Interview: Tian Yang

CIO at Variant Perception

Disclaimer: Asian Century Stocks uses information sources believed to be reliable, but their accuracy cannot be guaranteed. The information contained in this publication is not intended to constitute individual investment advice and is not designed to meet your personal financial situation. The opinions expressed in such publications are those of the publisher and are subject to change without notice. You are advised to discuss your investment options with your financial advisers. Consult your financial adviser to understand whether any investment is suitable for your specific needs. I may, from time to time, have positions in the securities covered in the articles on this website. This is not a recommendation to buy or sell stocks.

1. Hi Tian! Thanks for doing this interview. Can you tell us a bit about yourself and how you ended up at Variant Perception?

I started my career as an equity derivatives trader at Bank of America Merrill Lynch after studying economics at Cambridge. I joined Variant Perception in 2014. Even before I joined the firm, I had read Jonathan Tepper’s books and I was keen to work with and learn from him.

After Jonathan started his own hedge fund in 2020, I transitioned into a leadership role at Variant Perception, with a focus on combining fundamental analysis with advanced quantitative modelling. Today, we offer a macro-quant research service and recently launched our first investment product, the VPX US Equity ETF.

2. What does your research tell you about the top-down macro conditions right now? And on that note, where do you see credit growth and liquidity potentially improving?

Our macro work relies heavily on our adaptive leading indicators, where we model out the growth, inflation, policy and liquidity outlook over the next 6-12 months. We then abstract down all of this complexity into an overall macro risk regime. We have been in a “risk on” regime since the summer of 2025 and still remain in that regime today.

At the margin, we are seeing some deterioration across growth, inflation and policy components, but I would describe the shift as the removal of previous tailwinds, not yet big headwinds. Given the inflationary impulse from the Iran war, we are seeing a pretty synchronized hawkish shift in global monetary policy pricing. These headwinds will build as the year goes on.

3. Can you talk about the broad macro picture for China? What does the government want to achieve, and what does that imply for exchange rates and asset prices?

The global investing landscape will continue to be dominated by the primacy of sovereignty, on which we wrote a big thematic report last year. The short version is that we live in a G2 US-China world and sovereignty and security of food, energy, supply chain etc is now the primary driver of policymaking.

As a result, expect governments to prioritize these aspects over traditional economic growth previously centred on the consumer. This does not mean that there won’t be a reactive stimulus to buffer the economy during big downturns, but it means that investors need to ask if their portfolio holdings directly support national security and sovereignty.

