Update: IMAX China (1970 HK)

The leader in cinema equipment at 9x P/E

Disclaimer: Asian Century Stocks uses information sources believed to be reliable, but their accuracy cannot be guaranteed. The information contained in this publication is not intended to constitute individual investment advice and is not designed to meet your personal financial situation. The opinions expressed in such publications are those of the publisher and are subject to change without notice. You are advised to discuss your investment options with your financial advisers and to understand whether any investment is suitable for your specific needs. From time to time, I may have positions in the securities covered in the articles on this website. Full disclosure: I do not hold any position in IMAX China when publishing this article. Note that this is a disclosure and not a recommendation to buy or sell.

Last year, IMAX Corporation's Richard Gelfond was accused of excessive drinking and cocaine use. And this year, he took two months of medical leave, supposedly to treat pneumonia.

In a normal year, I wouldn't have paid much attention to the latest rumors about a coming takeover. But given Richard Gelfond's poor health, a takeover suddenly seems plausible, though as one of many possible scenarios.

1. Quick recap

I first wrote about IMAX China (1970 HK - US$353 million) back in early 2024:

Michael Fritzell

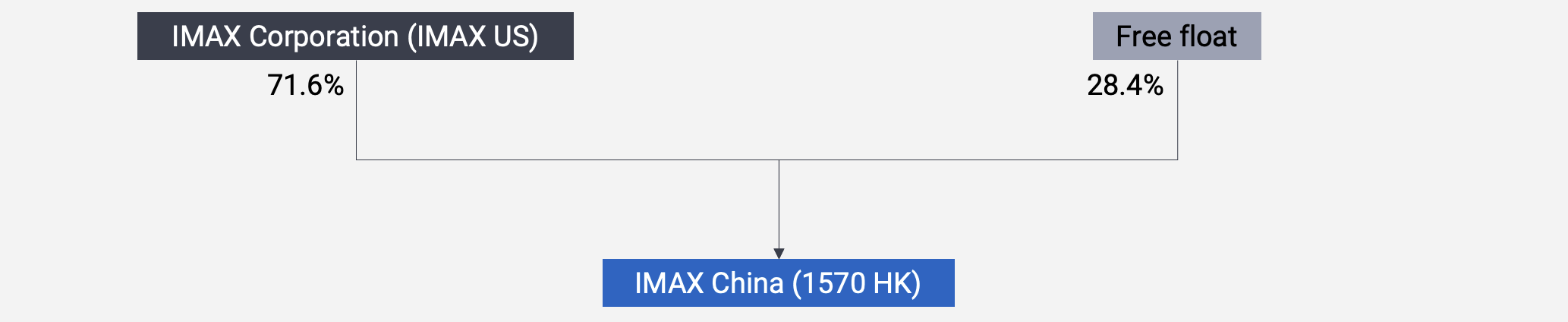

Michael Fritzell- It's a publicly listed subsidiary of cinema equipment company IMAX Corporation (IMAX US - US$2.1 billion).

- While the parent company, IMAX Corporation, manufactures the equipment, IMAX China has the exclusive right to sell it in the Greater China region, including Mainland China, Hong Kong, Macau, and Taiwan.

- IMAX Corporation was acquired by a group of investors in 1994 in a leveraged buyout. That group included Richard ("Rich") Gelfond, who remains the company's CEO.

- IMAX's core product is equipment for high-end cinemas. These cinemas use special IMAX standards for screen sizes, an unusual 1.43:1 aspect ratio, steep seating arrangements, high-resolution images, and top-tier sound systems.

- Movies made for IMAX – including the movie "Dune" – are shot on large-format digital cameras that provide greater detail for the viewer:

- Note that IMAX doesn't own any cinema screens. It simply provides the equipment and receives recurring income from maintaining it, as well as fees for converting movies into the IMAX format.

- Given that an IMAX ticket costs around 50% more than a normal ticket, it ends up being a profitable deal for all parties involved, including the exhibitor. And IMAX China itself has been profitable, with operating margins above 40% and strong free cash flows.

- The IMAX brand name is incredibly strong, especially in Mainland China. It's almost become synonymous with a high-end cinema experience.

