Borrowing ideas from funds, part 6

Estimated reading time: 19 minutes

Here’s yet another edition of my reviews of the key holdings of Asia-focused funds.

I will release new editions as time progresses.

Summary

- I love VARECS Partners’ strategy of focusing on companies dominating their niches. The stock that intrigues me the most is the online auction platform Aucnet. The stock trades at a P/E of 8.5x and EV/EBIT of 2.5x. For reference, Thailand’s Union Auction trades at 20.5x and Copart at 30.0x.

- Forager Funds seem to like niche software businesses. In any case, New Zealand’s Tourism Holdings fits into my personal positive view of Asian tourism. The stock trades at a consensus 2024e P/E of 11.6x, which does seem low.

- Airlie Funds proclaims to have a value-focused strategy. But neither of their top positions trade at particularly low multiples. I suppose Tabcorp trades at an EV/Sales of 0.8x. I covered the stock in this prior deep dive here.

- VinaCapital’s Vietnam Opportunity Fund is publicly traded and seems to give exposure to companies with high margins and high returns on equity. After listening to the Business Breakdown podcast on India’s Titan, I’m starting to understand the attractiveness of Phu Nhuan Jewelry. I also think that FPT Corporation makes sense. And PetroVietnam Technical Services will probably benefit from any upswing in regional energy sector capex.

- Capital Dynamics’ Tan Teng Boo is an old-school value investor. I do think his portfolio company Padini is a high-quality retailer, mostly thanks to the brilliance of founder Yong Pang Chaun. It enjoys a return on equity of 26%. I’ve long been sceptical about their ability to deal with the competition with H&M, Uniqlo and Zara. But I’ve been proven wrong. The valuation multiple of P/E 12.3x remains low.

VARECS Partners VPL-I Trust

Tokyo-based Varecs Partners was founded by Jiro Yasu, previously at First Eagle in New York City, focusing on Asian equities for them. Since 2006, he’s been the portfolio manager for VARECS Partners’ VPL-I Trust.

There is no performance data for the trust, at least not in the public domain.

The strategy is to invest in high-quality businesses at significant discounts to intrinsic value. According to the website, they prefer dominant businesses in niche markets. And since they’re long-term investors, they hope for intrinsic value to “compound”. At least, that’s how they think about the intrinsic value concept.

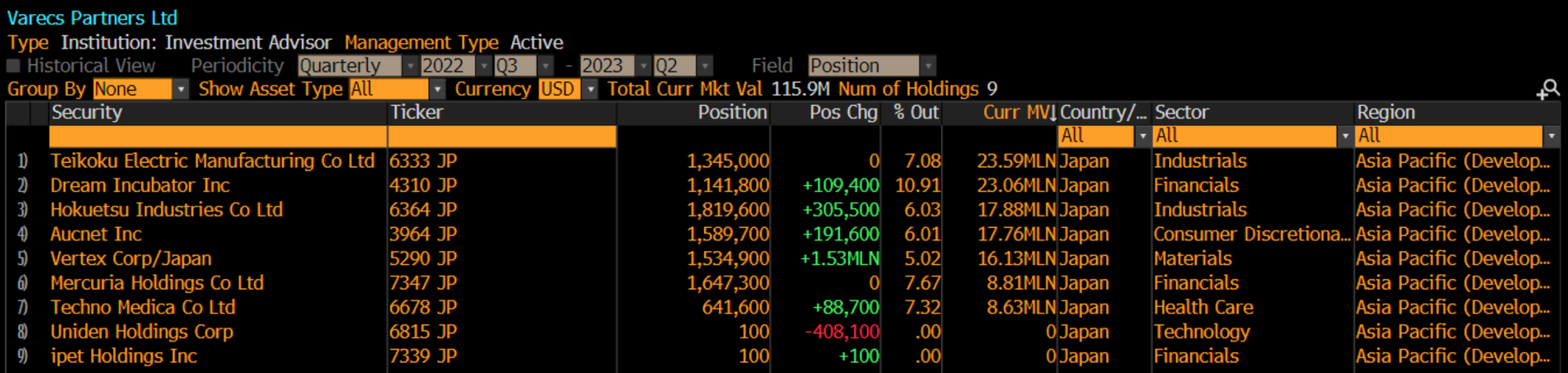

There is no full disclosure of VPL-I Trust’s portfolio. But since VARECS takes large positions, they’ve had to disclose their positions in the seven companies with larger than 5% stakes. These companies are eclectic, to say the least.

Teikoku Electric Manufacturing (6333 JP - US$334 million) produces no-leak canned pumps, with a 40% global market share in its segment. Canned pumps are used in the chemicals and petrochemical industries where hazardous materials are being handled, and liquids need to be transferred with zero risk of leakage. The stock has performed well and still trades at just 13.0x P/E.

Dream Incubator (4310 JP - US$212 million) is a consulting company established by Koichi Hori, a former BCG consultant. It has a venture capital business, incubating start-ups. It also has a consulting arm which serves large enterprises and the government. And it also does M&A advisory. Its profitability has been inconsistent, but the stock trades at 0.27x revenues.

Hokuetsu Industries (6364 JP - US$300 million) is Japan’s largest producer of air compressors used in sectors such as construction, mining, agriculture, and manufacturing. Compressed air is used as a power source for tools and machinery. Compressed air can also be used for drying, blowing and cleaning. Hokuetsu’s earnings have recovered nicely from COVID-19. It trades at 10.1x P/E.

