Thailand's stimulus package

The Bhumjaithai Party's impact on economic growth and Thai equities

Hi! I'm Michael Fritzell. Welcome to another free-to-read edition of Asian Century Stocks – a newsletter about Asian value stocks. First time reading? Sign up here. For a complete list of all previous posts, check out the Table of Contents.

In his latest Gloom, Doom & Boom report, Marc Faber revealed that he is accumulating Thai property stocks, which tend to be sensitive to the credit cycle.

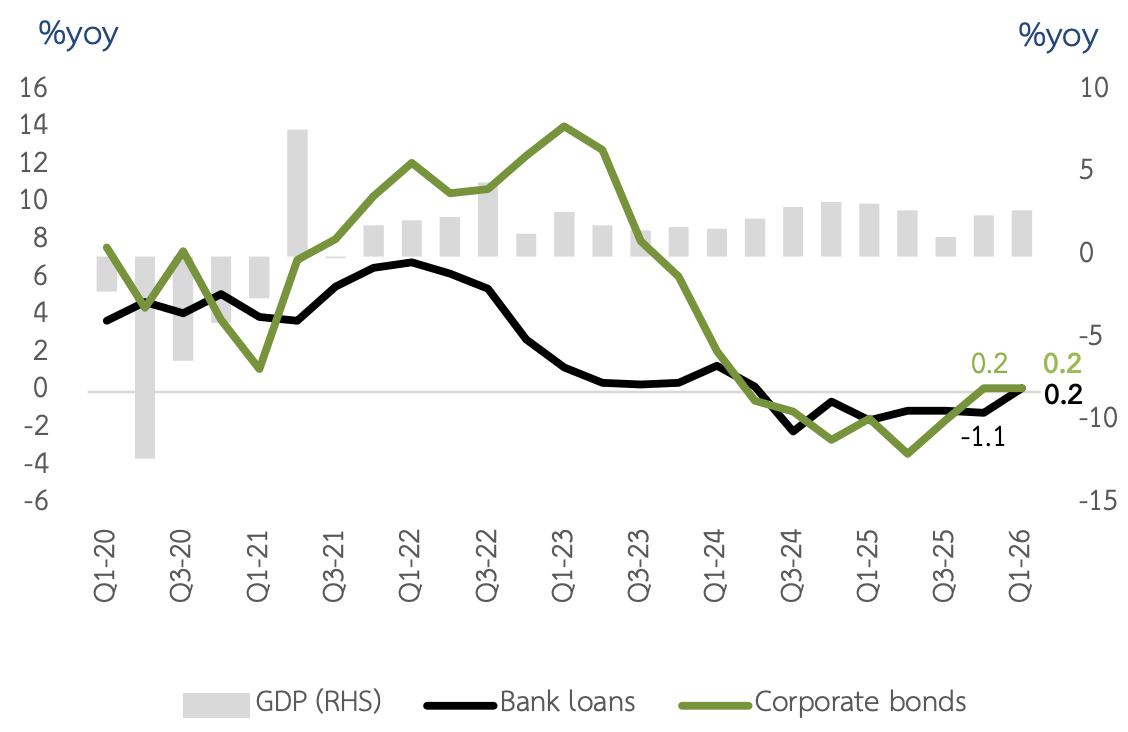

Thailand has been suffering from a multi-year downturn in credit growth:

However, there are signs that the credit cycle is finally turning. The new Bhumjaithai government is pushing for a THB 400 billion stimulus package. And loan growth finally turned positive in the first quarter of 2026.

I'll discuss the Thai macro backdrop, why the cycle might be turning and what type of companies might be benefitting from a turnaround.

1. The Bhumjaithai victory

Historically, Thai business has been dominated by an elite closely connected to the royal family and the Thai military.

In 2001, a businessman called Thaksin Shinawatra became Prime Minister by appealing to rural voters through cash handouts and other populist policies.

But the elite eventually struck back. Thailand had several military coups, with riots between military-backed "Yellow Shirts" and Thaksin-backed "Red shirts.

Thaksin fled to the UK and spent more than a decade in exile. In his absence, his Pheu Thai party has served as a proxy for him. And several of his family members served as Thailand's Prime Minister.

Since 2018, Thailand's elite has been further challenged by a new party called Move Forward, later renamed the People's Party. This party became popular on the back of its promises to break up Thailand's monopolies, including the companies that make up a large portion of the Stock Exchange of Thailand. A People's Party victory would not be positive for stocks in the short run.

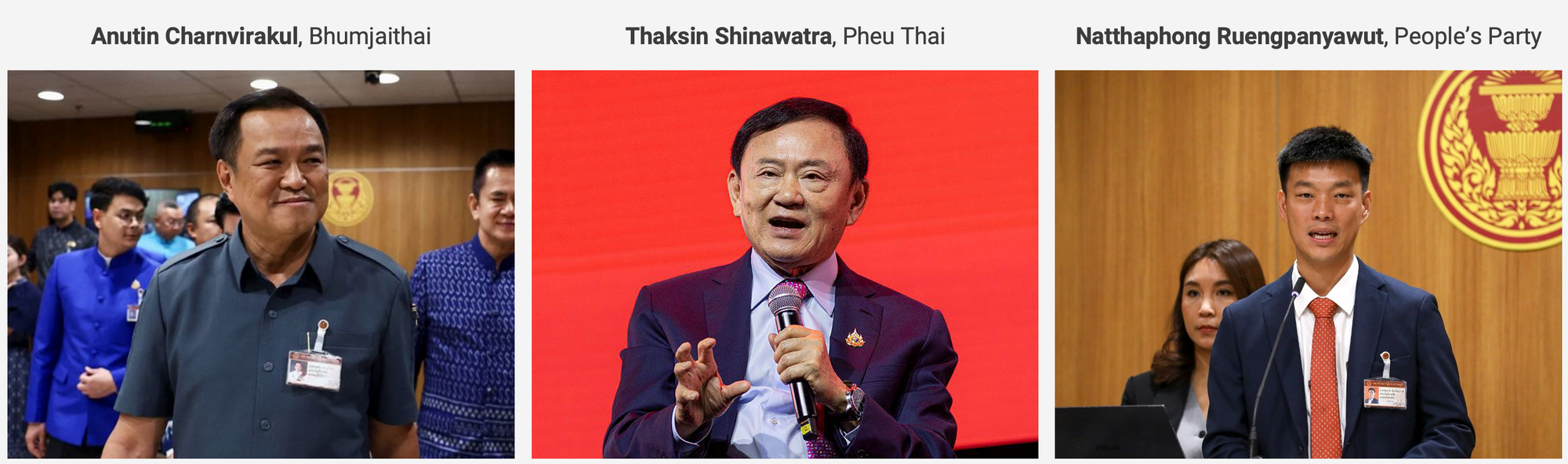

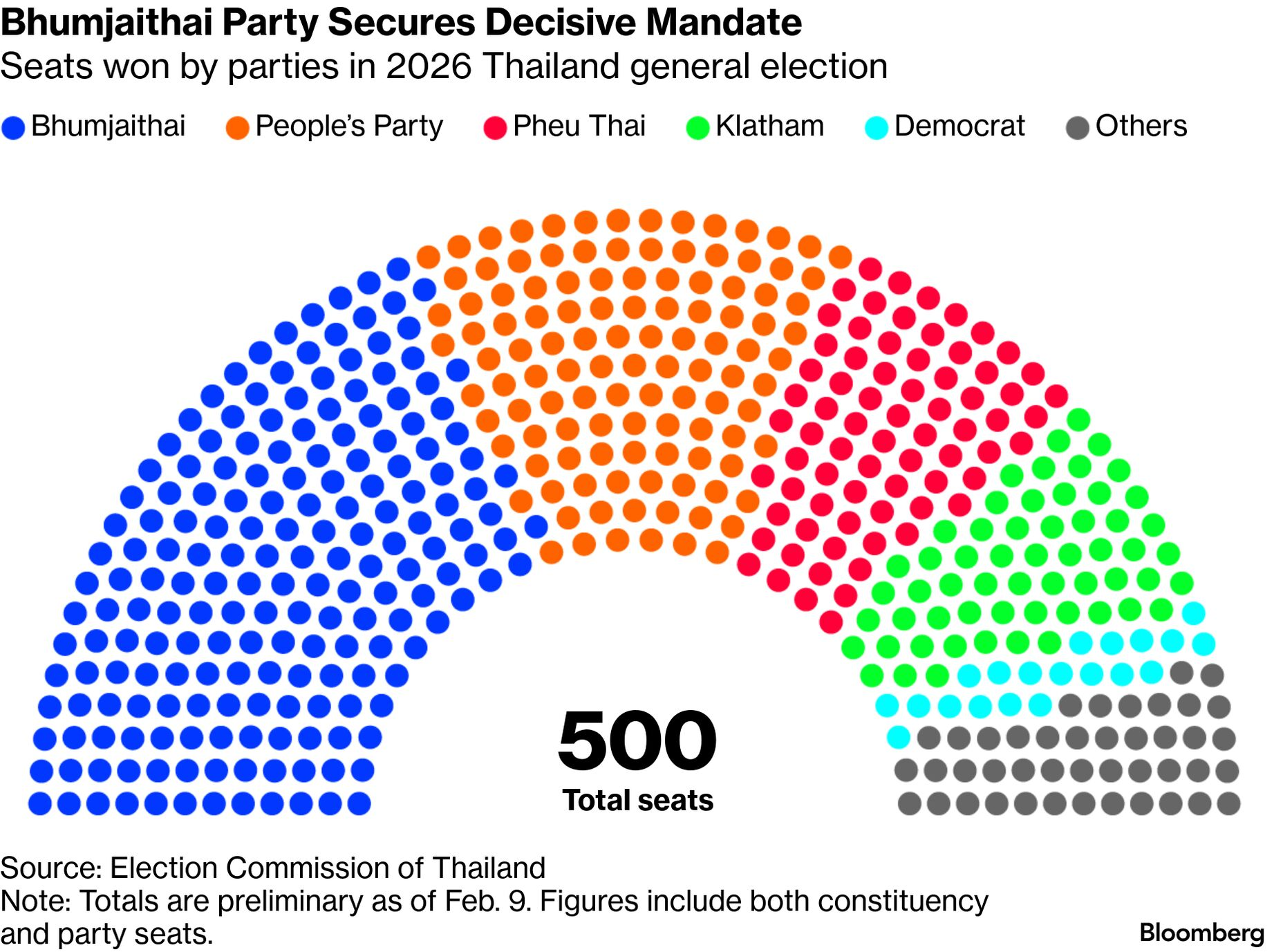

In February 2026, Thai voters went to the polls again. The election was a fight between these three forces: the military-aligned Bhumjaithai party, Thaksin-connected parties and the reformist People's Party.

The Bhumjaithai Party won in a landslide, taking 192 out of the 500 seats in the House of Representatives.

So Thailand now has a new government controlled by the Bhumjaithai party and its supporters, including the military and the tycoons that are running many of Thailand's publicly-listed companies. And that should actually be positive for stocks, as the government is now pro-business.

2. The Thai credit picture

For over two years now, Thailand has been in a long, messy, bad-debt clean-up cycle. Household debt is close to 90% of GDP, of which a significant portion is unsecured non-mortgage debt. And nominal GDP growth has been so slow that the debt burden has not declined materially.

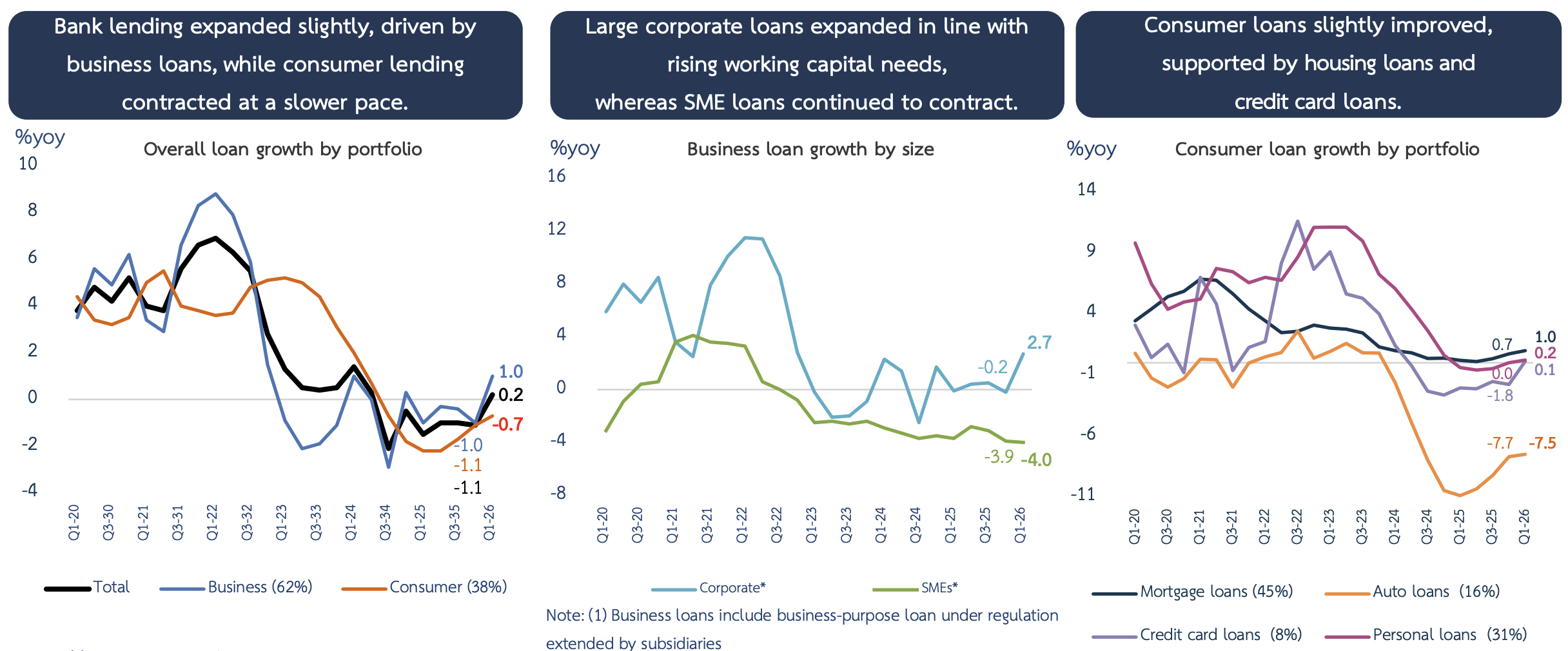

So we've seen a decline in credit growth, especially in auto loans and small and medium-sized enterprise loans:

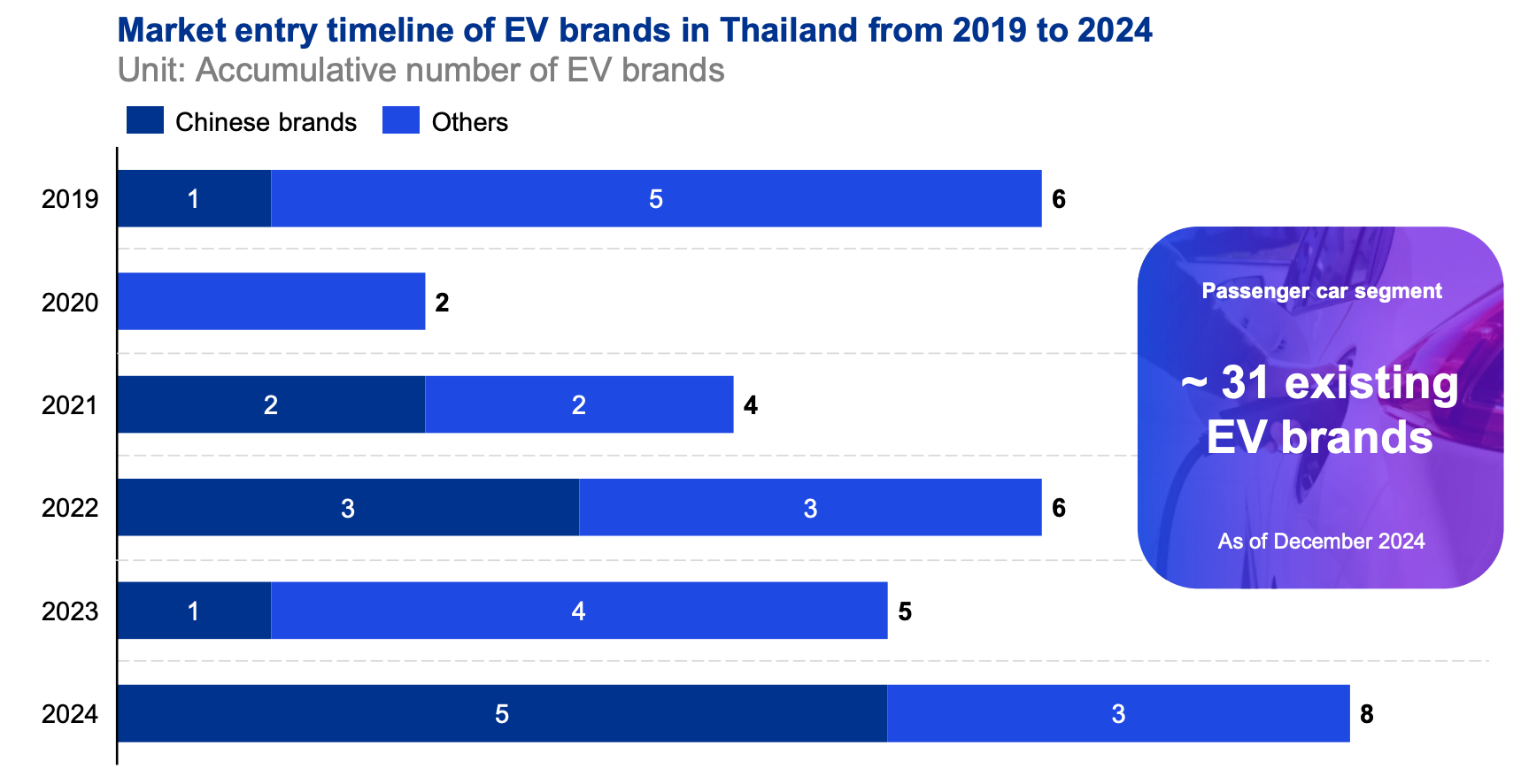

When it comes to auto loans, the decline is due to a price war initiated by Chinese electric vehicle manufacturers like BYD, causing second-hand prices to plummet. Keeping loan-to-value ratios fixed, lenders have had to reduce ticket sizes.

