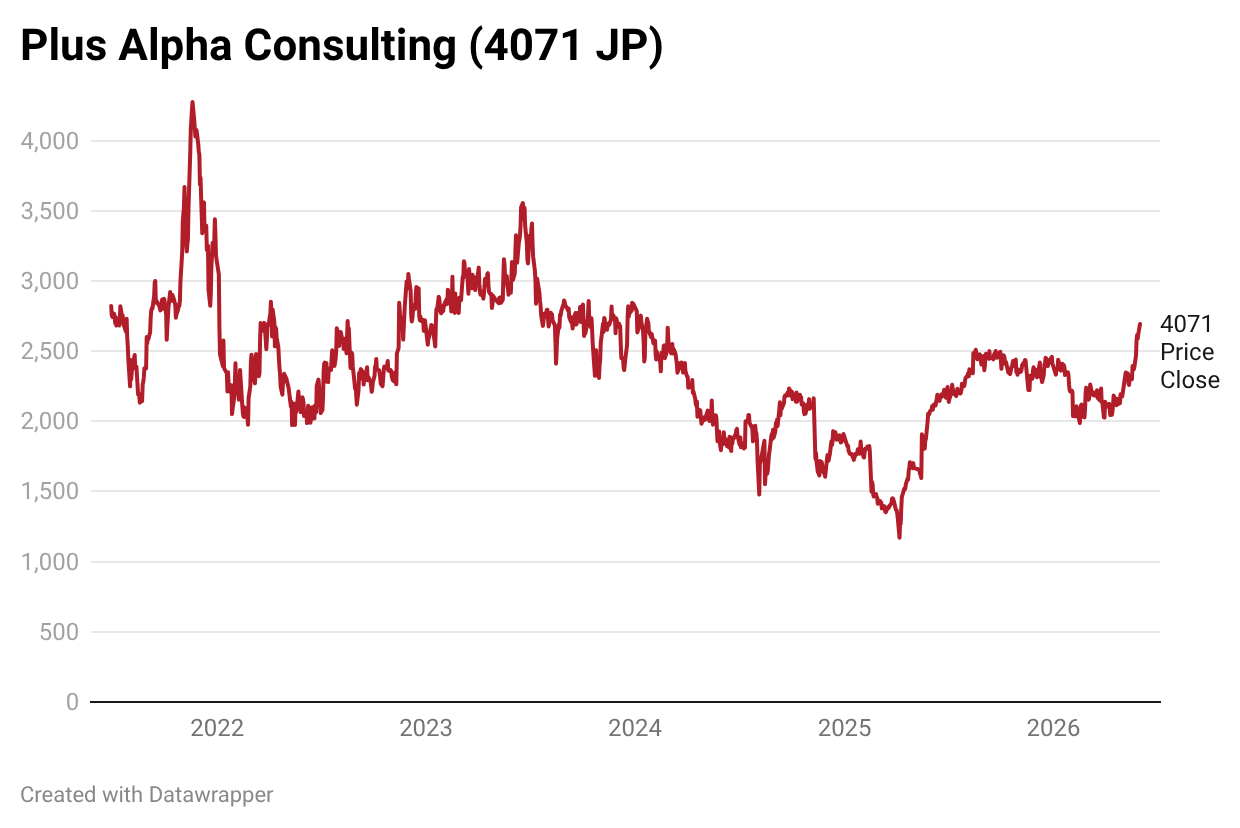

Plus Alpha Consulting

Talent management software developer Plus Alpha Consulting (4071 JP – US$715 million) has rallied since the early 2026 slump, partly thanks to new generous dividends and share buybacks:

Plus Alpha Consulting's 2Q2026 result was okay, with net sales growing +14% year-on-year and operating profit +32%. The result was driven by its core HR product, Talent Palette, whose operating margin just expanded to 50%. The churn rate for Talent Palette remained stable at just 0.36% per month.

Plus Alpha Consulting did see some pressure in its marketing solutions segment, though the new tool AI TalkTra has apparently caused active users to rebound. Management commented that Talent Palette is highly insulated from AI replacement, as it relies on proprietary data. If anything, PAC thinks generative AI should serve as a tailwind for its enterprise products.