Aucnet (3964 JP - US$295 million) has an online auction platform for used cars and machinery. The company also offers inspection services for the vehicles listed on the platform to guarantee the quality of the items. It also offers payment services with escrow accounts and delivery of the vehicles to the customer. The commission is charged as a percentage of the price of each vehicle. The stock trades at just 9.5x P/E with a 3.2% dividend yield.

Vertex (5290 JP - US$313 million) produces concrete-related products such as beams, columns and panels, bridge girders, and tunnel linings. They’re essentially a supplier to construction companies. The stock has performed beautifully over the past two years yet only trades at 10.1x P/E.

Mercuria (7347 JP - US$116 million) is a fund manager founded as a JV between the Development Bank of Japan and Asuka Asset Management. They provide growth capital to small and medium-sized enterprises in Japan that have demonstrated potential for expansion but require additional funding to accelerate. To date, Mercuria has invested in healthcare, education and tech companies. Its main shareholder is Itochu. The stock trades at 9.5x P/E with a 5.6% dividend yield.

Techno Medica (6678 JP - US$117 million) manufactures and sells internally-developed test tube preparation systems, automating whole blood and urine tests from check-in to collection. It has a domestic market share of about 90% and is now turning overseas for growth. The stock trades at just 12.9x P/E with a 3.3% dividend yield.

Forager Australian Shares Fund

Forager Funds was founded by Steve Johnson in 2009. The fund manager is focused on long-term value in companies that other investors overlook. Today, they manage around AU$350 million in assets under management.

Johnson started at Macquarie, then shifted into writing a newsletter called “The Intelligent Investor” between 2003 and 2009. Today, he manages several funds, including the Forager Australian Shares Fund and the Forager International Shares Fund.

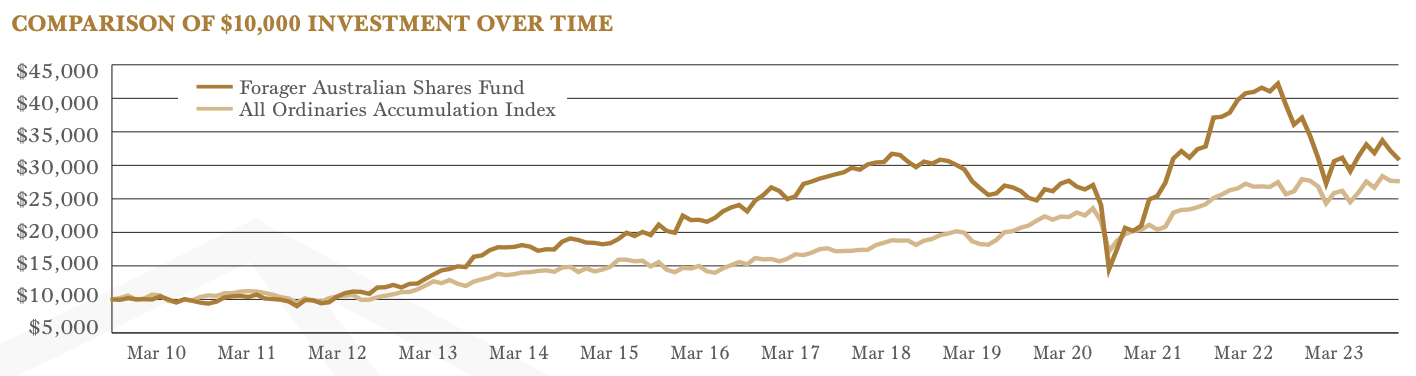

Since its inception, the Forager Australian Shares Fund has performed better than the index, though not significantly. On my numbers, I get to a compound annual growth rate of about 8%.

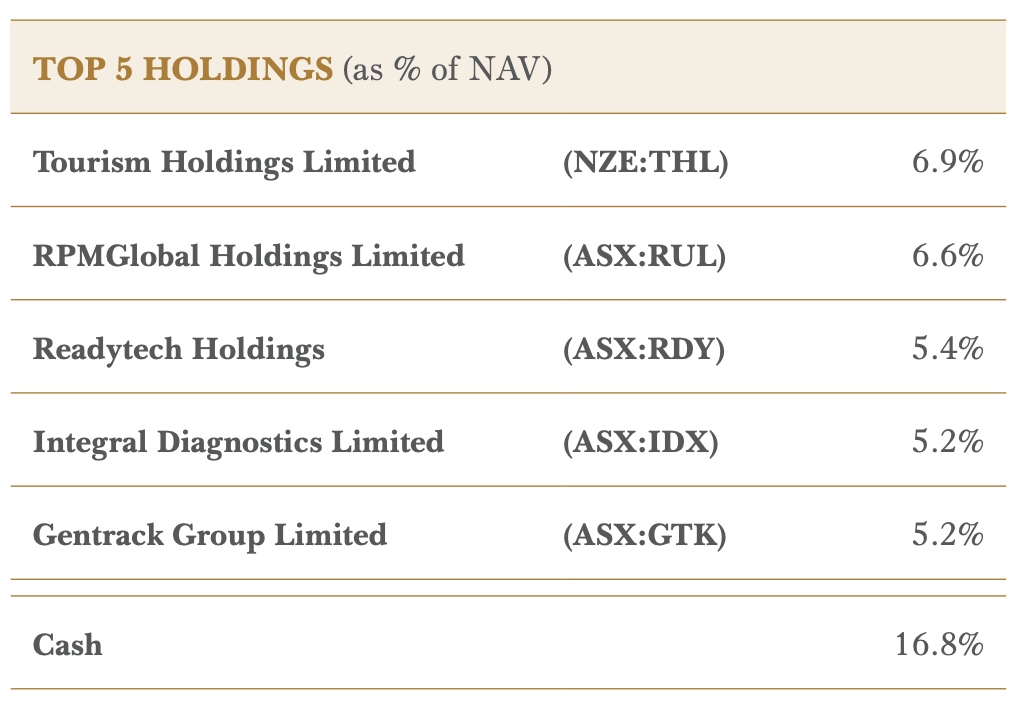

According to the latest March 2023 fact sheet for the Australian Shares Fund, the largest exposures are companies that are relatively obscure to the average investor.