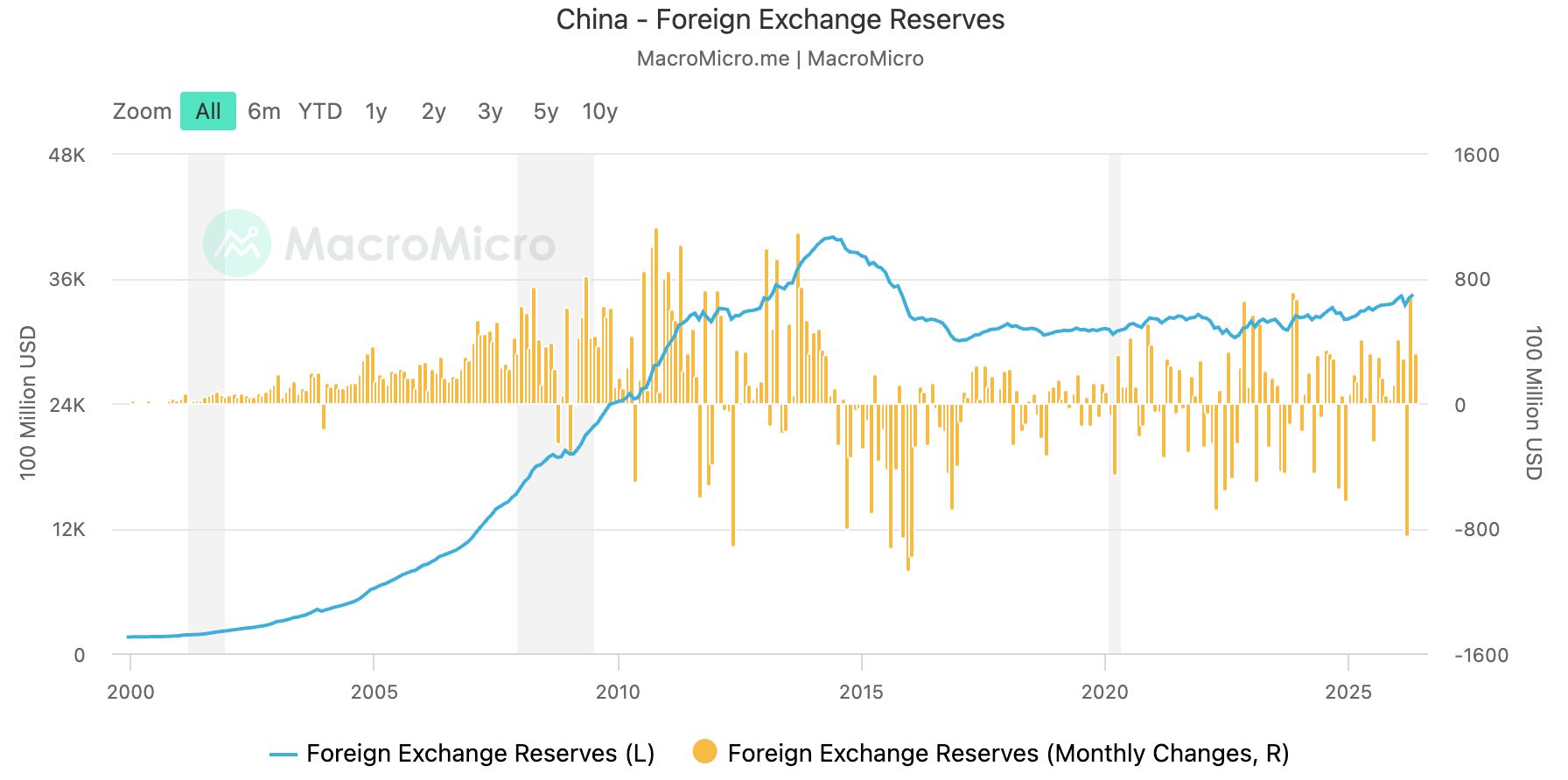

The Chinese economy remains in a “new normal”, where the household/consumer are no longer the priority, with resources and capital diverted towards geopolitically important industries linked to critical resources, technology and manufacturing. FX is tricky. The most clear trend is that China’s need to diversify away from USD reserves will continue to weigh on the USD and create a bid for hard assets such as gold.

4. What’s your take on the US interest rate cycle, and what would a weaker US Dollar mean for Asian asset prices overall, and in specific countries?

The markets are pricing in hikes across most major economies fearing a 2022 repeat. However back in 2022, interest rates were only just coming off the zero bound and there was still a lot of Covid-stimulus working its way through. Today, the starting level of real yields is much higher and the Fed is NOT obviously behind the curve. So the odds of a 2022 repeat crashing bonds and equities is low right now. I think interest rates markets are pretty fairly priced at the moment.

The US dollar is probably going to be stuck for a while, caught between the structurally bearish outlook of countries diversifying away from USD reserves, and the cyclically bullish terms of trade shock due to the Iran energy shock.

In terms of the impact on Asia, you need to differentiate between which countries are exposed to the terms of trade shock and which countries will benefit. Not only do you have the Iran-linked energy shock, but you also basically have a semi supply chain shock too. So if your country needs to import energy and import chips or semi equipment, then your currency is much more vulnerable.

5. What’s your view on the Japanese Yen? It seems incredibly cheap on a real effective exchange rate basis. How do you expect interest rate differentials to develop, and what does that mean for the exchange rate? What do you think about the Japan carry trade narrative?

Japan’s problem is that its impossible trinity problem has not been resolved leaving a weaker JPY as the natural adjustment mechanism. This has been the case for a number of years and up until the end of 2025, this was the primary reason we were consistently skeptical of the bullish arguments for a strong JPY.

However this year, things seem to be changing. Prime Minister Takaichi is firmly committed to her expansionary fiscal agenda and they are allowing long-end yields to rise. Yet, at the same time, the BoJ is still not willing to normalize policy rates at the speed the market demands, but the MoF is still happy to burn reserves intervening in the FX markets again.

This shows that we are near breaking point and Japan will be forced to make a choice. My guess is there is a non-negligible chance of a US-Japan Plaza Accord style FX intervention to strengthen the JPY. US Treasury Secretary Bessent has visited Japan multiple times and a weaker USD is also in the Trump administration’s interest. My bias is to now be long JPY.

6. You expressed optimism about Indonesian equities recently. What’s your thinking there?

I think this is more one for the Asian bottom-up specialists such as yourself who can find the babies thrown out with the bathwater. The crisis of confidence among investors in Indonesia is reaching a crescendo and the MSCI review of Indonesia’s EM status could mark the final capitulation. Yet leading indicators are still holding up for Indonesia and there are high quality non-bank non-commodity stocks in Indonesia trading at very reasonable valuations.

