Portfolio update December 2021

Estimated reading time: 9 minutes

Disclaimer: This article constitutes the author’s personal views only and is for entertainment purposes only. It is not to be construed as financial advice in any shape or form. Please do your own research and seek your own advice from a qualified financial advisor. From time to time, the author may hold positions in the below-mentioned stocks consistent with the views and opinions expressed in this article. I have positions in all of the below stocks at the time of publishing this article. This is a disclosure - not recommendations to buy or sell stocks.

Portfolio update

Here is the second update to the Asian Century Stocks portfolio introduced to you in October 2021.

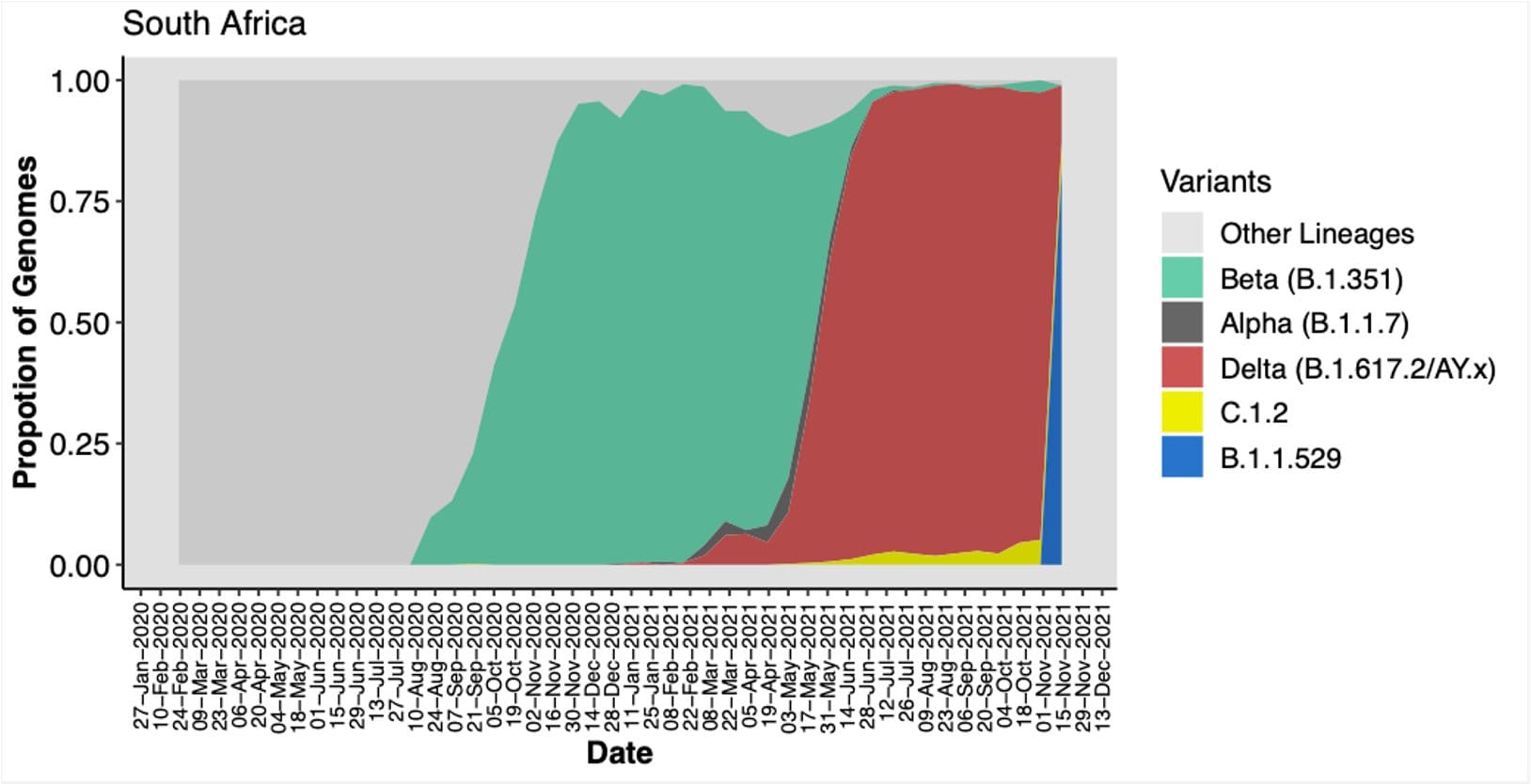

On 26 November, I sold a significant portion of the portfolio due to precautionary measures of the rapidly spreading B.1.1.529 variant.

I noticed that the new variant had outcompeted the Delta variant in South Africa’s Gauteng province. Its transmissibility was far higher than anything I had seen in the past, as can be seen from the following chart:

The chart made nervous. It gave me a feeling of déjà vu, having seen a similar scenario play out with the Delta variant in early 2021.

On the morning of 26 November, I therefore sold shares in the following companies:

- Bloomberry Resorts. I believed that new travel restrictions would be imposed

- SATS. I thought that Singapore’s government would likely follow the UK’s example of putting in new travel restrictions

- Daiichikosho: A highly transmissible variant would likely lead to karaoke bar restrictions

- Pico Far East: I had a hunch that China’s response would be the strongest of all countries, making Pico Far East vulnerable

I increased the cash position to almost 20%. And I was willing to increase it even further if new evidence came out proving that Omicron led to severe illness.

By 8 December, I had changed my mind. Data from South Africa’s Gauteng province suggested that the now-called Omicron variant would be mild. While the number of new hospital admission had shot up, most of those hospital admissions were incidental. And the total burden on Gauteng’s hospital system proved to be significantly less than that experienced under the prior Delta wave.

By early December, market sentiment had turned bearish. A spike in VIX to levels above 30 together with bearish positioning suggested significant caution among investors.

There might be cross-immunity from Omicron to other SARS-CoV-2 variants. If such cross-immunity exists, then Omicron is probably a blessing in disguise. The world will become infected within the span of a few months and then have significant immunity to future variants of SARS-CoV-2.

The big wild card is how governments will respond. In theory, zero-tolerance governments such as China’s and possibly Singapore’s could impose even stricter measures to stop the spread of Omicron. Given what we know about Omicron’s transmissibility, fighting it will be futile. But zero-tolerance governments will try.

In my view, emerging markets such as India and Indonesia will reach herd immunity significantly faster than China. And that’s fundamentally bullish for companies in such emerging markets.

For these reasons, I took up the exposure to almost 95% on 8 December. I added to my positions in the following stocks:

- CNOOC. Futures prices continue to be strong, and CNOOC trades at incredibly low multiples. Its A-share IPO could act as a catalyst.

- Jardine C&C. Astra’s numbers have been strong, and while I know that current tax breaks will soon end, I also believe that Omicron will spread across Indonesia faster than elsewhere.

- Ultrajaya. Fundamentals look fairly bright with positive guidance and recent solid results. I felt that the downside protection was relatively strong.

- Ichigo Hotel REIT. The share price had dropped significantly, with a likely improvement in fundamentals as Omicron will lead to faster herd immunity.

- Kyushu Railway. Same story here: faster herd immunity is fundamentally bullish, longer-term.

- BAT Malaysia. The new budget released by the Malaysian government is largely positive for the tobacco industry with no excise tax hikes and improved vaping regulation.

Here is the portfolio as it looks like on 17 December 2021. The portfolio's performance is -1.5% since its inception a bit over two months ago — a disappointing result, to be honest. The cash balance now stands at 5.5%.