Tourism Holdings (THL NZ - US$564 million) is a New Zealand-based company that sells campervans, motorhome rentals and tourism-related services such as holiday park management, tour agencies, etc. Regarding motorhomes, its fleet is currently over 6,000 vehicles, mostly in New Zealand and Australia. The stock has performed nicely in the past year. On a forward-looking basis, the stock still trades at just 11.6x P/E.

RPM Global (RUL AU - US$218 million) develops software solutions for metals & mining companies. A few of its software programs include mine design, planning, scheduling and optimisation solutions for open-cut and underground mining. RPM also sells an asset management solution that helps companies manage their mining equipment and infrastructure. The company is losing money but its EV/Sales multiple is 3.9x.

Readytech (RDY AU - US$228 million) is another company, but focusing on a different niche: education. Readytech’s software is focused on student management software, measuring enrolment, attendance, assessment and reporting. It can also help manage school employees, including payroll services and compliance. Readytech also has an e-learning platform, but its popularity is unclear. The stock now trades at a P/E of 17.8x, though be aware of the historically low return on capital.

Integral Diagnostics (IDX AU - US$492 million) provides diagnostic imaging services such as X-rays, ultrasounds, mammograms, CT scans, MRI scans, etc. They have a number of diagnostic imaging centres across Australia and have built up a network of doctors referring patients to their clinics. It seems like growth has been driven by acquisitions, leading to a weak return on equity. Trailing twelve-month P/E on a GAAP basis is currently 27.6x, which doesn’t sound all that low.

Gentrack Group (GTK AU - US$200 million) is also a software developer in another vertical: solutions for utilities and airports. Its software is used for billing, customer management, operational analytics, etc. Its apparently been used by over 200 utilities and airport operators worldwide, including in Australia. The company is barely profitable but trades at an EV/Sales of 2.3x.

Airlie Australian Shares Fund

Airlie Funds Management is one of the Australian value investors I respect the most. I came across them during my research of Tabcorp, covered here. But the firm also seems to have a decent reputation among the Australian investment community.

The company was founded in 2012 by John Sevior, who came from being head of equities at Perpetual. Today, it runs about AU$9billion in assets under management, with a clear value-focused approach. In 2018, Magellan Financial Group acquired Airlie. And more recently, John Sevior has said he will retire from Airlie in June 2023.

The Australian Shares fund is today run by Matt Williams, who was also head of equities for Perpetual, though at a later date. Co-portfolio manager for the fund is Emma Fisher. She can be found on Airlie’s YouTube channel, where she provides quarterly updates to investors.

The fund’s strategy is bottoms-up, long-only and concentrated into roughly 25 stocks in Australia. They call their approach “active, high conviction”. Current assets under management are AU$ 347 million.