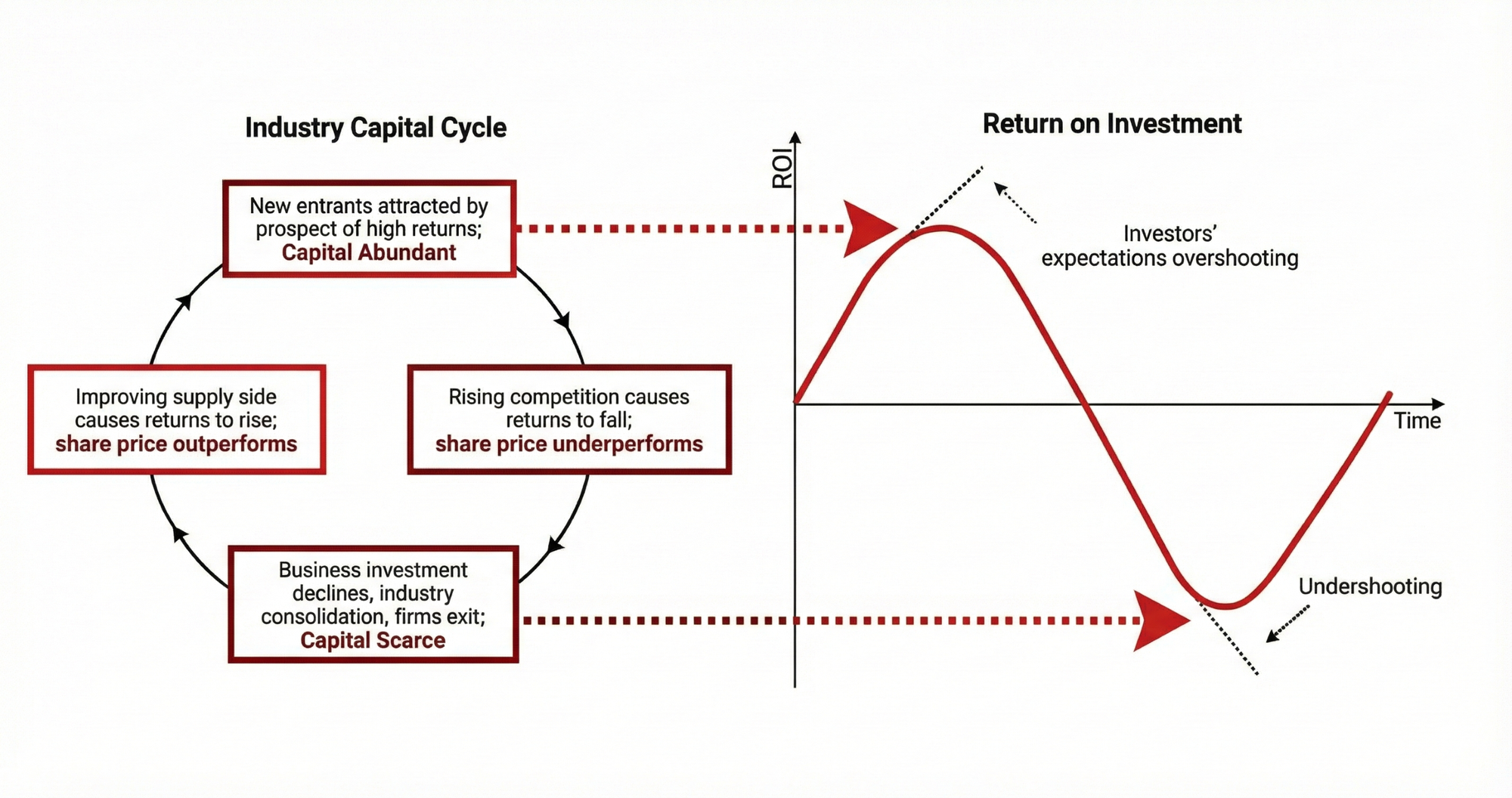

7. I know you’ve done a lot of work on capital cycles. What’s the theory behind that work? How do you actually spot where industries are in their capital cycles, and which industries are currently turning upwards?

We were inspired by Marathon Asset Management's capital cycle framework. The basic idea is very intuitive, too much capital flowing into a particular industry creates too much competition, reducing future profits and vice versa. We have quantified the capital cycle across global industries.

We track net investment (capex, R&D spend net of D&A) across industries and the marginal operational ROIC generated above WACC for that investment. Which then allows us to compare across industries.

The best times to invest are when net investment has been low, yet ROIC is inflecting higher and vice versa. How you define your industries and profit pools matter. On our models semiconductors remain capital scarce, but software and communication services have poor capital cycle scores. Alongside semis, energy and financials are also capital scarce, so we like a barbell of semi secular growth alongside the more traditional cyclical value from energy and financials.

In terms of how we turn the capital cycle into an equity portfolio, we actually use it alongside quality and crowding when we are coming up with our fair value estimates. Nobody knows how long the current semi bottlenecks and secular demand shift can carry on for, but the pace at which Anthropic’s revenue is surging is a reminder of the unique nature of AI and the speed at which Jevon’s paradox is having an impact vs any traditional commodity cycle. Our mindset is much more to observe marginal changes in our models across all these factors and react accordingly rather than make deterministic predictions on how things will look.

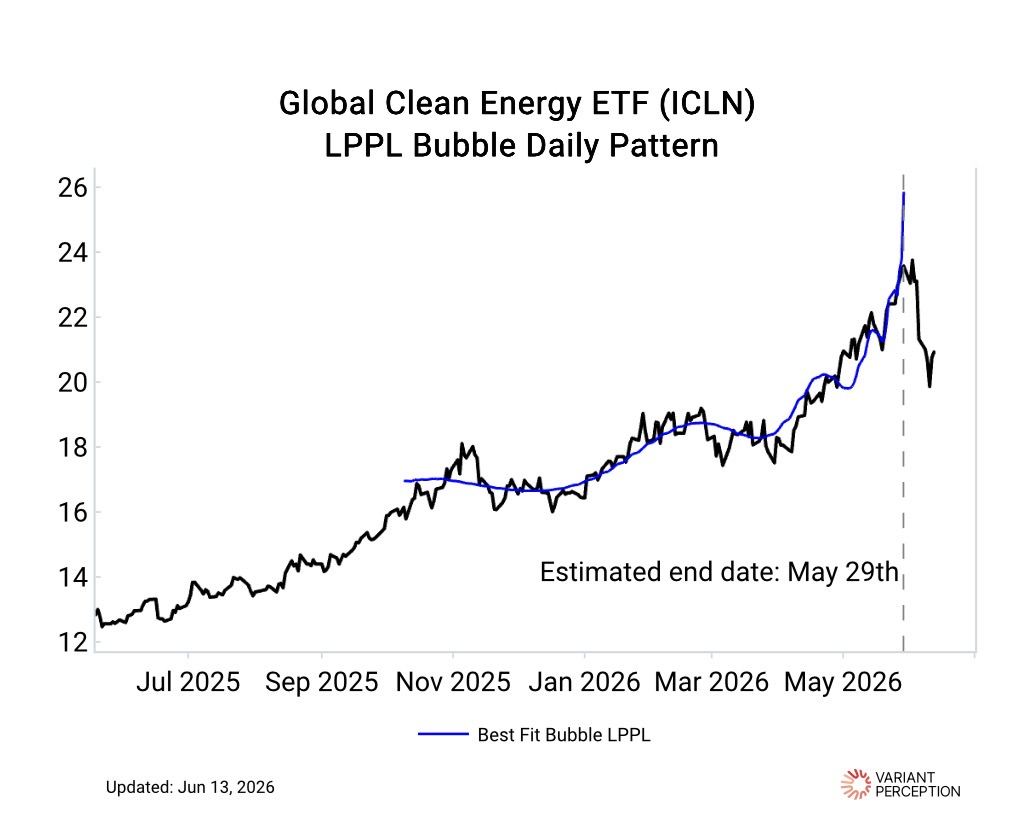

8. You’ve mentioned Didier Sornette’s Log-Periodic Power Law (LPPL) model in your research. Could you explain what the model does, and why it can be helpful for investors? Any asset classes that are exhibiting late-stage bubble behavior right now?

The LPPL model is a very good way to model stop-loss behavior, when a stop-loss sell order drives down the price and triggers 3 more stop-loss sell orders which crash the price further and sets off 9 more stop-loss sell orders.

It is not enough just to observe a parabola in the price, you also want to see the wave pattern within the parabola speed up, which reflects this dynamic of accelerating stop loss behavior. I.e. during the sell-off you observe each dead-cat bounce being weaker and lasting for a shorter period of time before the next sell-off.

We use this model to help with tactical timing and to flag when these cascading sells or buys are exhausting. For example at the end of March we saw a cluster of LPPL crash exhaustions (i.e. buy signals) across tech and growth names.

Today, we are seeing a cluster of LPPL crash exhaustions across China tech, suggesting we have already seen a disorderly stop-out there and that this is a good time for contrarian investors to step in or at least sharpen pencils.

9. Thanks for doing this, Tian! Where can people go to learn more about you, your writing and Variant Perception?

www.variantperception.com or @VrntPerception on X.