The stock trades at 4.8x EV/Sales and 11.9x EV/EBIT. It targets a 30%+ operating margin in the longer term.

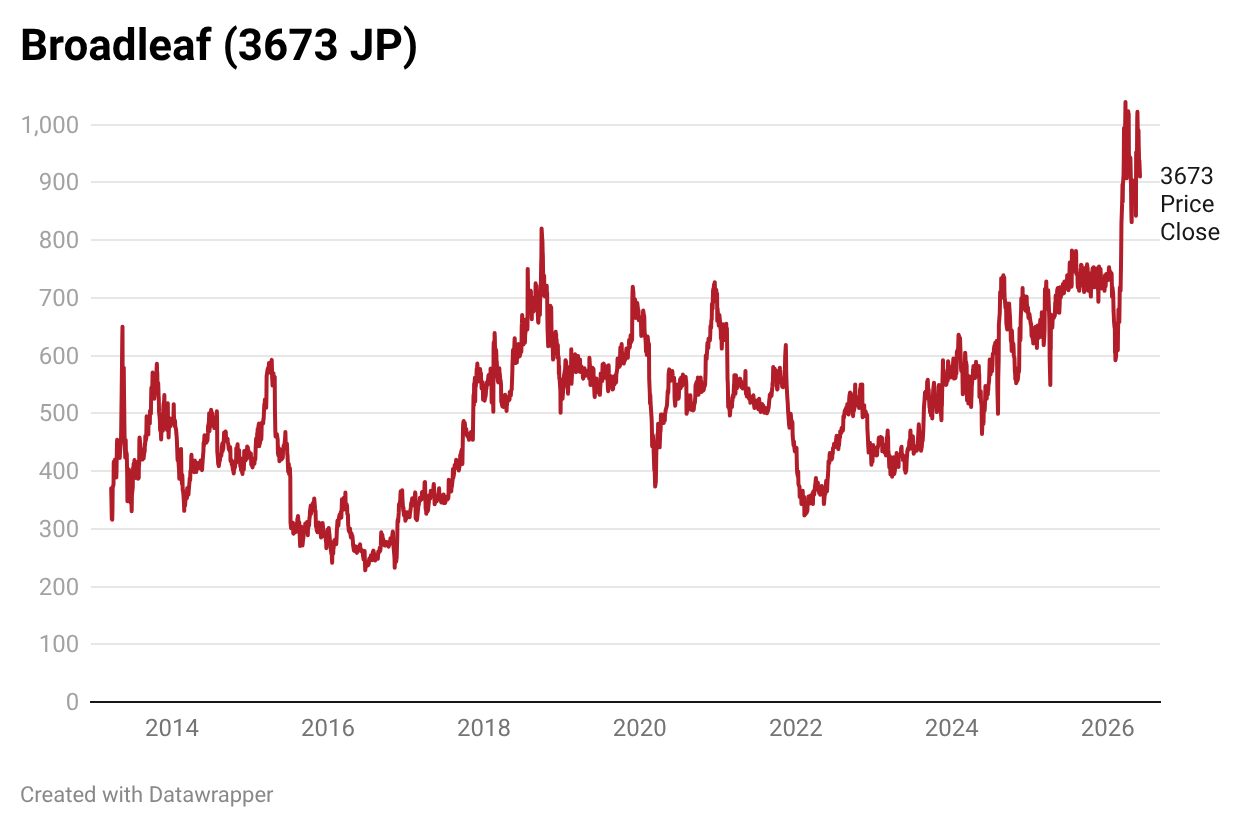

Broadleaf

Auto aftermarket software developer Broadleaf (3673 JP – US$513 million) saw a massive spike in its share price following strong earnings and a stock split:

The company offers an auto parts inventory database and a marketplace that connects buyers and sellers of auto parts. It's been transitioning to a SaaS pricing model, and that transition is now halfway through.

Broadleaf's 1QFY2026 results showed middling top-line growth of +16% year-on-year, but the cloud transition has proven highly margin-accretive. Its operating profit grew +142% year-on-year. Broadleaf's cloud rate reached 37%, with still some way to go before the transition takes place. The full-year guidance was left unchanged.

Management said it's now implementing AI features to help users search its database more effectively. Since Broadleaf relies on proprietary data and maintains an industry-standard "BL code" database, it cannot be easily disrupted.

The stock now trades at 6.4x EV/Sales and targets a 41% long-term operating margin.

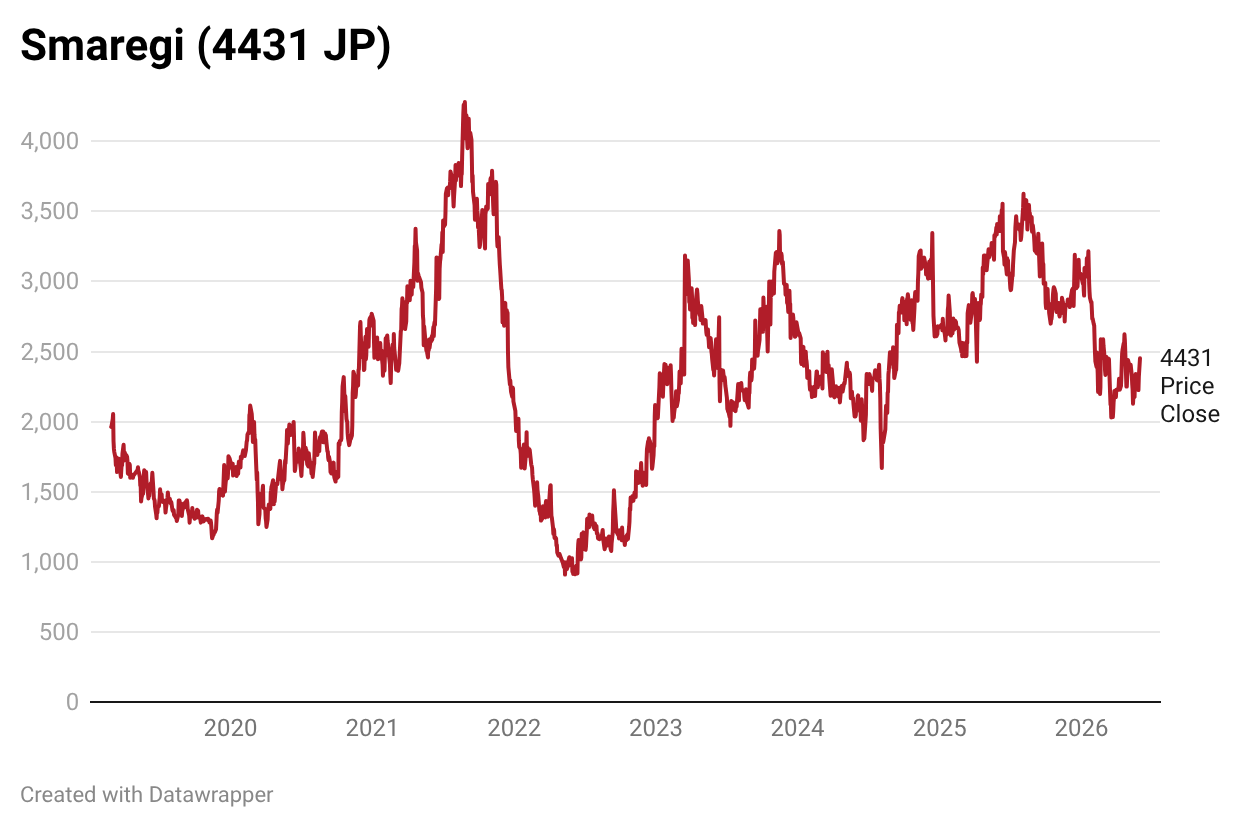

Smaregi

Payment solutions company Smaregi (4431 JP – US$296 million) has been range-bound since the early part of 2026:

Smaregi sells point-of-sale hardware connected to a software platform that helps retailers manage their businesses. This platform includes an app store, and Smaregi takes a 30% cut, just like Apple and Sony PlayStation.

The latest 3QFY2026 quarterly result ending January was okay, with revenue +22% year-on-year, and net profit +25% year-on-year. However, the full-year revenue growth guidance was raised to +30% year-on-year. The churn rate stayed flat at 0.47%.