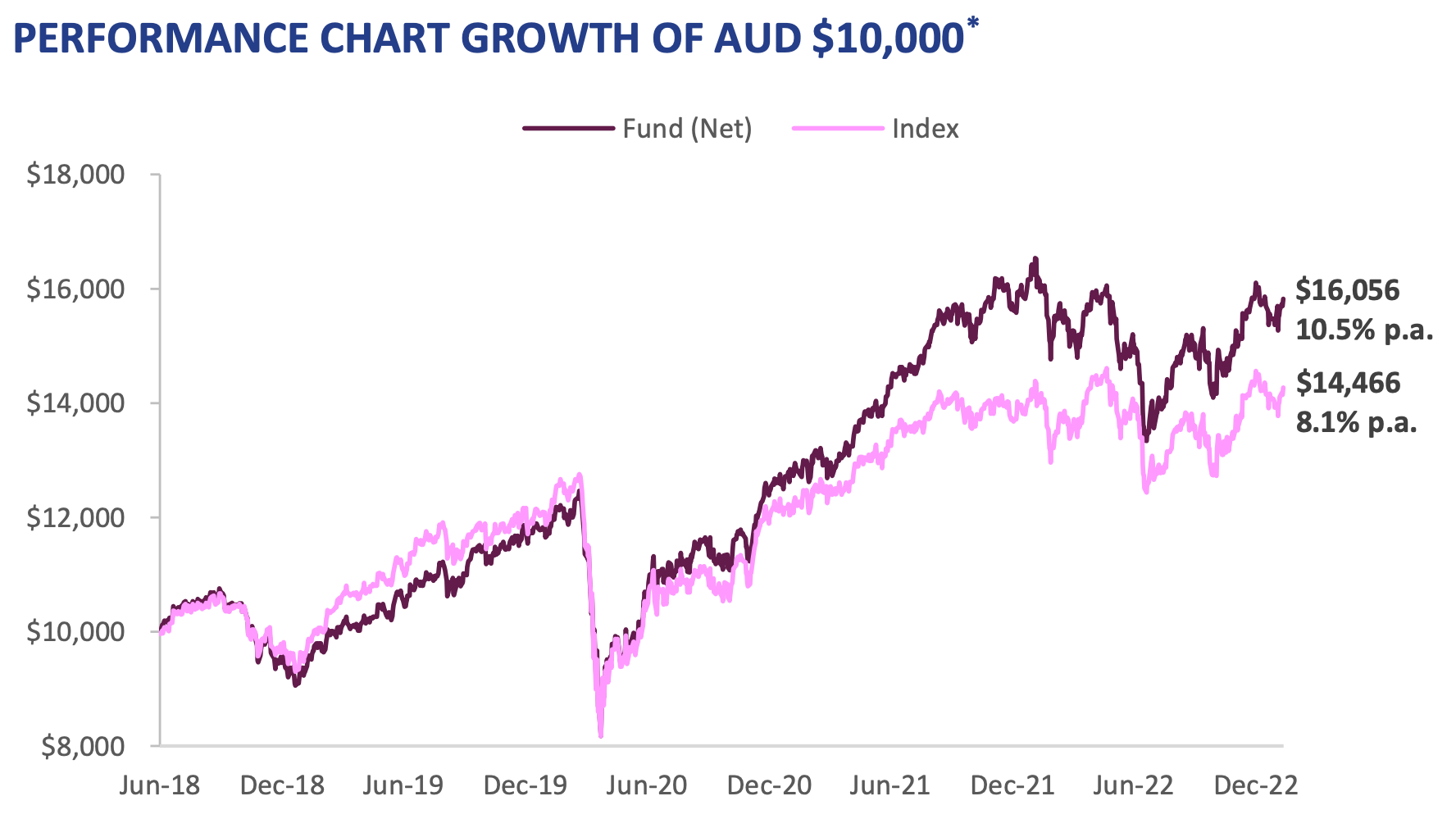

The performance of Airlie’s Australian Shares Fund has been quite impressive at 10.5% per annum compared to an index return of 8.1%.

