Lithium is moving into oversupply

Demand growth will probably decelerate as subsidies are phased out. Supply should eventually react to higher prices. Estimated reading time: 14 minutes

Disclaimer: Asian Century Stocks uses information sources believed to be reliable, but their accuracy cannot be guaranteed. The information contained in this publication is not intended to constitute individual investment advice and is not designed to meet your personal financial situation. The opinions expressed in such publications are those of the publisher and are subject to change without notice. You are advised to discuss your investment options with your financial advisers. Consult your financial adviser to understand whether any investment is suitable for your specific needs. I may, from time to time, have positions in the securities covered in the articles on this website. This is not a recommendation to buy or sell stocks.

Summary

Lithium is used for a number of applications, including glass, ceramics, pharmaceuticals and even atomic bombs.

Since the invention of the lithium-ion battery in the 1990s, the primary use case of lithium has become batteries. And especially EV batteries, which are now the main driver of demand.

EV demand has been boosted by subsidies and license plate regulations in China and Europe. But the financial subsidies are slowly being phased out, particularly in China. So it would be unwise to extrapolate the past few years of record growth.

This massive growth in EV demand caused lithium prices to go to US$80,000/kilotonne compared to just US$10,000 a few years ago. Producers are now making returns on equity of about 60%, with incredible IRRs on new projects. This should, in theory, incentivise new production. And since lithium is plentiful with a reserve life of >250 years, I can’t see lithium remaining scarce. Any supply response will cause spot prices - and eventually, contract prices - to correct.

There’s a significant amount of froth among several listed lithium producers, including the Australian small and mid-caps, but also America’s Albemarle and Chile’s SQM. Some of these stocks have gone up 10x as higher lithium prices have worked their way into sell-side estimates. The companies’ earnings would suffer if a supply response ever materialises.

Lithium is used for batteries

Lithium is a base element with the atomic number 3. It’s essentially a silvery-white metal that’s highly reactive. Therefore, it never occurs freely in nature, always bound to something else.

Another key property of lithium is its high energy density per unit of weight, making it particularly suitable for battery applications.

But in the early days, batteries weren’t even on the radar for lithium. It was used for ceramic and glass production. The use of lithium back then helped reduce the melting point of glass and helped glass producers as on energy costs. Lithium was also used to produce high-strength glass for televisions, for example, from the 1950s onwards. And as raw material for the construction of atomic bombs as well as a pharmaceutical to treat depression.

The demand for lithium didn’t take off until Sony invented lithium-ion batteries in the 1990s. Compared to lead-acid- and nickel-cadmium batteries, lithium-ion batteries are rechargeable, more environmentally friendly and with higher energy density. It’s now used as a raw material in the batteries used for laptops, power tools, smartphones and, more recently, electric vehicles (EVs).

In fact, looking forward, almost all growth in demand for lithium is expected to come from EVs. Both because EV sales volumes are on the increase, but also because a typical EV uses 30-60kg of lithium compared to just around 5g for a smartphone.

These lithium-ion batteries work by transferring lithium ions between two electrodes:

From an anode, typically made of graphite or possibly silicon;

To a cathode made of nickel, cobalt, manganese, etc

Ions are atoms that have extra or fewer electrons. The transfer of these lithium ions from the anode to the cathode creates a flow of electrons - electricity - that can then be used to power a device such as an EV.

To recharge the battery, plug in a power source to move the lithium ions from the cathode back to the anode.

Today, the cathode, the anode and the electrolyte tend to be in cylindrical shapes, similar to typical household batteries. In electric vehicles, thousands of such cylindrical batteries are stacked together in cells, forming larger battery packs.

Two technologies compete in the EV battery market, differing in the types of materials they use for the cathode:

Nickel-manganese-cobalt (NMC): NMCs offer better energy density and therefore longer driving range per kg of weight. Longer life span.

Lithium-ferro phosphate (LFP): Less combustible and therefore safer. Don’t require cobalt, which is expensive and subject to volatility in price.

Many believed that NMC batteries would take over, but even Tesla continues to use LFP batteries thanks to recent technological improvements and relative affordability.

In any case, whatever technology is used, lithium is present in all of them. So if EVs become the de facto standard for passenger vehicle transport, lithium will be needed in greater and greater quantities over time.

The lithium triangle, Australia and China

The supply of lithium comes from either:

Lithium brines (=salty water) in salt lakes such as Chile’s Salar de Atacama or in China’s Qinghai or Tibet. Lithium from salt brines is concentrated through solar evaporation in ponds and refined further.