The reason Smaregi's share price has come down has less to do with generative AI and more with the recent data leak, in which the personal information of 100,000 users on one of its apps in its app store was stolen. That could be why the 3QFY2026 hardware sales declined by -9%, which might pose a problem in the future.

Smaregi is a nimble company, however, and management is arguing that they'll benefit from generative AI. The company is now using OpenAI and Gemini integrations to analyze transaction data to provide better analytics to its merchants. Coding efficiency has apparently improved as well.

The only question is whether the data leak will affect the company's future growth. Smaregi now trades at 2.6x EV/Sales and 11.8x EV/EBIT but no operating margin guidance has been provided yet.

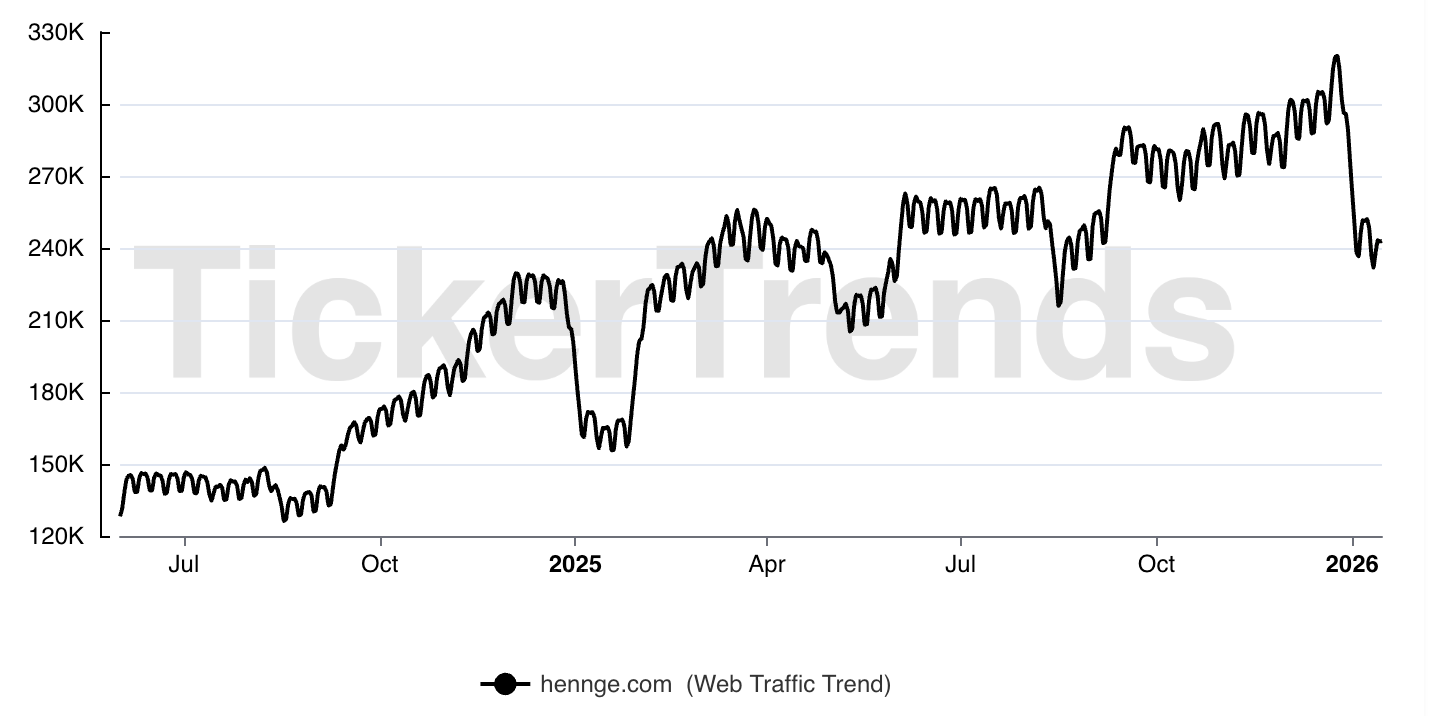

Hennge

Japanese identity-as-a-Service company Hennge (4475 JP – US$229 million) has seen a partial rebound in its share price since early 2026:

Hennge competes with Microsoft Entra ID. It can best be thought of as Japan's answer to Okta, the US cloud security business. The core service is to provide secure log-ins for employees to other software platforms, without the need for additional passwords. The company uses Hennge to control what software employees have access to. Hennge also has an email security feature that automatically encrypts all email attachments.