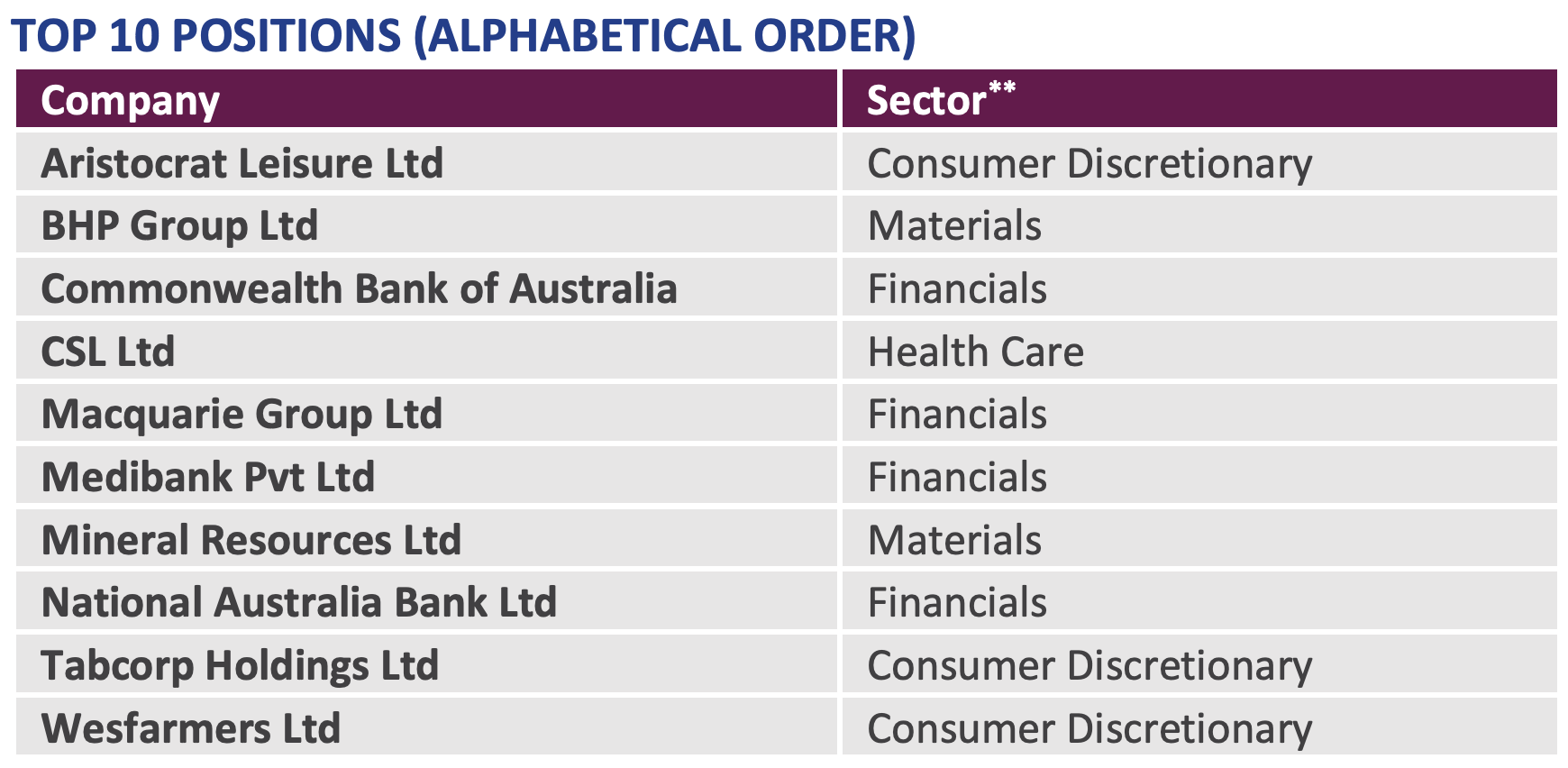

While I haven’t been able to retrieve the entire portfolio, the fund’s top ten positions are disclosed in the fund’s monthly fact sheets, for example, here. Since they are listed in alphabetical order, unfortunately, we do not know which of these stocks are their highest conviction bets.

This portfolio is decidedly mainstream. The portfolio covers major index weights such as BHP, Commonwealth Bank, CSL, National Australia Bank and Macquarie. While the Australian banks enjoy stronger underlying profitability than most of their European peers, I personally question why you’d want to own them in the face of a weakening Australian property market. And 2023 is when many mortgages face interest rate resets, which will undoubtedly be challenging for many homeowners. I also question whether my former employer, Macquarie, will do well in a high-interest-rate environment.

Airlie has a larger-than-index weight on Aristocrat Leisure (ALL AU - US$17 billion). The company produces slot machines under the brands Buffalo, Queen of the Nile, and More Chilli. It also has an online game developer subsidiary, Product Madness, which produces free-to-play casino games for social media platforms like Facebook. The stock has recovered from COVID-19 and trades at a fairly lofty P/E multiple of 27.7x.

Mineral Resources (MIN AU - US$10 billion) is even more of an off-index bet. It’s a mining services business with excellent returns on capital thanks to its (historically) asset-light business model. The services offered include mine design and construction, mining and crushing, and mine site operation and maintenance. It also has a renewable energy subsidiary focusing on waste-to-energy and gas-fired power generation. The stock has gone on a massive rally since 2020, thanks to its exposure to the lithium mining industry. The stock trades at P/E 21.6x, but be aware that Chinese onshore lithium prices have started falling.

Medibank (MPL AU - US$6.6 billion) provides health insurance domestically and healthcare services such as telehealth, in-home care and support services, etc. Earnings growth has been somewhat weak, but the company pays out most of its earnings as dividends, providing a 3.8% dividend yield. The 2024e P/E ratio is 19.3x.

Lastly, Airlie has invested in offline wagering services company Tabcorp (TAH AU - US$1.6 billion). They invested in the stock before the spin-off of The Lottery Corporation. But according to analyst Will Granger in this video here, they are now more bullish on the former, given the large valuation disparity that has emerged. Weak foot traffic at Tabcorp’s retail venues during COVID-19 is now in the rearview mirror. States are also equalising the playing fields between the taxes paid by online and offline wagering companies. The stock trades at an EV/Sales of 0.88x. I wrote about Tabcorp in a prior dee-dive available here.

VinaCapital Vietnam Opportunity Fund

VinaCapital is a Vietnam-focused asset manager founded in 2003 by a group of American and European businessmen and portfolio managers. Today, it’s one of Vietnam’s largest investment managers with US$4 billion in assets under management.

Vietnam Opportunity Fund (VOF LN - US$846 million) was launched that same year as a closed-end fund listed on the London stock exchange. The fund invests in a diversified portfolio of listed and unlisted equities, real estate and private equity.

VOF’s performance has been impressive, rising roughly 11% annually in British Pound terms.

The fund is managed by a group of individuals at VinaCapital, including portfolio manager Khanh Vu and VinaCapital’s CIO Andy Ho, whose book I reviewed here and can be purchased here.

Andy has been with VinaCapital since 2007 and now leads the firm’s investment strategy and portfolio construction. Before VinaCapital, he worked as an investment banker for Goldman Sachs in New York and Hong Kong. He also worked for US-based private equity firm Pegasus Capital. He has an MBA from Kellogg.