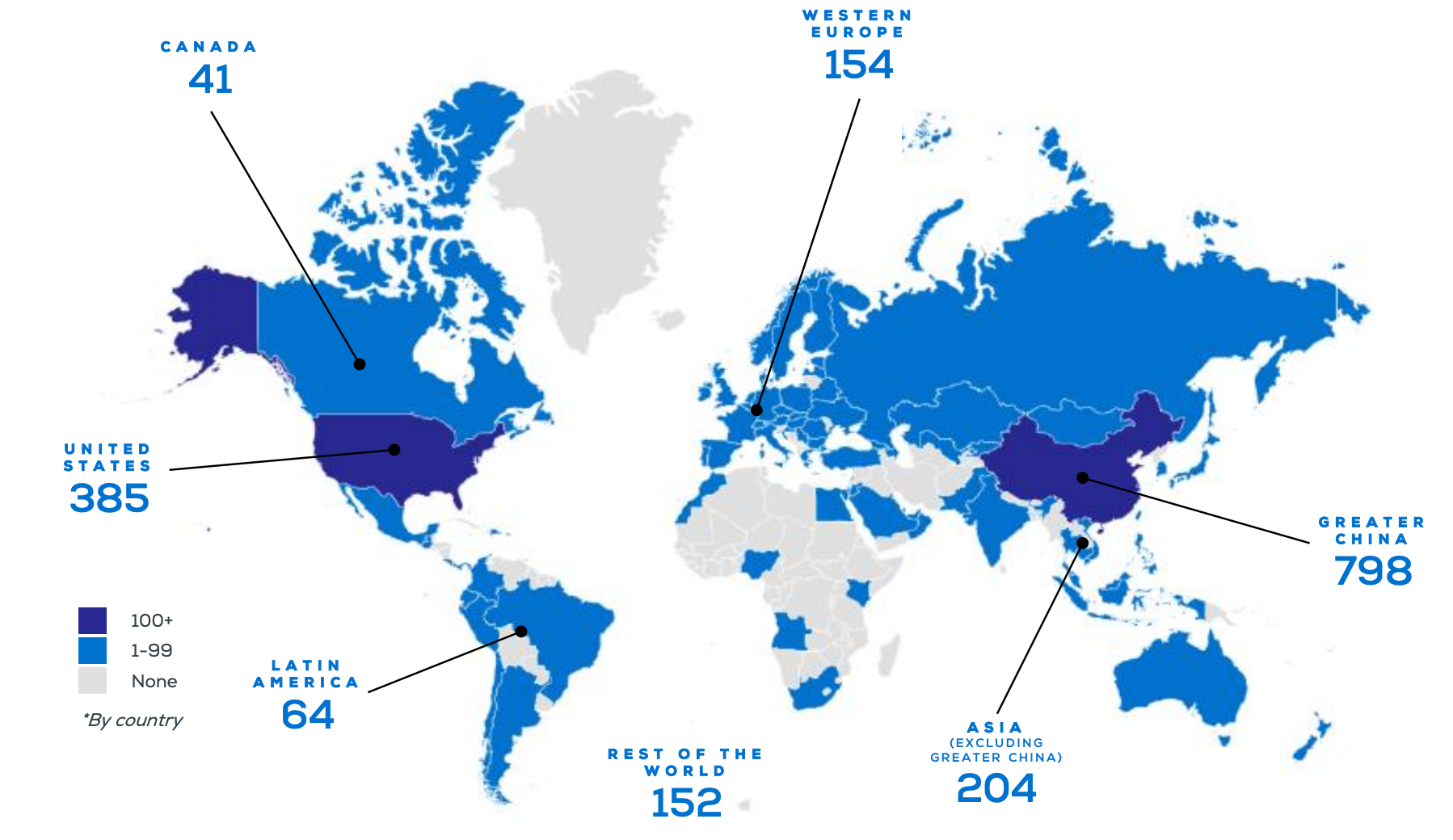

- IMAX serves about 800 screens in Greater China — more than twice as many screens as in the United States. This critical mass drives studios to produce IMAX-compatible movies – or else they'd lose out on a big chunk of the market.

- At the time of publishing my first report, the share price had been on a long downward trajectory since the 2015 IPO. At that time, a large part of IMAX China's revenues were construction-related. And as construction declined, all that remained were recurring revenues such as revenue-sharing agreements, film conversion fees, and equipment maintenance revenues.

- In 2024, I was hopeful that China's movie industry would recover from COVID-19. I felt that a big part of the issue was that Hollywood movie production had slowed down during the pandemic. And that once the output recovered, we would see people return to cinemas.

- IMAX China traded at 7.5x P/E at the time, with net cash equivalent to 20% of the business's market capitalization. And that was with a share price almost identical to today's.

2. The failed takeover

In 2023, IMAX China's parent company, IMAX Corporation, bid HK$10 per share in a proposed privatization. But as more than 10% of minorities opposed the deal — a key hurdle for Hong Kong privatizations — it ultimately failed.

In response, IMAX Corporation's CEO Richard Gelfond expressed disappointment but emphasized that it remained fully committed to the Chinese market.