The company reported a just-okay 2QFY2026 in May, with 1H2026 revenues up 18% year-on-year and operating income up 13% year-on-year. The number of customers increased by +17%. The churn rate fell 6 basis points to just 0.26%. There's been some pressure on ARPU, as larger clients have opted for cheaper, single-function plans.

There's no indication that Hennge has been negatively affected by generative AI. Management is still projecting 20% CAGR for its core Hennge One product through FY2029. And it targets JPY 20 billion in annualized revenues by FY2029. The website traffic trends still look positive:

The stock now trades at 4.6x EV/Sales, slightly below Okta's 6.8x. Longer-term, the company believes it will hit an operating margin of 50%, though that will be far into the future, perhaps by the mid-2030s.

CYND

CYND (4256 JP – US$38 million) owns a software suite called Beauty Merit, which you can think of as a reservation management tool for beauty salons. It acquired its second-biggest competitor, Pacific Porter, in 2023. Since that time, the stock price nearly doubled, before coming off earlier this year:

A primary reason for the recent decline was a data leak when unauthorized access to Beauty Merit was discovered. It's not clear whether any data was compromised. But CYND couldn't rule it out either.

The latest earnings results for FY2026, ending March, showed top-line growth of +13% year-on-year, slightly below estimates. The operating profit grew by +40%, driven by customer wins and operating leverage. But with an annualized recurring revenue growth of +11%, there doesn't seem to be a great deal of momentum in the business.

The churn rate remained flat at 0.65% per month. I don't think generative AI tools can easily synchronize bookings across point-of-sale systems and booking sites. CYND launched an AI-driven machine learning tool for dynamic pricing strategies within the Beauty Merit app, which could eventually help its customers.

The stock now trades at 1.8x EV/Sales, but the company does not have a formal operating margin target.

Poper

Poper (5134 JP – US$12 million) is a Japanese nanocap software developer serving the local tutoring industry. I wrote about it here:

The core software suite, Comiru, allows students to communicate with parents, provide them with updates on how the students are progressing, whether they're attending their classes, etc. Students can also pay via the app. Teachers also use Comiru to manage their schedules.

Comiru's share price came off significantly in late 2025 and early 2026:

The reason was a large number of customized software projects being recognized as revenue in 2025, and then a complete shutdown of such projects. The latest 1QFY2026 report ending January was weak. Net sales grew only +1% year-on-year, and operating profit declined by -42%. However, the annualized recurring revenue did grow 8.5% year-on-year, and the number of paying clients actually grew with +15% with student numbers +13%. The churn rate remains decent at 0.5%.

The problem seems to be Poper moving to less lucrative non-cram schools. Its customized software development projects last year are also forming a high base, causing growth to slow down. The slowdown in growth is almost definitely not due to generative AI tools, but rather competitors that existed before ChatGPT, including LINE.

Poper is now moving away from customized software to standardized cloud service platforms. And Poper is guiding to a sequential recovery in 2Q2026, as several larger customers have recently joined Comiru. The stock trades at 1.9x EV/Sales with no operating margin target.

Conclusion

So as you can tell, there's practically zero evidence of any disruption from Claude or even other generative AI tools. Churn rates have remained stable or continued to fall. And while growth has declined in some cases, it's almost always due to competitive pressures or one-off events such as cybersecurity incidents.