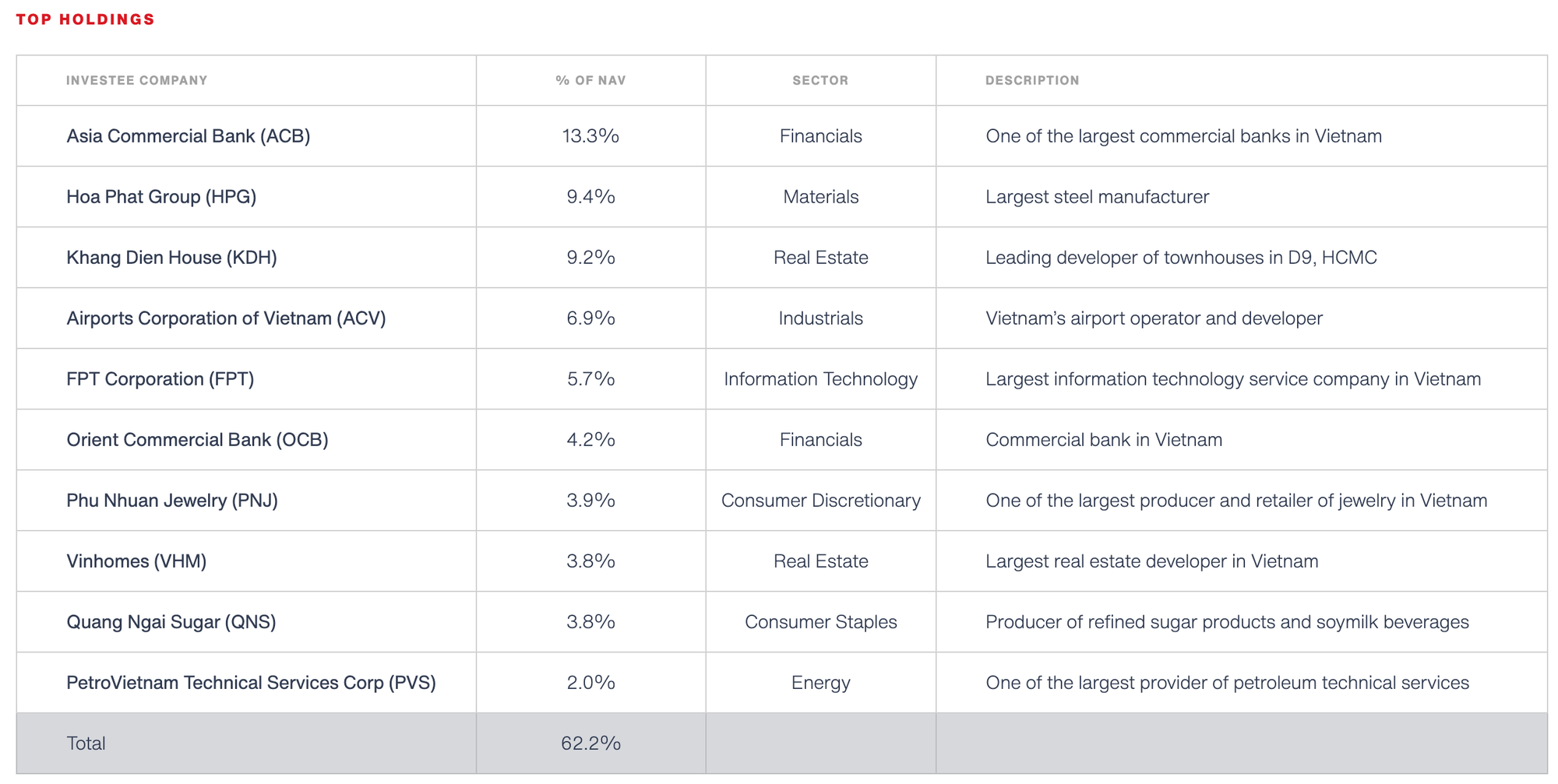

The portfolio is 100% focused on Vietnam and seemingly index-agnostic:

Asia Commercial Bank (ACB VN - US$3.5 billion) is one of the largest commercial banks in Vietnam, with total assets of roughly US$30 billion. It seems that ACB has been at the forefront regarding its technology, with a slick mobile app and online banking platform. Its financial performance is also impressive. The stock trades at a P/E of 6.1x, despite a return on equity in the mid-20s.

Hoa Phat Group (HPG VN - US$5.1 billion) used to be VOF’s largest position, but it looks like it’s now been sold down in favour of ACB. It’s a large Vietnamese steel manufacturer with two steel plants and over 7 million tonnes of capacity. Hoa Phat also has a real estate development subsidiary called Hoa Phat Land and an agriculture subsidiary producing and exporting rice, coffee and cashew nuts. The stock trades at a P/E of 11.8x.

Khang Dien House (KDH VN - US$868 million) is a Vietnamese real estate developer across residential (luxury villas, apartments, townhouses) and commercial (office towers and shopping centres). It has pioneered mixed communities such as Celadon City in Ho Chi Minh City, which has many facilities, including schools, shops, recreational facilities, etc. They seem to be focused on higher-end developments. The stock trades at trailing 27.0x P/E but note that the Vietnamese real estate sector is in a downturn due to a lack of credit. The P/B is 1.8x, in line with its historical level.

Airports Corporation of Vietnam (ACV VN - US$7.1 billion) is a state-owned enterprise operating 22 airports in Vietnam, including the Noi Bai International Airport and Tan Son Nhat International Airport in Ho Chi Minh City. The state continues to own most of the shares, and the Chairman is a former government official from the Civil Aviation Authority. The retail side of the business only represents 12% of revenue vs 50% at most modern airports. But the airport is highly regulated, and higher profitability will be driven primarily by higher passenger numbers. The stock trades at 26.9x P/E, with earnings having more or less recovered from COVID-19.

FPT Corporation (FPT VN - US$3.7 billion) is a tech conglomerate based in Hanoi, focusing on a number of disparate segments: software outsourcing (primarily to Japanese clients), broadband and wireless telecom services, retail shops, digital content and a tech-oriented university. Despite decent earnings growth in the past few years, the stock trades at no more than 13.9x P/E.

Orient Commercial Bank (OCB VN - US$944 million) is a smaller commercial bank owned partly by Japan’s Aozora Bank and the Trinh Van Tuan family. The returns on capital metrics are impressive, with a return on equity of 25%, putting it in the top 3 banks in Vietnam. The stock now trades at a P/E of 6.3x.

