Portfolio update August 2022

Slow but steady gains as most of Asia's economies recover from COVID. Estimated reading time: 19 minutes.

Disclaimer: This article constitutes the author’s personal views only and is for entertainment and educational purposes only. It is not to be construed as financial advice in any shape or form. Please do your own research and seek your own advice from a qualified financial advisor. From time to time, the author may hold positions in the below-mentioned stocks consistent with the views and opinions expressed in this article. I have positions in all of the below stocks at the time of publishing this article. This is a disclosure - not recommendations to buy or sell stocks.

Portfolio update

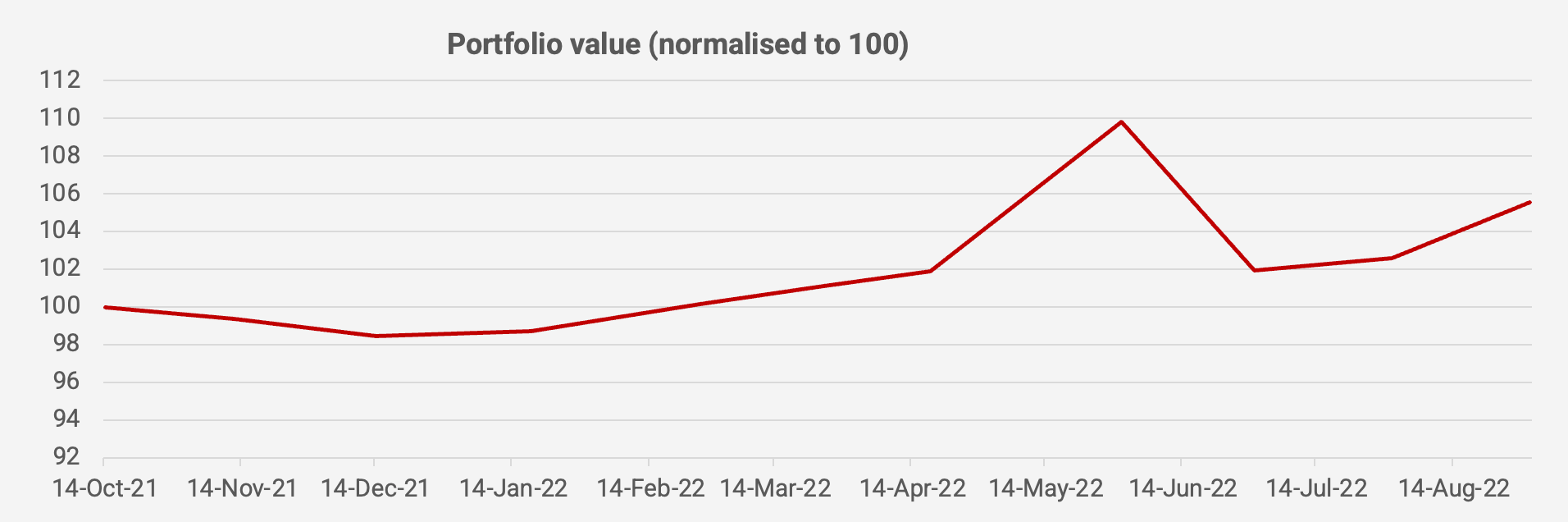

August was a good month for the portfolio, up +2.9% vs late July and +5.6% since its inception in October 2021 - all in US Dollar terms.

The strength of the US Dollar continues to be a headwind for EM and Japanese assets. But I don’t have a strong view of the future direction of the dollar.

What I am certain about is that fundamentals are improving across the broad buckets of COVID-19 recovery stocks, travel stocks as well as energy and agricultural commodities.