Hard rock deposits include spodumene ores and clays such as Australia’s Greenbushes, Mt Marion or Pilgangoora and China’s Jiangxi, Sichuan or Xinjiang.

Such lithium resources can be found across three main geographies globally:

The so-called lithium triangle is where Chile, Argentina and Bolivia meet in the southwestern part of South America. The lithium triangle is the home of roughly 70% of the world’s lithium resources. An incredibly dry climate caused lakes to dry up, with lithium from volcanic rocks ending up in high concentrations. Chile is currently the largest producer of lithium from salt lakes but the largest resources are found in Bolivia. Argentina’s production has also remained surprisingly weak, due to infrastructure bottlenecks and macroeconomic uncertainty.

Volcanic rocks or clay deposits in Western Australia. These lithium deposits are typically found in a mineral called spodumene. Crushing and milling the ore with acid leaching is then used to concentrate the lithium.

China’s Xinjiang, Sichuan and Jiangxi provinces with a mix of hard rock deposits and salt brines. These are higher-cost resources.

Brine deposits have lower operating costs and quicker timeline to initial production. While the initial capex for hard rock deposits is higher, they tend to lead to a more reliable and consistent product. Almost like a typical manufacturing operation.

Since only a fraction of the brine contains lithium, it doesn’t make sense to transport lithium brine or spodumene ore over large distances. Instead, solar evaporation increases the concentration of lithium, causing it to become lithium chloride. Soda ash is then added to create lithium carbonate, which can be used for ceramics or glass. Sometimes, batteries require lithium hydroxide, which can be achieved by adding lime.

The final step of the production process is removing impurities. 90% of such final processing takes place in China. Typical battery-grade lithium has a purity level of 99.5%. But that’s not enough. It’s also a question of what materials are in the remaining 0.5%. Calcium, iron or sulphate are unwanted materials that will affect the performance of a battery.

The final battery, cathode and anode production typically takes place in close proximity to key auto manufacturing centres in China, Europe, the United States, etc.

Demand is likely to decelerate

So, EV markets have been on a tear since 2020. China’s EV sales have increased exponentially. But the European EV market has also been strong since the pandemic. I believe that subsidies and license plate regulation have been the primary drivers of this growth. It doesn’t hurt that automakers have released a larger number of EVs available for sale.

In 2020, roughly 11 million electric vehicles were sold. Most of those electric vehicles were sold in China - the largest market, by far.

As I argued in this previous post, the major driver of the Chinese EV market has been stricter license plate regulations since 2019. Consumers have been able to secure license plates by purchasing EVs, even though they’re less convenient.

These license plate advantages remain in place in most cities. But China’s EV market is slowing due to the expiry of financial subsidies at the end of 2022. And by the end of this year, the 10% purchase tax exemption for EVs will also lapse, making it more expensive to buy an EV in China.

Many of the EVs sold in the past year have also been purchased knowing that subsidies will eventually lapse:

“A lot of EV demand has been brought forward, so I think the first half of 2023 will not look good" - Source from a China-based lithium converter, early 2023

Europe - the second-biggest EV market - is barely growing in terms of sales volumes. Subsidies and VAT exemptions are now being reduced across Germany, France and Norway. These subsidies have, in many cases, been in place since 2020, when Europe’s EV market really took off.

Other markets, such as the United States, have not been meaningful so far in overall EV volumes. The Inflation Reduction Act, which will become effective later this year, will spur EV sales growth for GM and Tesla as well as for commercial vehicles, since they now enjoy tax breaks as well.

But overall, I absolutely do not agree with the view that EVs are about to exhibit an S-curve effect in demand. What’s needed for such an S-curve to take shape is for EV prices to drop below those of ICEs even before subsidies. Beyond the psychological effect of a higher car price, gasoline savings from EVs are easily counteracted by fast battery depreciation and range anxiety, in my view.

For example, a Volkswagen Golf ICE vehicle today costs around US$31,000, whereas a Volkswagen ID4 EV costs about US$40,000. But almost no OEM globally makes money producing EVs - the profit margins remain extremely low. At normal profit margins, EVs would probably be more expensive. Even dealerships suffer from low margins selling EVs.

So we’re witnessing governments worldwide trying to affect consumer behaviour through heavy-handed methods. It’s not impossible that ICEs will become outlawed at some point, like in the EU after 2035. But I do not think it will be a smooth process. Consumer demand has traditionally been the driver of technological revolutions - not government mandates.