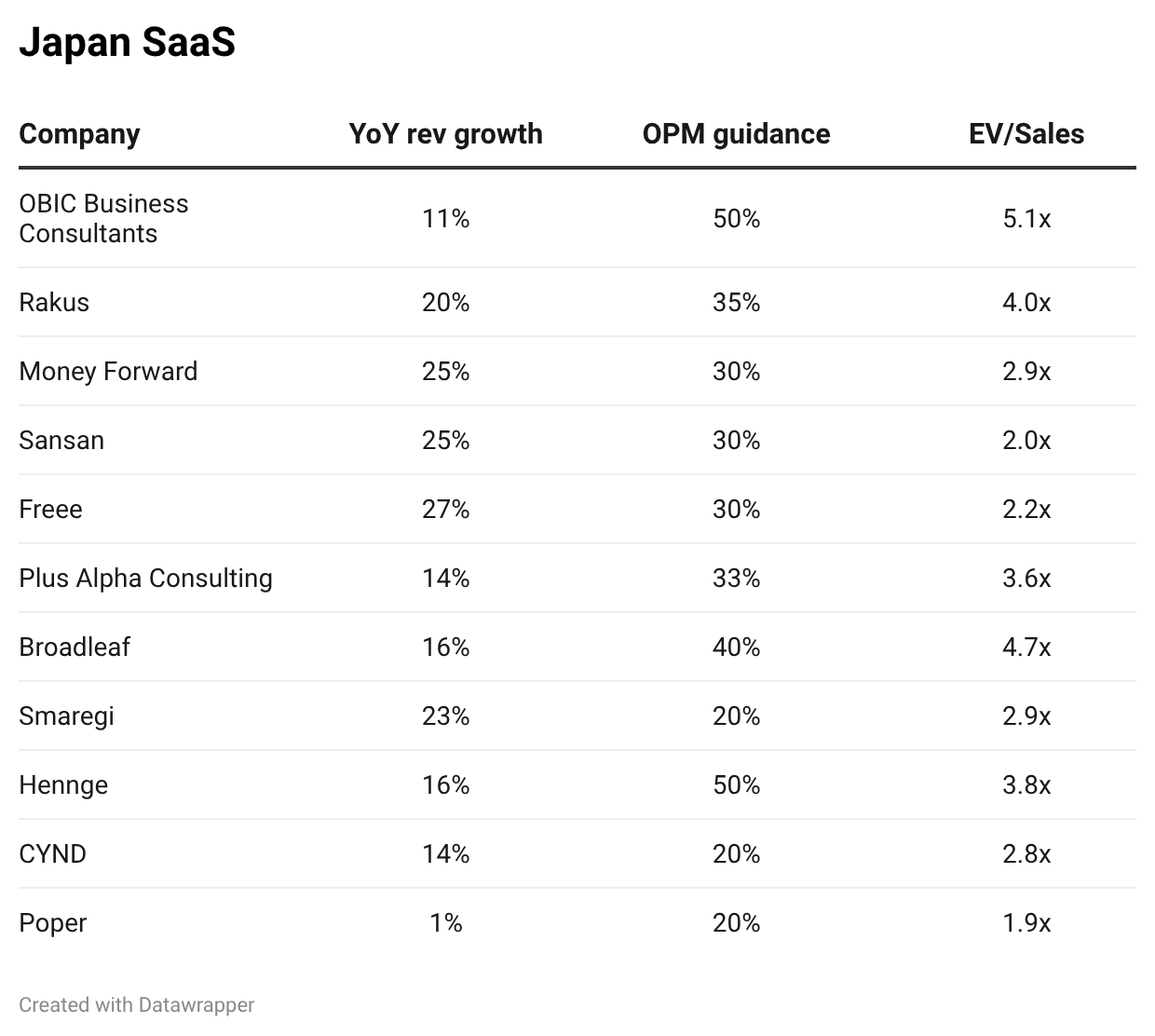

Here's how the latest results stack up against their EV/Sales multiples:

As you can tell from the table, many of these stocks trade at margin-adjusted EV/EBIT below 10x, despite continued growth. That's the case for accounting software developers Money Forward and Freee.

Both Hennge and Smaregi are guiding for relatively high top-line growth going forward. The former could be facing competitive pressure from Microsoft. And the latter has seen its growth slow down due to a data leak. But the guidance seems to suggest that growth will continue.

One cannot completely rule out the risk of AI-native software companies popping up and posing a direct threat to these companies. But so far, the evidence is thin. And Japan's SaaS sector continues to trade at rock-bottom valuation multiples.