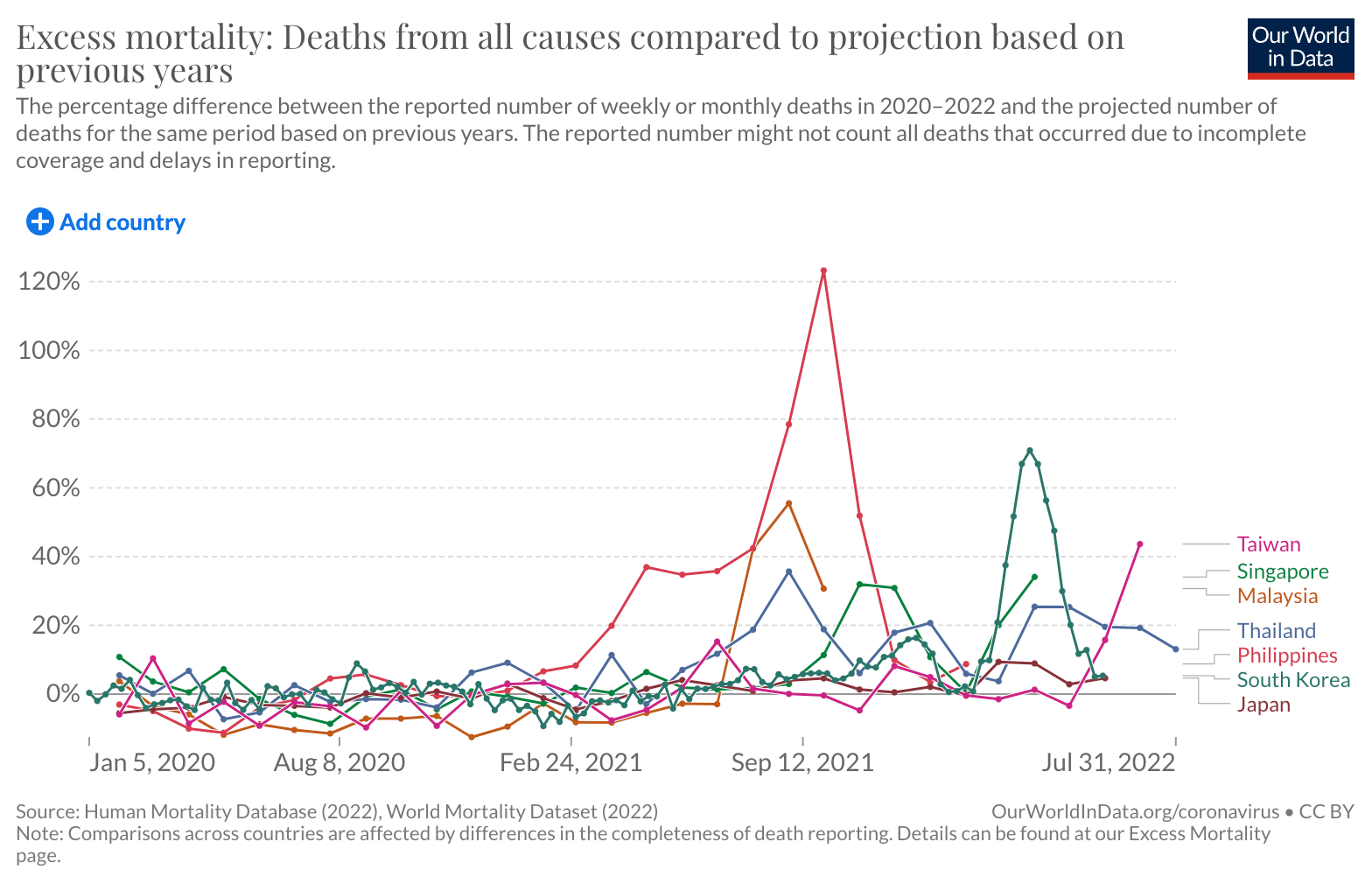

Some investors I’ve spoken to worry about the BA5 outbreak. My response is usually that countries that have let the virus “rip” - including my home country of Sweden - are now seeing almost complete normalisations of their economies. And countries within Asia that have had lax COVID-19 policies, such as the Philippines, are now starting to see excess mortality go down to zero. So it looks like we’re nearing the end of the pandemic - at least in economic terms.

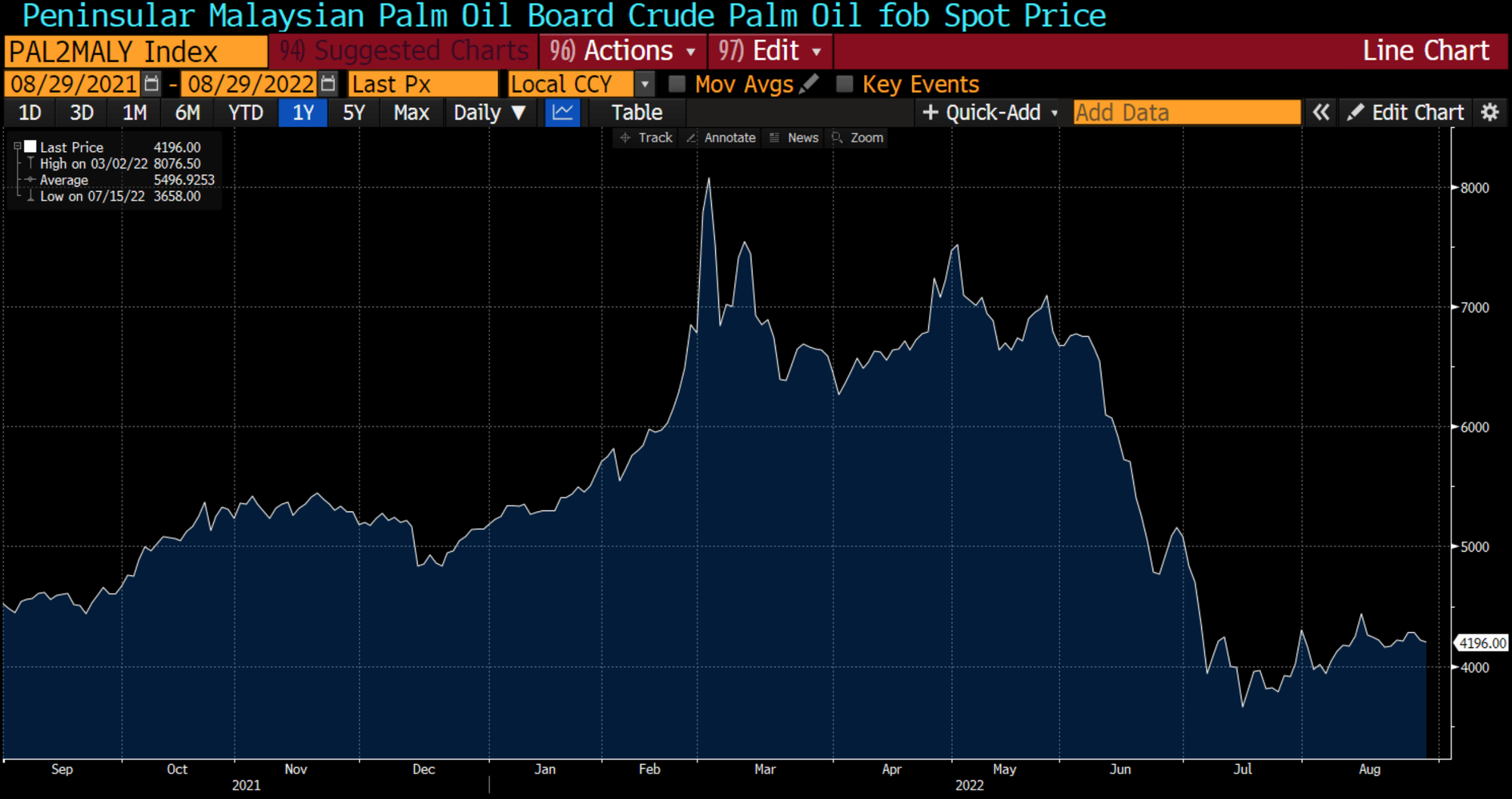

I’m bullish on palm oil. The spot price is now slowly creeping up again after Indonesia’s shock decision to waive export levies for several months. I expect the spot market to firm up gradually over the next few months. If the levy is re-introduced in November, then global supply will become tight yet again.

I’m also constructive about crude oil. The Brent crude oil price for 2025 delivery remains at the US$76/barrel level, despite all the talks about a coming US recession. US strategic petroleum reserve releases will end in about 2 months. OPEC’s spare capacity is limited. That’s why I’m comfortable owning CNOOC for now.

Here is my Asian portfolio as of 30 August 2022: