Update: Saramin (143240 KS)

South Korea's leading HR-tech company

Disclaimer: Asian Century Stocks uses information sources believed to be reliable, but their accuracy cannot be guaranteed. The information contained in this publication is not intended to constitute individual investment advice and is not designed to meet your personal financial situation. The opinions expressed in such publications are those of the publisher and are subject to change without notice. You are advised to discuss your investment options with your financial advisers, including whether any investment suits your specific needs. From time to time, I may have positions in the securities covered in the articles on this website. Full disclosure: I do not hold a position in Saramin at the time of publishing this article. To reiterate, this post and the below presentation are for informational and educational purposes only – not a recommendation to buy or sell shares.

South Korean online recruitment platform Saramin is highly unusual. It operates in an oligopoly together with private equity-owned JobKorea. It has high margins and a high return on capital.

Despite all this, Saramin trades at a discount to its net cash position. This will be the subject of today's post.

1. Quick recap

I wrote about South Korean HR-tech company Saramin (사람인, formerly known as "SaraminHR") back in 2023:

The background is this:

- Saramin runs the largest online job board in Korea, with 2.5 million monthly active users. Users upload their resumes to the database, and employers use the search engine or matching algorithms to find potential hires. Its business model is very similar to Japan's Recruit or Australia's Seek.

- On the saramin.co.kr website, you can search for jobs via profession, region, through personality-based AI matching, etc. You can also find graduate events and intakes. You can also find company reviews, anonymous salary information and a community where you can ask career-related questions.

- The revenue comes from employers who place ads on the platform. To get your job posting higher up in the search results, employers need to pay. Prices range from KRW 182,000 (US$120) to KRW 6 million (US$3,900) depending on the visibility tier. Meanwhile, basic postings are free. The average active employer has paid a little over US$1,000 per year, lower than in many other developed markets.

- In addition to the job board, Saramin also runs a headhunting arm that helps companies and government agencies find employees. As well as a staffing agency that's closer to a company like Manpower. But these segments have not been particularly profitable. Almost 100% of Saramin's operating profit has come from the online job board.

- Within South Korea, Saramin has had a roughly 25% market share. Its domestic peer JobKorea had similar user numbers and engagement rates. Network effects would normally dictate a winner-takes-all market. But I pictured the two companies coexisting. Saramin had carved out a niche for itself through a focus on small-and medium-sized enterprises, and that consumer mindshare has proven difficult to beat.

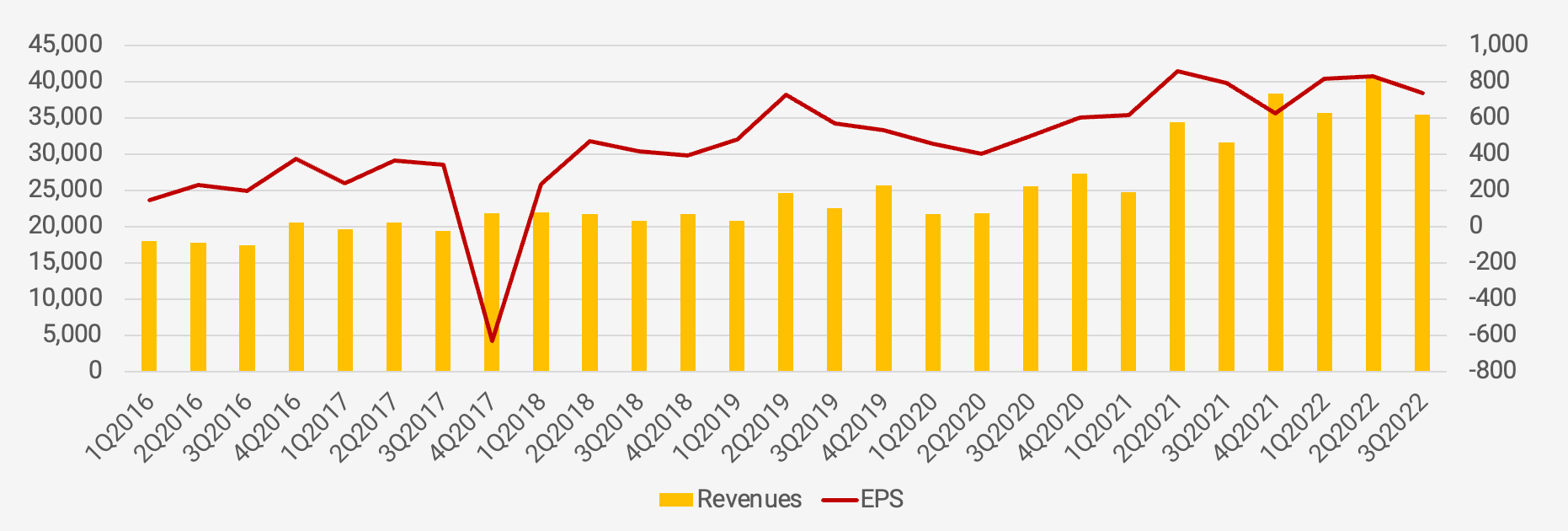

- An online job board can be incredibly profitable. Back in 2022, Saramin had an operating profit of 30%, which I pictured was thanks to its network effects, the scale of its company review database and the scale of its R&D.

- The trailing 5-year top-line compound annual growth rate was +12%, and EPS growth was +25%. I expected growth to slow down, but the historical numbers were high:

- Outside the country, Saramin owns a 70% stake in the Vietnamese recruitment portal TopDev, one of the leading job portals in that country. And since 2021, it has also held a stake in Remember, a newer app sometimes referred to as the LinkedIn of South Korea.

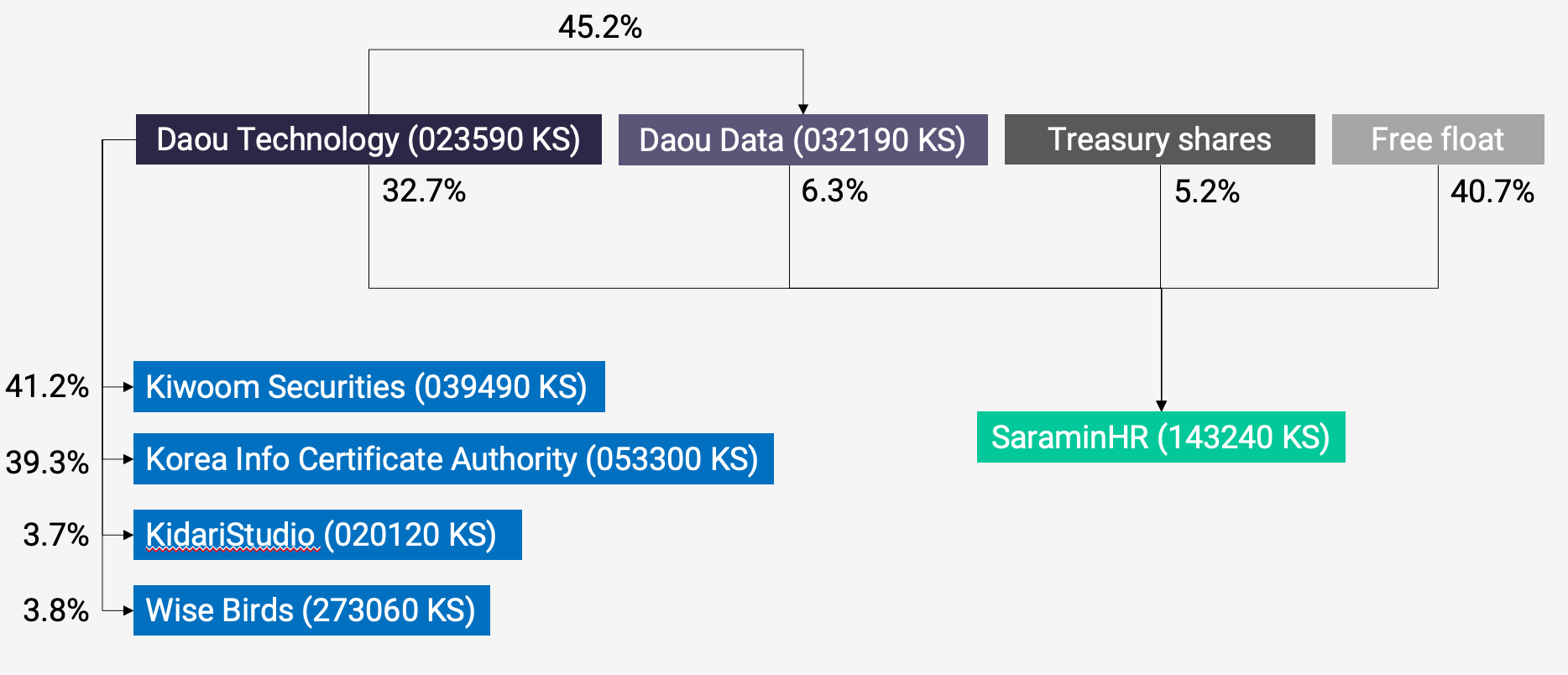

- Saramin is a part of the broader Korean technology group Daou Technology, which also owns Kiwoom Securities. The Kim family controlled Saramin through a pyramid structure, enabling them to maintain absolute control despite historically holding only 1.5% economic interest.

- Saramin's then-CEO Lee Jeong-geun had come from Korea Credit rating, then NICE Dun & Bradstreet and finally NICE Credit Rating. He was seen as a safe pair of hands.

- There were early signs that the industry backdrop had weakened, however. The number of job openings had turned lower. Revenue growth had also deteriorated along with a weaker Korean economy. The demand for consumer electronics was hurt during the COVID-19 recovery, and I couldn't see any light at the end of the tunnel.

- The stock, however, traded at a low multiple of around 8x forward P/E. And I noted that the company had instituted its first share buyback since 2015, suggesting a focus on capital returns.

- A key risk was that South Korea's job market would continue to deteriorate. Some investors worried about competition from the newly listed Wanted Labs. There had also been claims that Saramin had copied job postings from JobKorea back in the mid-2010s, but I could not find any evidence either way.

But ultimately, Saramin was a cyclical story. I believe that the economy would eventually turn, though the timing was certainly hard to judge. And indeed, the recovery took longer than I had expected.

2. A recovery in Korea's job market

First, let me just say that there are clear headwinds in the Korean economy. The demographics are poor, with a total fertility rate of just 0.7. Interest rates have been elevated since 2022, causing households to deleverage and consumers to pull back.

However, after four years, the job market is finally recovering. This chart from East Asia Econ shows that the labor market started to become tighter from early 2026 onwards: