Hi! Welcome to a subscriber-only edition of Asian Century Stocks – a newsletter about Asian value stocks. For a complete list of all previous posts, check out the Table of Contents.

Disclaimer: This article constitutes the author’s personal views and is for entertainment and educational purposes only. It is not to be construed as financial advice in any shape or form. Please do your own research and seek your own advice from a qualified financial advisor. From time to time, the author holds positions in the stocks mentioned below consistent with the views and opinions expressed in this article. This is a disclosure, not a recommendation to buy or sell stocks.

Summary

- The portfolio rose by +6.8% in February 2026, driven by a massive rally in the Korean index provider FnGuide.

- The Asia-Pacific has become a two-tier market, with East Asian tech-heavy names riding the AI capex cycle and Southeast Asian old-economy markets left in the dust. However, the Thai market has surprised positively, and I'm seeing greater interest in Asia from international investors.

- Several new buys. They're either at low valuation multiples or trading at fair value, with positive momentum in their fundamentals.

- Looking forward, I'm excited about the decline in the share prices of SaaS companies like Freee. The impact of generative AI tools is hard to gauge, but Freee should certainly be more protected than the typical point-solution software providers. They seem to be skating to where the puck is going. The store count growth in Best Mart 360 excites me as well, especially as the company is set to report full-year earnings in late March 2026.

Market commentary

East Asian markets have been on fire. KOSPI is up by almost half in just two months. While that performance is mostly due to the memory chip bull market, index provider FnGuide has also been swept up in the mania as Korean retail investors are clamoring for thematic ETFs.

The Asia-Pacific has now become a two-way market: with tech-heavy markets like South Korea and Taiwan on the one hand, and sleepy Southeast Asian old-economy markets on the other.

I prefer to stay away from industries that I do not understand. But I cannot help notice the scale of the capex taking place. In January 2026, TSMC reported +37% year-on-year sales growth, and it's now upping its capex from US$41 billion to US$52-56 billion. I see smart people are betting on Japanese AI capex beneficiaries. Others, like Stan Druckenmiller, are out of the AI capex trade altogether.

My only exposure is in Japan's SaaS industry, where I own the mini-enterprise resource planning system Freee. I spent some time thinking about the disruption from generative AI tools. The value of existing software must have decreased, given ongoing improvements in coding. In the words of newsletter company Ghost's founder, John O'Nolan:

"I don't imagine it will be long before any sufficiently successful proprietary product with a public-facing interface can be reverse-engineered and rebuilt by a motivated competitor with access to frontier models"

Scary words. So if I invest in software, I need to err on the side of caution. In other words, stick to companies with strong economic moats with management teams that are skating towards where the puck is going. It does feel like Freee is a sticky platform. I'm personally more concerned about outsourcing companies like Infosys and Tata Consultancy Services, as generative AI tools could well reduce their billable hours, at least in the longer term.

Another bombed-out sector is alcohol. I personally own Ginebra San Miguel and Multi Bintang. There seems to be a post-COVID inventory problem that's about to be resolved. Alcohol seems more hated than tobacco at this point, so I lean towards the former. But I'm still not excited, given the signs that Gen Z are becoming less health-conscious and less willing to drink.

A more positive trend is the rise in watch collecting. And I've now taken three positions in companies benefiting from it. I noted in a weekly update that there's an ongoing turnaround in luxury watch prices. Southeast Asia remains stronger than China/HK, but the turnaround is visible across almost all regions. The Swiss watch export data is constructive, and many of the names are trading at low multiples.

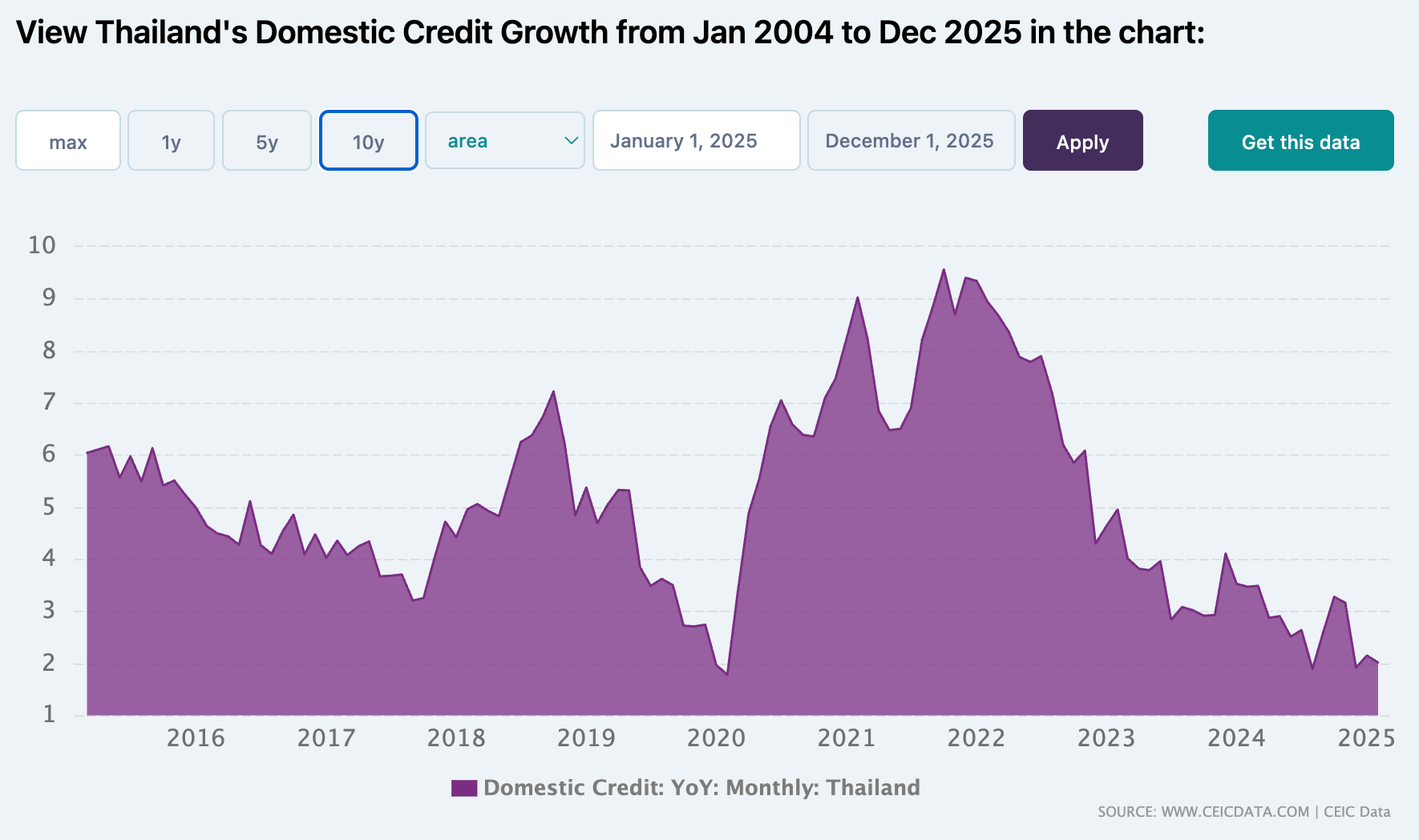

Finally, there's been a quiet turnaround in the Thai stock market:

I haven't seen anybody express optimism about Thai stocks yet, except for Marc Faber late last year. That makes me think the rally has legs. The latest rally took off after the general election on 8 February 2026, which gave the Bhumjaithai Party coalition a supermajority. The outcome reduced the risk that incumbent monopolies would be broken up by the reformist People's Party (the successor to Move Forward). The Bank of Thailand also reduced its policy rate to 1.0%, increasing the likelihood that Thai credit growth has finally bottomed out:

Overall, I see the greatest value in Southeast Asian equities. But I'm also excited about South Korea, where the reform momentum is gathering pace, and many higher-quality stocks still trade at single-digit P/E multiples.

Portfolio update

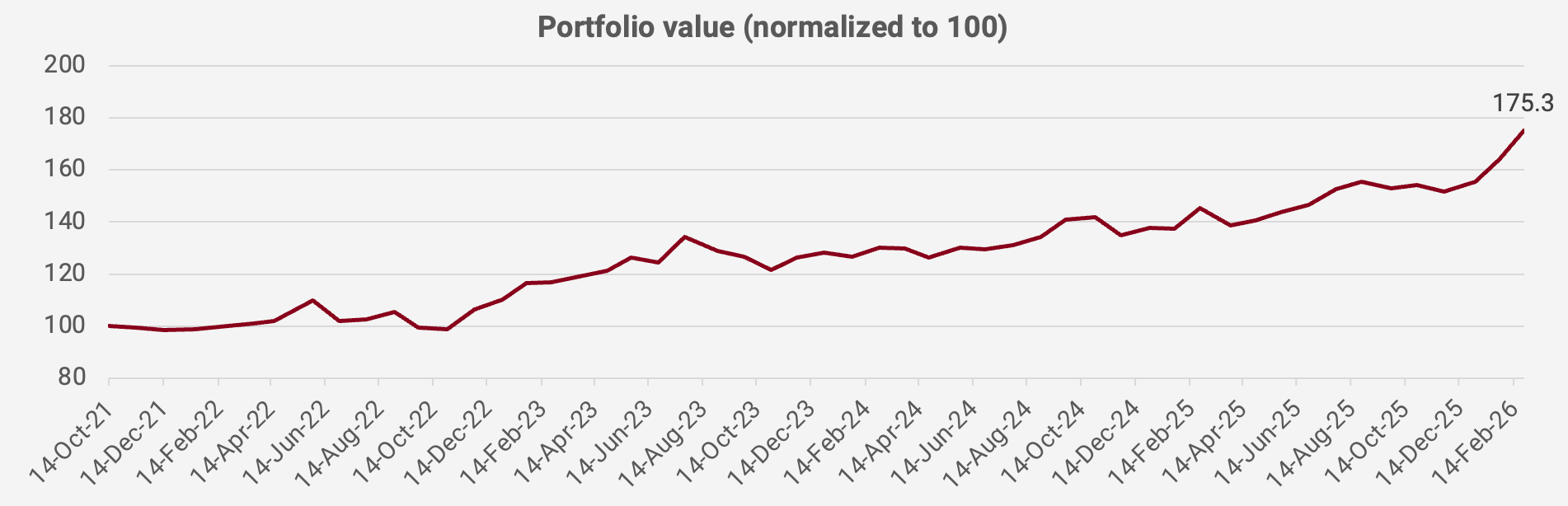

My portfolio rose by +6.8% month-on-month in US Dollar terms in February 2026. Since the portfolio's inception in October 2021, the portfolio's value has increased by +75.3%, equivalent to a +13.7% compound annual growth rate:

The largest contributor by far was FnGuide, which reported that the AUM of ETFs following its indices rose from KRW 14 trillion in early 2025 to KRW 50 trillion today. There has been news of a large number of ETFs being launched based on the FnGuide indices. And there's also been a general market boom benefitting FnGuide's core information platforms. The bellwether stock in this bull market is memory chip maker SK Hynix. And from what I can tell, there's no sign of DRAM or HBM prices falling just yet.

Thai cinema operator Major Cineplex has also started rallying, with no news other than a general turnaround in the Thai stock market.

On the negative side, the Japanese SaaS company Freee declined by almost half over the past year. Investors are worried that competition will heat up, now that Claude can replicate code quickly. Freee's founder, Daisuke Sasaki, says that it will be a net beneficiary of generative AI. As a generalist, I can't have much conviction in how the software industry will develop. But at the same time, the market panic is clearly visible. And I question whether the market is properly differentiating between point-solution software and the moatier, B2B software like SAP's.

In any case, here's what the latest portfolio looked like as of 25 February 2026:

{kind=link}