Hi! Welcome to a subscriber-only edition of Asian Century Stocks – a newsletter about Asian value stocks. For a complete list of all previous posts, check out the Table of Contents.

Disclaimer: This article constitutes the author’s personal views and is for entertainment and educational purposes only. It is not to be construed as financial advice in any shape or form. Please do your own research and seek your own advice from a qualified financial advisor. From time to time, the author holds positions in the stocks mentioned below consistent with the views and opinions expressed in this article. This is a disclosure, not a recommendation to buy or sell stocks.

Market commentary

I feel like a kid in a candy store. Stock prices came down significantly in March due to the US and Israel attacks on the Iranian government.

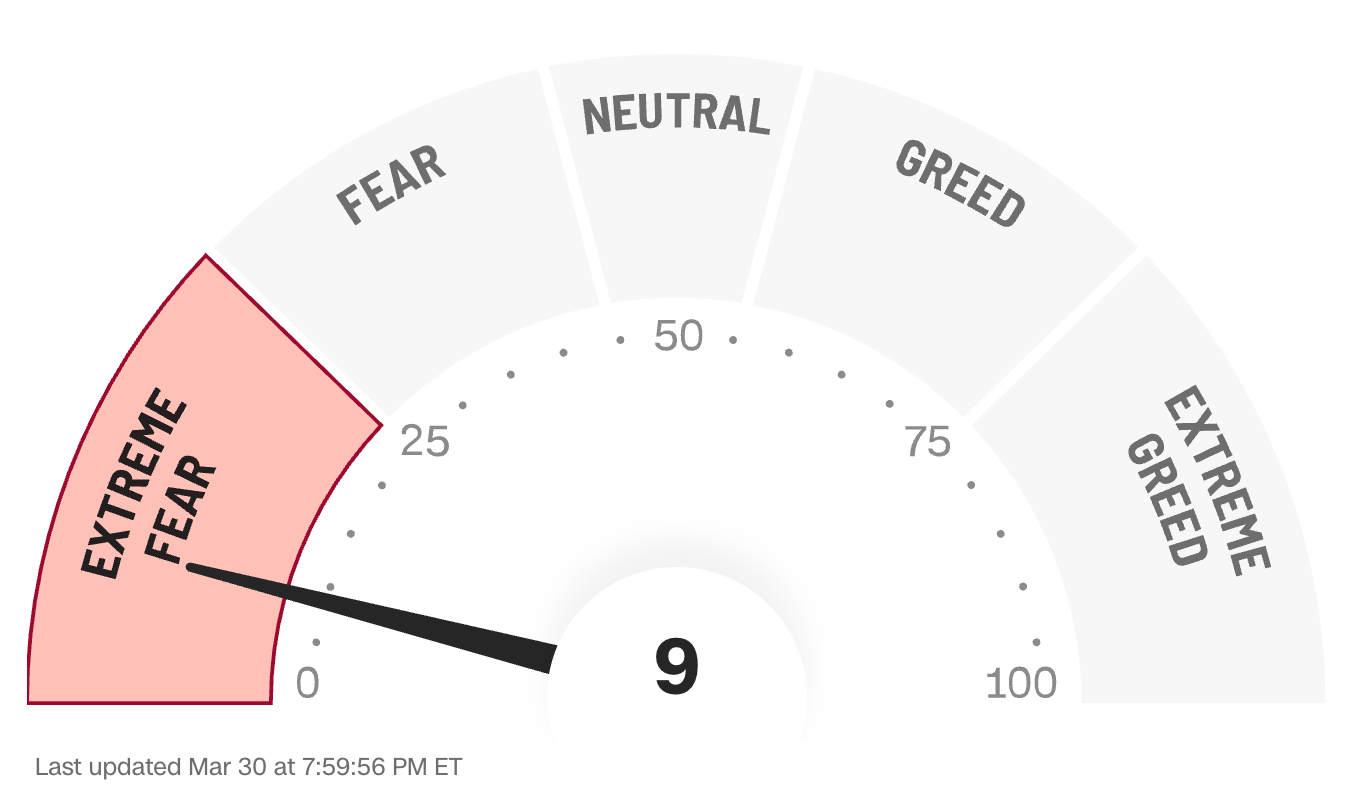

I'm not an expert on the conflict. But what I do know is that most of my holdings have zero exposure to the Middle East, or even to oil prices. And sentiment is now extremely weak, judging from the CNN Greed & Fear Index, which just reached 9/100:

Low reading tend to correlate with bottoms in the stock market, according to research from Sentimentrader.

The MSCI Asia Ex-Japan ETF is now down about 13% from the peak:

Several smart investors, such as Bill Ackman, seem to believe that it's now a decent time to enter. It does feel like a non-consensus call.

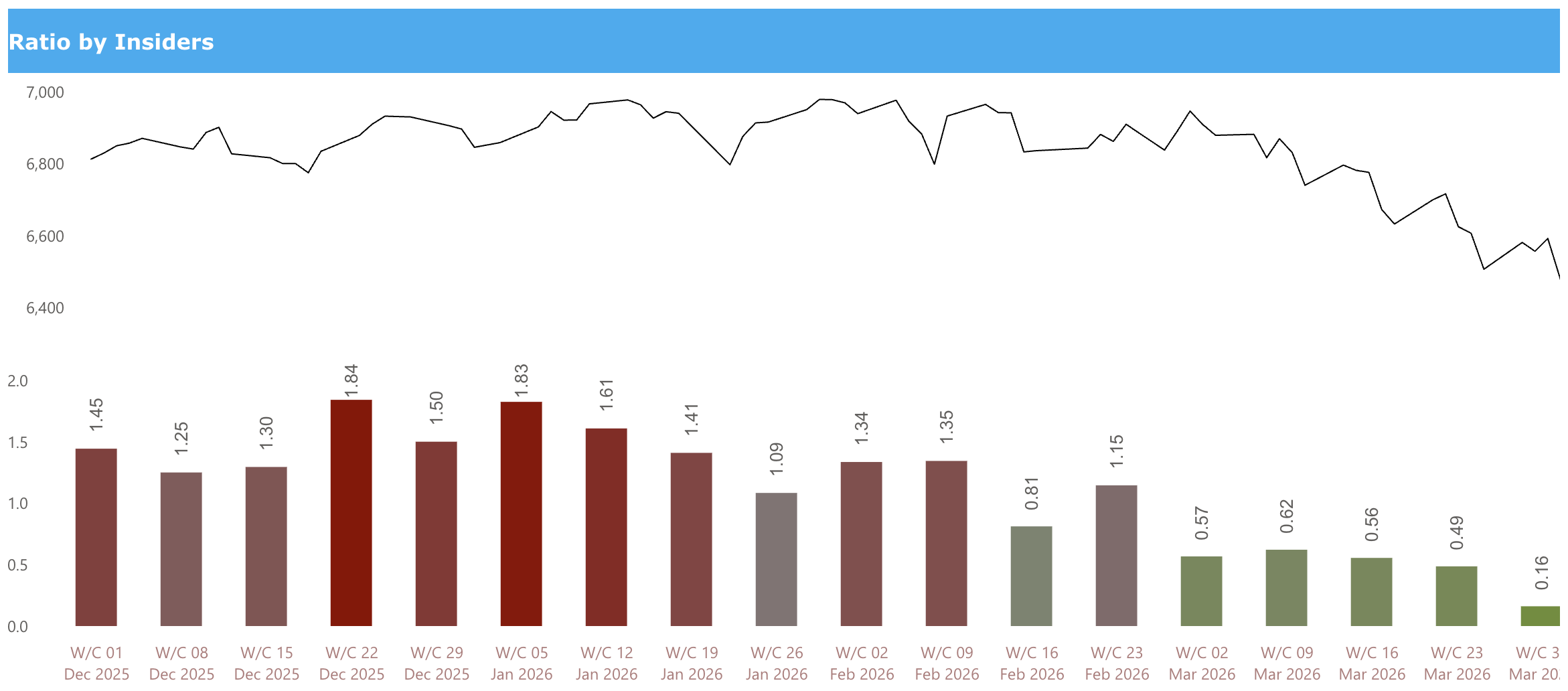

Also, check out the Asia insider selling/buying ratio, courtesy of Smart Insider. It measures the number of insiders selling vs buying. A low ratio means that buyers outnumber sellers.

Today, the ratio has come down to an almost unprecedented level of 0.16x:

In other words, buyers outnumber sellers by a factor of six. Are they seeing something we don't?

In terms of sectors, one interesting trend is that Asian DRAM spot prices have begun to decline. DRAM spot prices tend to be coincident indicators for memory chip makers like Micron and SK Hynix.

Robeco argued that Korean memory chip export volumes dropped from October to February due to retooling of fabs for high bandwidth memory chips, causing a squeeze in the market for memory chips. But supply is now coming back to the market. SK Hynix's new M15X fab will primarily make high-bandwidth memory, but not entirely. So the commodity DRAM market will benefit as well. And it won't take much to correct the ludicrously overpriced commodity DRAM market.

This has implications not just for memory chip makers and the KOSPI, but also consumer electronics companies – the buyers of DRAM and NAND chips. I'm therefore becoming interested in companies such as Micro-Star International, Logitech (which just initiated a new share buyback), Lenovo, Sony, and Nintendo.

I'm also noting that through this market carnage, Japanese SaaS companies have held up very well. Poper, for example, rose +6% this morning on no news. Who's buying and why?

So given this backdrop, I'm keen to be fully invested. I see plenty of opportunities across Thailand, the Philippines, consumer electronics companies, Japanese software developers, and sellers of wristwatches, among others. I see no reason to stay cautious.

Portfolio update

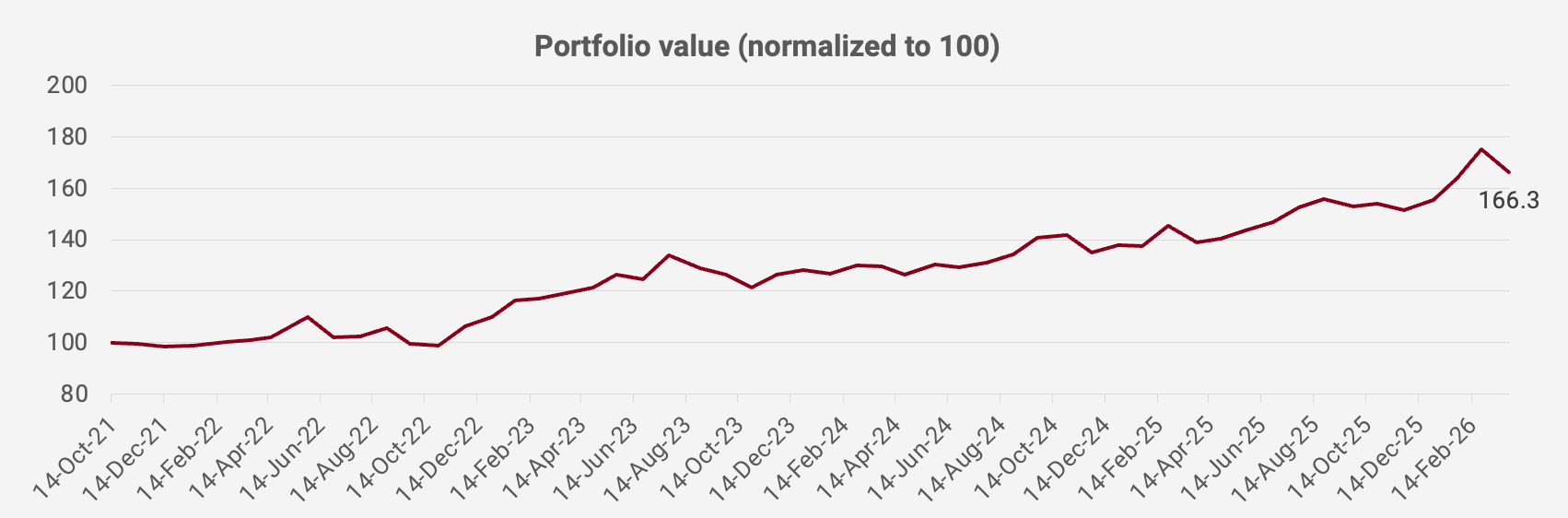

My portfolio declined by -5.1% month-on-month in US Dollar terms in March 2026. Since the portfolio's inception in October 2021, the portfolio's value has increased by +66.3%, equivalent to an +11.6% compound annual growth rate:

Part of the decline was currency-related, with the US Dollar Index (DXY) rising by +2.8%, indicating that the US Dollar appreciated against other currencies. But we also saw broad-based declines in e.g. Thai stocks in late February and early March, hitting Major Cineplex and Carabao. Fairfax India also declined as India is exposed to higher oil importers.

Here's what my Asia-focused portfolio looked like as of 30 March 2026:

{kind=link}