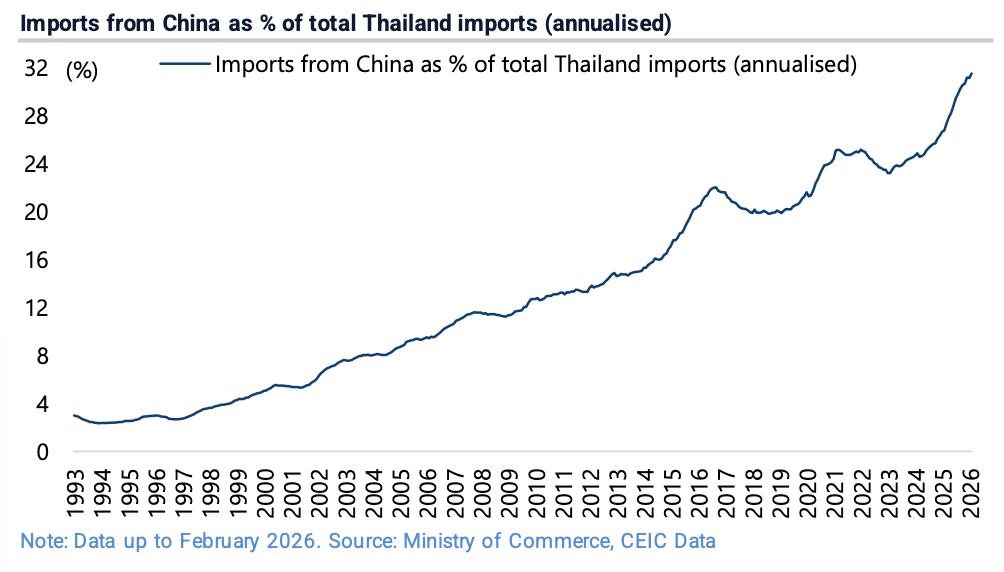

In the SME segment, credit growth has weakened due to general economic malaise. It could be due to competition from Chinese imports. In early 2026, Chinese imports grew +42% year-on-year, according to strategist Chris Wood at Jefferies:

In addition, while tourism from Europe has recovered, tourism from China has not. And there's plenty of anecdotal evidence that small businesses like local restaurants are suffering. They never fully recovered from the COVID-19 pandemic.

The property sector has been weak as well. The government has tried to help with 100% loan-to-value ratios, but developers are still facing weak demand with high mortgage rejection rates. It's ultimately due to poor creditworthiness among borrowers.

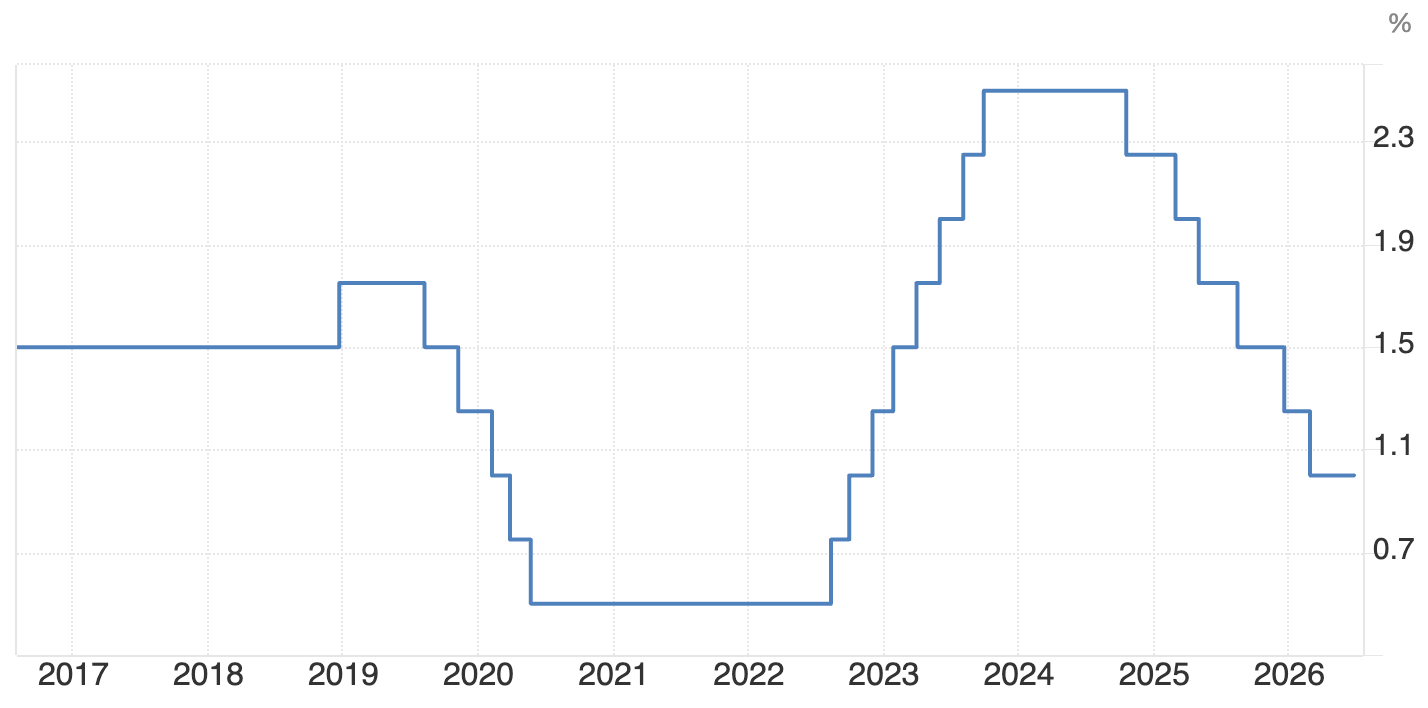

The property market should have benefited from the recent decline in Thai interest rates:

But we haven't seen much of an impact on either credit growth or property transaction volumes.