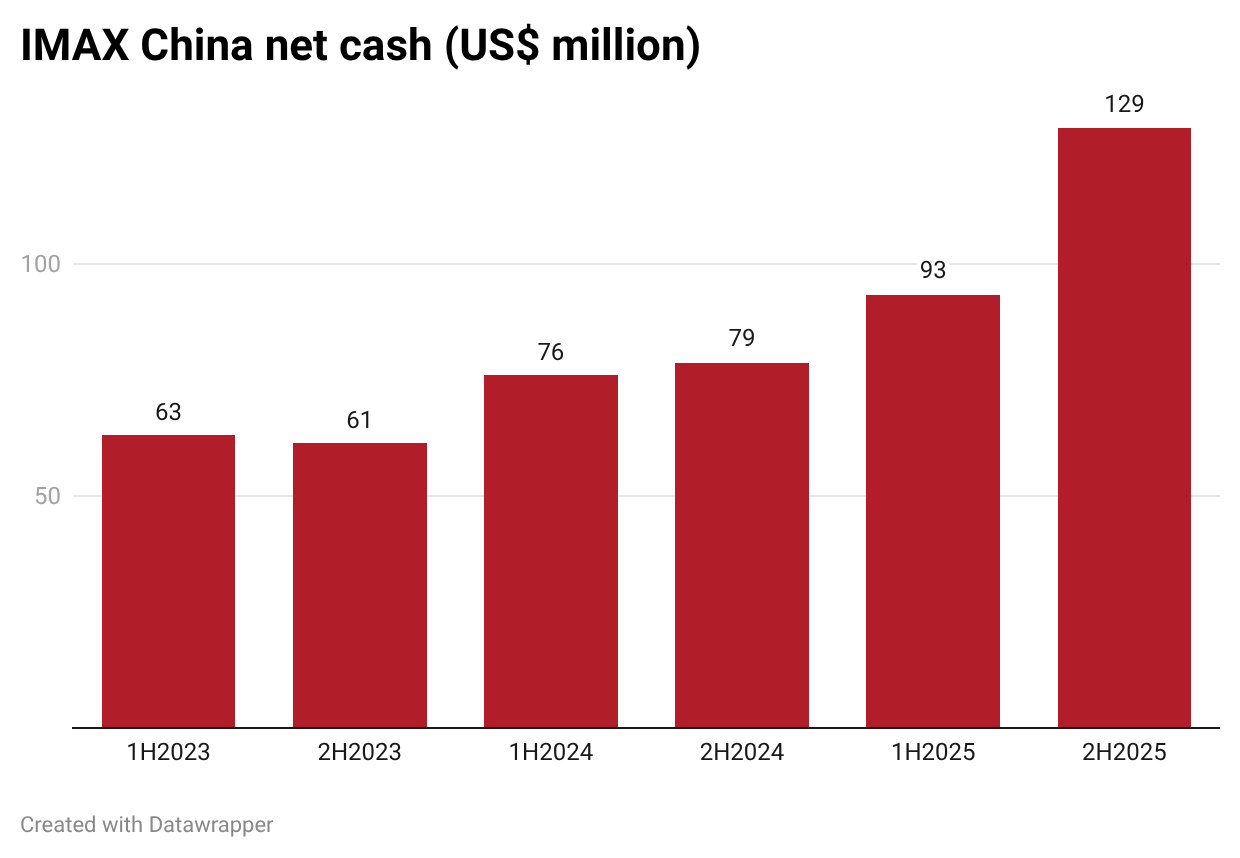

However, corporate governance issues began to emerge. IMAX China soon announced it would cut its dividend. And the already-high net cash position in IMAX China continued to build.

The lack of dividends was unfriendly to minorities, to say the least.

In an update, I hypothesized that a second bid could come as early as October 2024, given the 12-month moratorium on placing new bids:

There were plenty of reasons to think that a new bid could be forthcoming. Most importantly, Gelfond said in an early 2024 earnings call that "it would be nice" to take IMAX China private:

“Are we going to try and privatize it? Again, and we can't go back until much later this year. But we haven't made a decision yet what to do. I think it will depend on China's financial performance, what IMAX's liquidity looks like and then how the Chinese shareholders feel about [it]. I'll make the decision just reminding everyone that wasn't had to do. That was – it would be nice if we could do it. But even though we didn't get it done in the way we want it, we've realized some of those savings along the way by being strategic about how we manage our costs there.”

So the situation seemed unsustainable. Cash kept building on IMAX China's balance sheet, while Gelfond clearly wanted to take the company private. Would his wishes eventually come true? Or would another suitor emerge to eventually acquire the entire group, including IMAX China?

3. The post-COVID recovery