Phu Nhuan Jewelry (PNJ VN - US$1.1 billion) is a gold merchant with its own retail shops. Vietnamese love gold, partly as a method to protect their savings from the ravages of inflation. The penetration rate of gold jewellery is already at very high levels. Still, given the success of Indian jewellery company Titan, I can see Phu Nhuan Jewelry continue compounding capital at a rapid rate. The company’s return on equity is currently 25%, probably among the strongest of any of the largest listed companies in Vietnam. The stock now trades at a P/E of 12.8x.

Vinhomes (VHM VN - US$9.3 billion) is Vietnam’s largest real estate developer. It has a massive land bank supporting its sales for at least the next 30 years. The bull case is that Vietnam’s living area per capita is currently about half that of China. The consensus 2023e P/E ratio of 6.1x looks low, but the gross margin of 57% may or may not be sustainable, depending on how land prices continue to develop.

Quang Ngai Sugar (QNS VN - US$620 million) is a sugar producer owned by the state. Its Quang Ngai province sugar mill has a capacity of 10,000 tons of sugarcane per day, which is then made into white sugar, raw sugar and liquid sugar and sold to third parties. The company has partnerships with sugarcane plantations to ensure a steady supply to its sugar mill. The stock trades at a P/E of just 9.4x.

PetroVietnam Technical Services (PVS VN - US$517 million) is a subsidiary of PetroVietnam, which provides services to the oil & gas industry - both to its parent and third parties. It does offshore engineering and construction services, deals with logistics and manpower supply, and does maintenance and repair. The return on equity has come down since 2015, most likely due to the downturn in global energy capex. The near-term P/E is 20.1x.

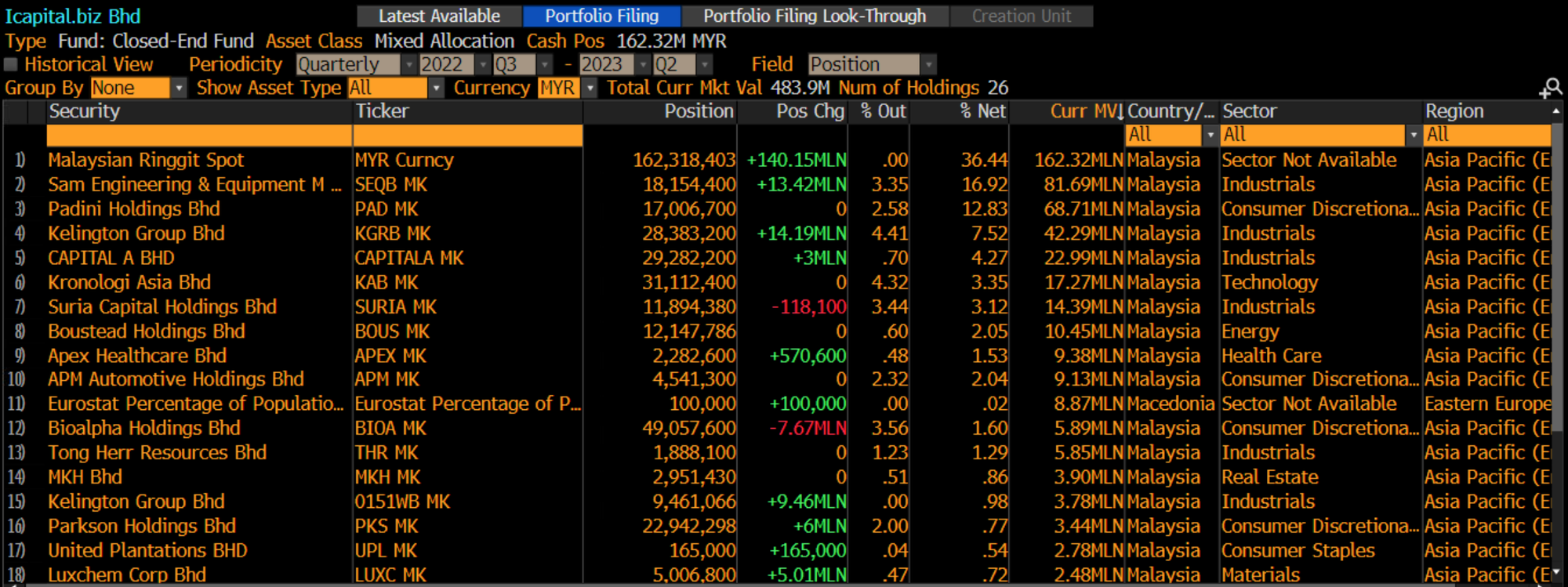

iCapital.biz

iCapital (ICAP MK - US$65 million) is a closed-end fund listed on Bursa Malaysia, which provides permanent capital to a number of sub-funds.

The manager of these funds is Capital Dynamics Asset Management. This fund manager was set up by value investor Tan Teng Boo in the mid-2000s and he has been the CIO of the fund since inception. He has a degree in economics from UCL in London and was an asset management professional before starting Capital Dynamics.

Tan’s approach is focused on value - identifying cheap stocks that have the potential to generate long-term returns. He has won a number of awards, including Best CIO at the Asia Asset Management Awards in 2012. Tan was recently interviewed by Malaysia’s FIRL Podcast here. And in November last year, he expressed optimism about Chinese stocks thinking that the zero-COVID policy might be lifted. He was proven correct in that view.

The growth in NAV per share has been around 8.0% per year vs Bursa Malaysia’s 1.8%, implying massive outperformance. But it’s worth noting that iCapital.biz trades at a significant discount to NAV of roughly 48%.

iCapital.biz currently has exposure to 26 companies, all listed in Malaysia.