That's why I think it's encouraging to see the Bhumjaithai party now push for economic stimulus. Most importantly, it's targeting a THB 400 billion (US$12 billion) stimulus program, equivalent to 2% of GDP. This program includes:

- A so-called SME Credit Boost scheme is meant to support new loan issuance through 2026

- The Clear Debt, Move Forward Plus program to restructure non-performing loans

- Khon la khrueng ("half-half") consumption subsidies to 30 million people

The Thai government has been constrained by its 70% public debt ceiling. But new Finance Minister Ekniti Nitithanprapas is pushing for the debt ceiling to be raised to 75%. That would be negative for the Thai Baht, but certainly positive for credit growth.

3. Stocks affected by the reforms

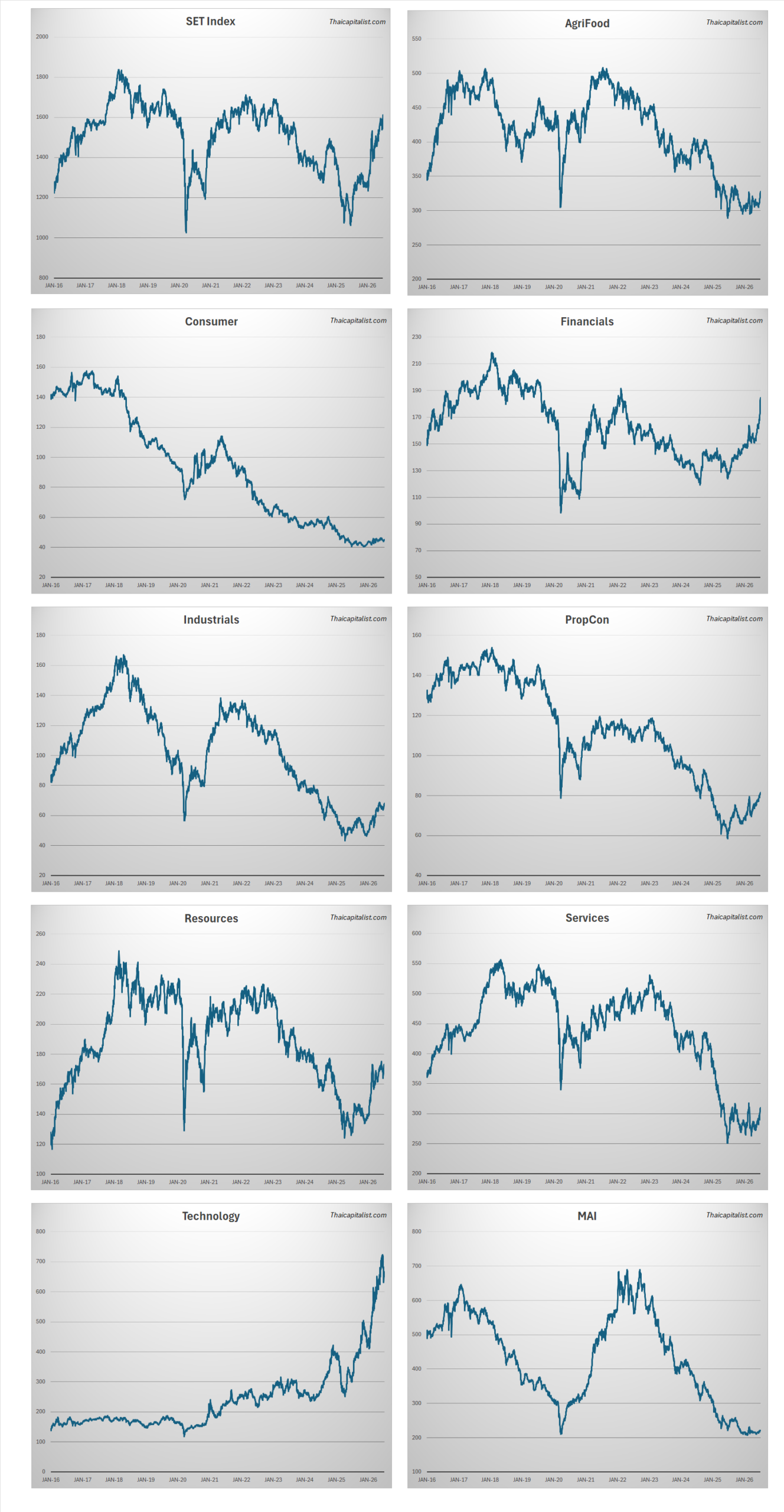

Thai stocks continue to trade at low multiples. This chart from Pon at Thaicapitalist.com shows that while the SET Index has recovered nicely, that recovery has been driven mostly by tech stocks like Delta Electronics Thailand and financials:

Consumer stocks remain depressed, as do many industrial stocks.

So who will benefit from the stimulus program? First, SME-focused lenders such as Thai Credit Bank should see their credit growth accelerate.

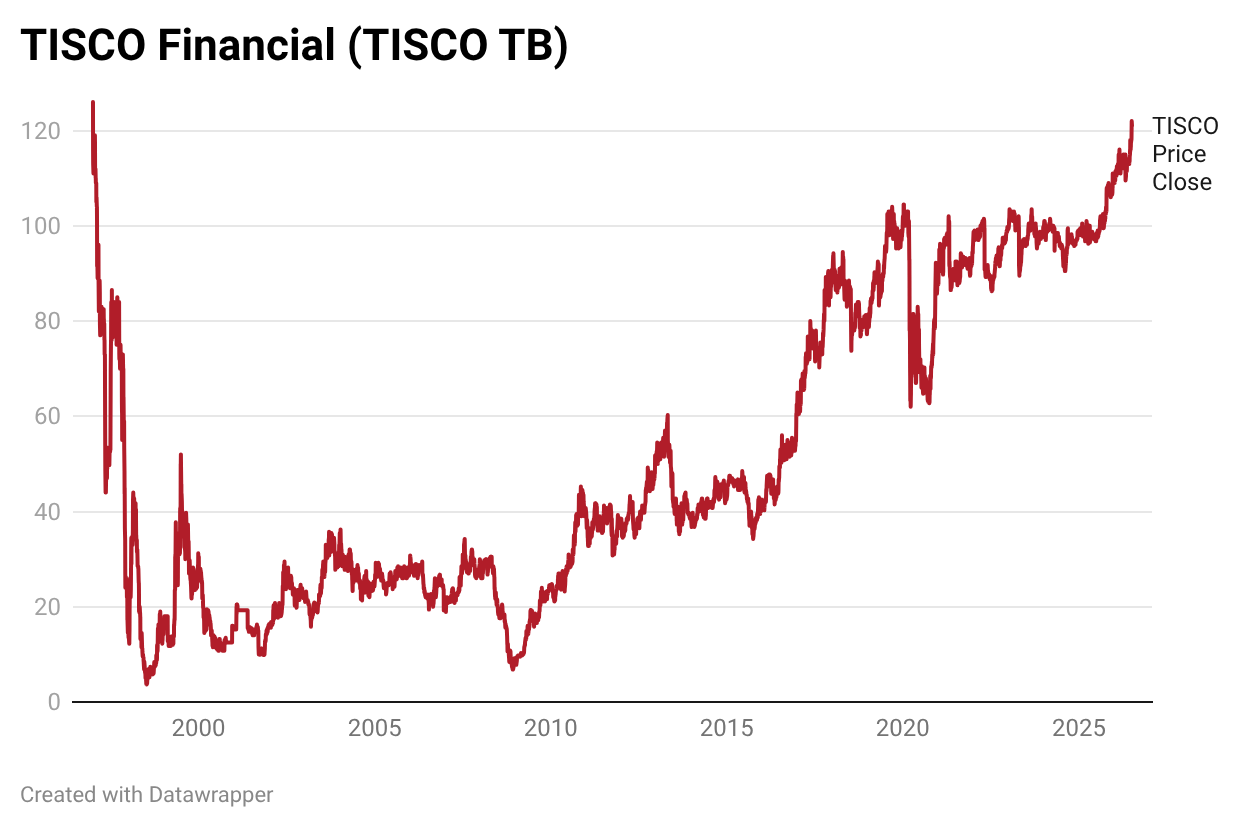

As noted by banking analyst Daniel Tabbush, many of Thailand's finance companies including TISCO and Thanachart Capital benefit from this lower interest rate environment as they primarily rely on wholesale financing rather than zero interest bank deposits.

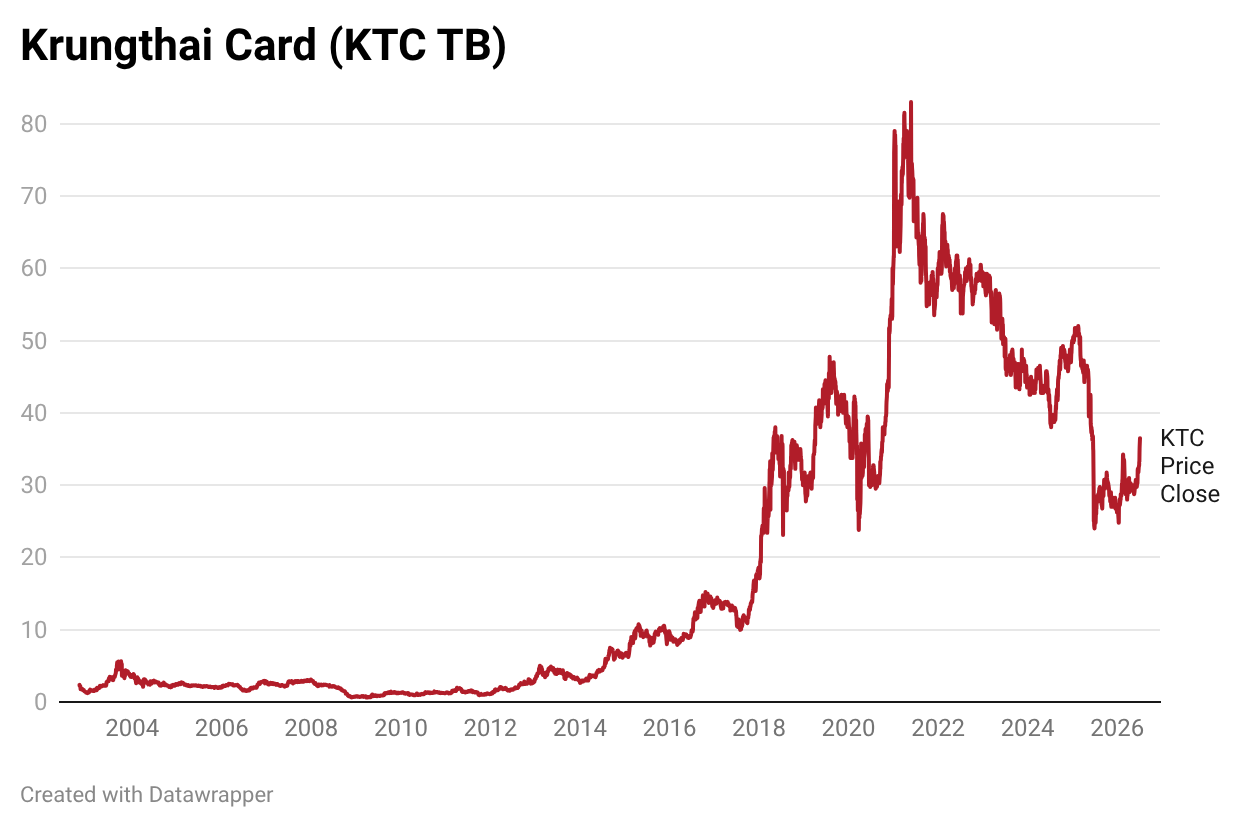

The same is true for credit card lenders like Krungthai Card. They enjoy fixed, regulated yields, while benefiting from lower interest rates.

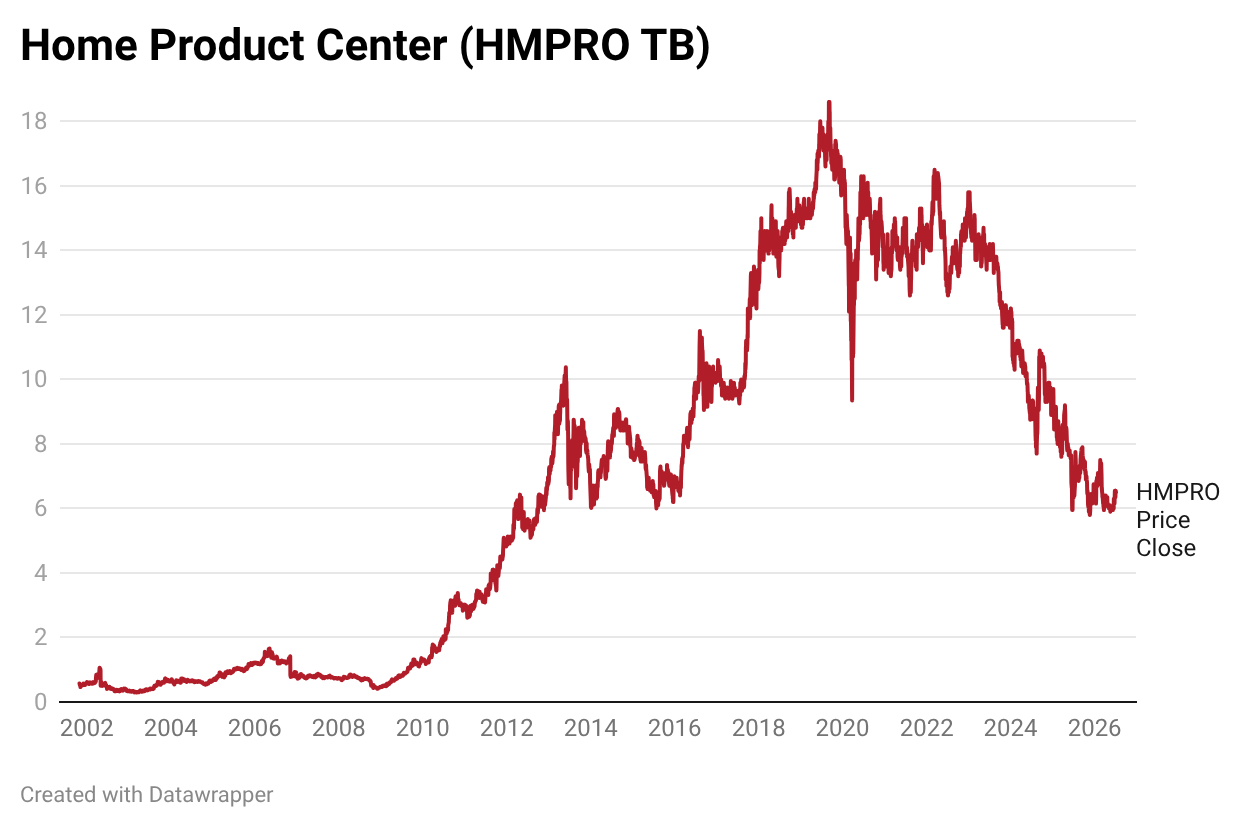

The new consumer subsidies should benefit companies like 7-Eleven store operator CP All, energy drinks company Carabao, seaweed snack company Taokaenoi, home improvement retailer HomePro, cinema operator Major Cineplex, and so on. Though I doubt the subsidies will really move the needle for any of them. (Full disclosure: I own shares in both Carabao and Major Cineplex)

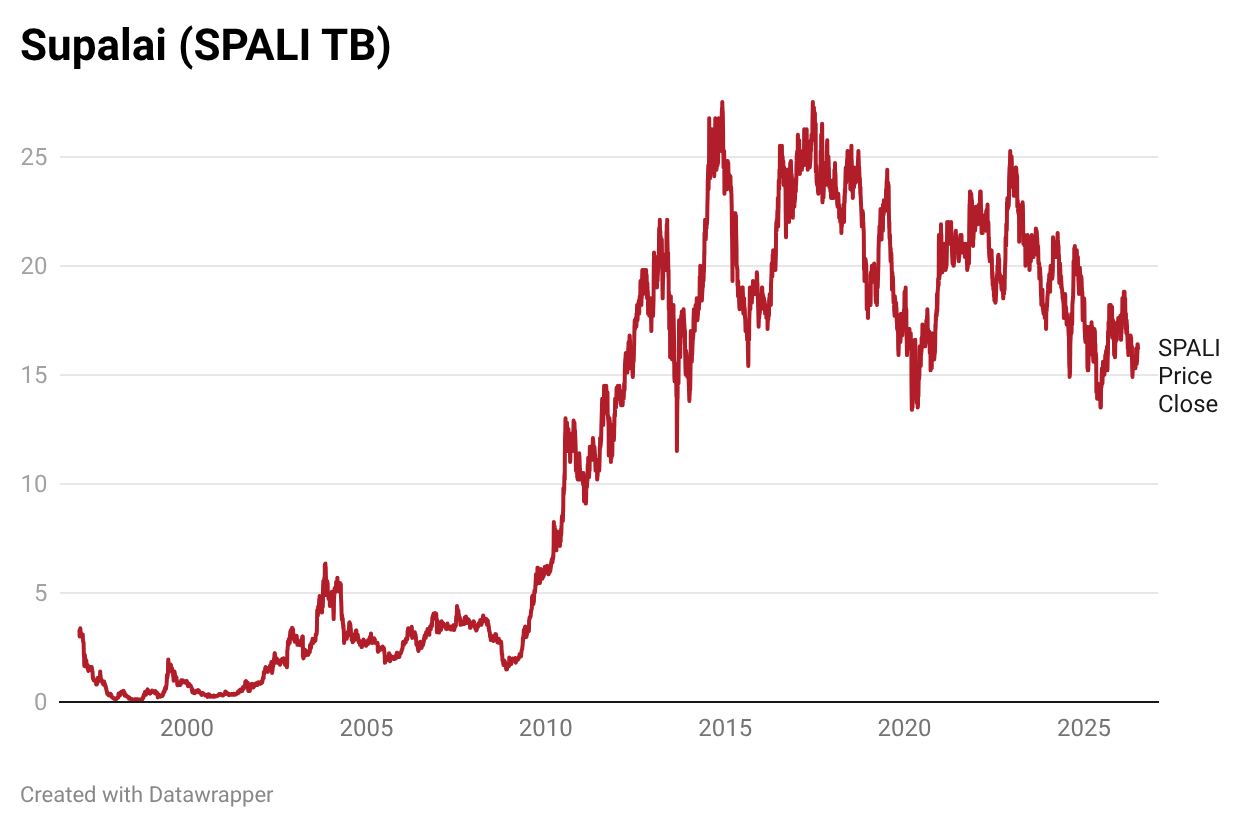

There will also be support for the property market. The government just extended 0% transfer and mortgage registration fees (usually 3%) through mid-2027. That should help on the margin. A restructuring of non-performing loans, consumption subsidies and lower interest rates will help too. Especially for mass-market developers like Supalai.

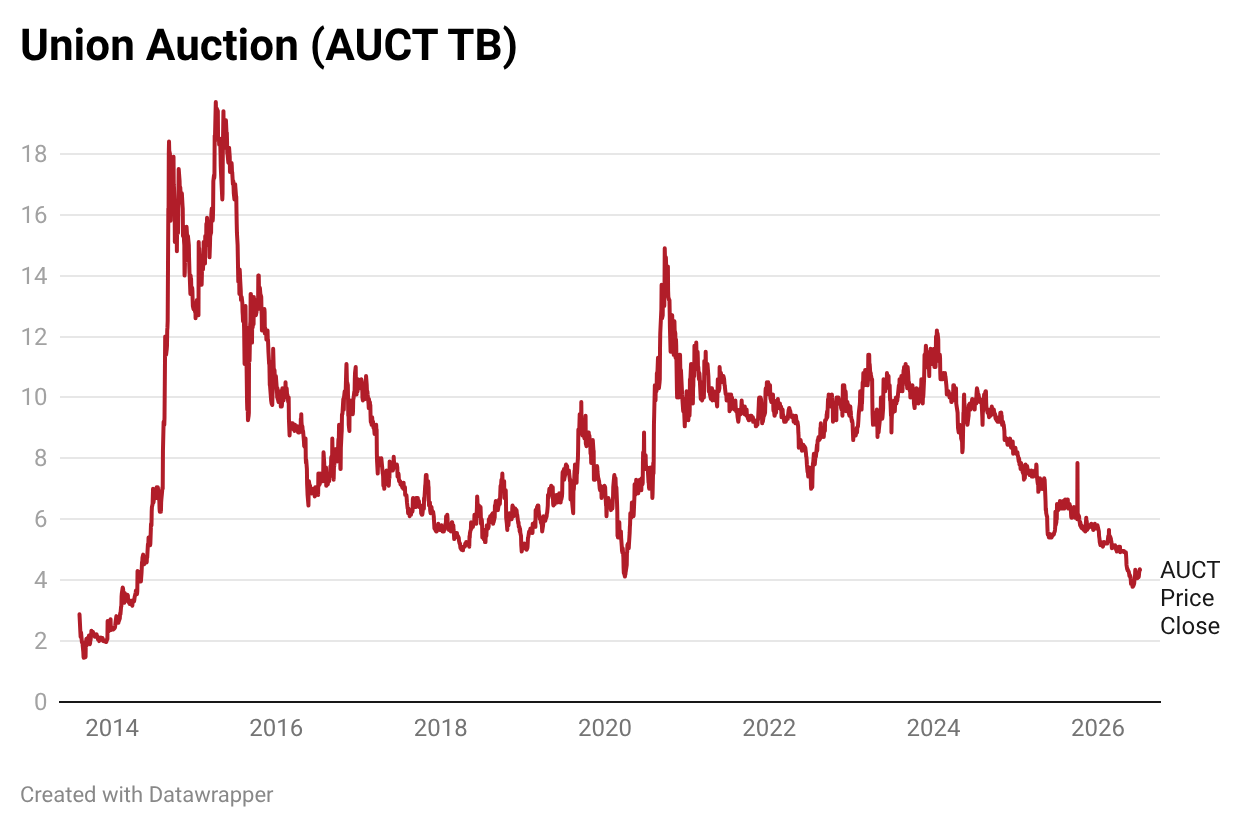

On the negative side, I think the restructuring of non-performing loans will be unfavorable to distressed-debt buyers like JMT Network and Bangkok Commercial Asset Management. And since there will be fewer vehicle repossessions, Union Auction will be hit, too.

4. Conclusion

It's still possible that Thailand's constitutional court will rule the emergency decree illegal, in which case the THB 400 billion stimulus program will have to be shelved.

But the new government seems determined to stimulate the economy. I expect the debt ceiling to be raised and for government borrowing to counteract the negative effects from weaker auto and SME borrowing. That should be positive for liquidity, and positive for stocks.

I do think the headwind from Chinese imports is structural. The Thai government has responded by removing the de minimis threshold for e-commerce packages. And the EV subsidies have been partially removed. But I expect the proportion of Thailand's imports from China to continue to go up.

I am not convinced that the Thai housing market has turned. Developer Supalai's forward guidance has not yet turned positive. But finance companies that rely on wholesale financing, including Krungthai Card, should benefit from government support and the ongoing decline in Thai interest rates.

And since non-performing loans will likely be restructured, vehicle repossessions will be pushed forward, causing the recovery for Union Auction to be delayed another year or two.