Largest position Sam Engineering & Equipment (SEQB MK - US$544 million) produces precision-machined components and other related engineering services. For example, aircraft engine parts, aircraft ground support equipment, material handling equipment, etc. It also has a services arm, providing E&C services in the renewables sector. The stock trades at a modest P/E ratio of 9.6x.

Padini (PAD MK - US$600 million) is a Malaysian clothing retailer, a domestic competitor to H&M, Uniqlo and Zara. Its store brands include Padini, Vincci and Brands Outlet. Except for the COVID-19 period, the company has earned a return on equity of around 20-30%. Padini has been surprisingly nimble in the face of significant competition from multinationals. I attribute much of Padini’s success to the brilliance of its founder Yong Pang Chaun. Today, the stock trades at a P/E of just 11.4x.

Kelington Group (KGRB MK - US$213 million) is another Malaysian engineering company focusing on high-tech industries such as semiconductors and chemicals. For example, Kelington might build cleanroom facilities and ultra-high purity gas and chemical delivery systems. It’s built plants across Southeast Asia, China, Taiwan and the Philippines. The stock trades at a P/E of 20.4x, but note that the stock has been a ten-bagger since 2016. Icapital.biz was an early investor.

Capital A (CAPITALA MK - US$701 million) is the recently-renamed holding company for low-cost carrier AirAsia. While AirAsia has been seen as a Malaysian success story, the corporate structure and accounting have also been criticised by GMT Research in Hong Kong. Capital A suffered during COVID-19 and has had to issue shares and dilute minority shareholders. The company continues to be loss-making.

Kronologi Asia (KAB MK - US$91 million) is an IT services provider helping organisations store and back up their data. Its customers include financial services, healthcare, telecom operators, and government agencies. Note the weak return on equity, despite being an asset-light services business. The stock trades at a P/E of 16.4x.

Suria Capital (SURIA MK - US$96 million) is not a financial services company but rather a port operator, managing the ports of Kota Kinabalu, Sandakan and Tawau in the Malaysian province of Sabah on the island of Borneo. Other than cargo handling, it also offers freight forwarding services. The company is also involved in property development, which may explain the weak return on equity in the single digits. The stock looks incredibly cheap at a P/E of 7.7x with a dividend yield of 3.3%.

Boustead Holdings (BOUS MK - US$391 million) is a Malaysian conglomerate focusing primarily on oil palm plantations, property development, and heavy industries such as shipbuilding, defence, and aerospace engineering. It has a storied background as one of the major trading houses in the 19th century British Malaya. Boustead Holdings has quite a bit of debt, and in its most recent financial year, it made a loss. It’s not an easy company to value.

Apex Healthcare (APEX MK - US$432 million) is a Malaysian pharmaceutical company producing generics such as antibiotics, painkillers and cardiovascular drugs. It has a medical devices division, which produces diagnostic and monitoring equipment such as blood glucose monitors and blood pressure monitors. The return on equity has been in the mid-teens, with slow but steady earnings growth. The P/E is currently 13.6x, with a dividend yield of 2.0%.

APM Automotive (APM MK - US$88 million) produces automotive parts and accessories such as seating systems, interior and exterior trims, acoustics and electrical systems. It’s part of the Tan Chong Group, which owns auto dealerships and a number of other distribution businesses. While APM Automotive is based in Malaysia, its clients include most major global automakers. After a tough period during COVID-19, presumably due to weak production output of vehicles globally, earnings are recovering. But the stock remains down 60% since its peak in 2014. APM Automotive’s near-term P/E is 14.9x.

Bioalpha Holdings (BIOA MK - US$37 million) sells health supplements, herbal teas and such. The company tagline is “Health Through Biotech”. It sells its products online through distributors and owns a retail chain where it sells its products. I find it difficult to judge the quality of Bioalpha’s health supplement - whether there is a scientific basis for their claims about their anti-ageing properties, for example. The company is loss-making but trades at 3.8x EV/Sales.

Tong Herr Resources (THR MK - US$107 million) is involved in the production of stainless steel fasteners such as bolts, nuts, screws, etc. They’re used in construction, automotive, electronics and manufacturing. The P/E ratio is 5.8x, but earnings seem surprisingly volatile.

MKH (MKH MK - US$176 million) is a Malaysian property developer focusing on properties across the spectrum from residential to commercial, industrial and infrastructure projects. It has many townships in Malaysia with related facilities and also builds landed properties and condominiums. The trailing P/E ratio is 3.5x.

Parkson (PKS MK - US$38 million) is a fallen angel, suffering from its exposure to department stores that have lost out to more modern shopping malls and other modern retail concepts. It had a large exposure to the Chinese department store industry. But without ownership and with falling revenues, it had to break leases and reduce its footprint. Today Parkson is unprofitable and only operates a handful of stores in Malaysia, Vietnam, Indonesia and China.

United Plantation (UPL MK - US$1.6 billion) is one of Malaysia’s best-managed plantation companies, partly owned by Danish conglomerate UIE. The business is vertically integrated, with plantations, infrastructure and refining all within the group's ownership, making the business an efficient operation. The stock trades at a P/E of 12.1x, below its historical average of around 18x. I wrote about United Plantations here.

Luxchem (LUXC MK - US$121 million) distributes chemicals in Malaysia, including solvents, industrial gases, resins and pigments. It also has a property development arm that does commercial and residential projects. The stock trades at a P/E of 3.0x.