In the very short term, EV sales will probably decelerate, given reduced subsidies across both China and Europe, the two most important EV markets. Now that lithium prices are high, the cost of producing an EV has also risen commensurately. Many sell-side reports assume a 30% growth in EV sales per year for 2023. That number seems way too high to me. I’d rather pencil in a number closer to 10-20%.

A supply response should emerge

Here’s a lithium cost curve from S&P Global back in mid-2022:

As you can tell, the all-in-sustaining cost of lithium for a current global demand level of 600 kilotonnes or so is about US$11,000/kilotonne. Australia and Argentina are low-cost producers. Chile’s Salar de Atacama enjoys high lithium concentration per unit of weight, which in theory, should improve its cost competitiveness. But government taxes are high at up to 40%. Meanwhile, China remains at the top of the cost curve.

Compare this US$11,000/kilotonne cost estimate with China's onshore lithium carbonate prices of roughly US$90,000. Lithium miners make windfall profits, at least if you exclude transport costs.

Will there be a supply response? Absolutely. Lithium is one of the most common commodities in the world, with a global reserve life exceeding 250 years, compared to 30-60 years for nickel, copper and iron ore.

IRRs on new greenfield projects should be gigantic at this point. Some of the IRRs that I’ve been able to identify from Atlantic Lithium, Sigma Lithium, and Manna Lithium are in the triple-digit range.

You can also observe the windfall profits in lithium miners’ return on equity for their trailing twelve-month earnings. Returns on equity are now about 60% vs about 14% historically. So it looks like the major lithium producers are over-earning at this point.

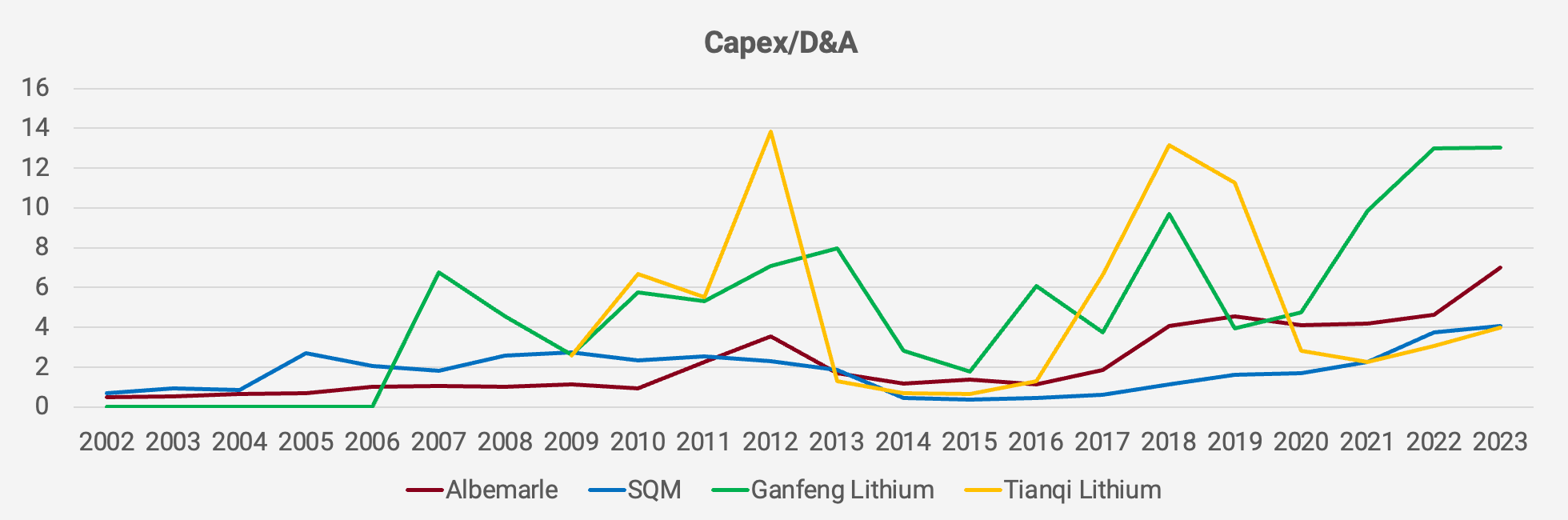

So far, I’m not seeing any elevated levels of capex among the major lithium producers.

Here are a few estimates of supply growth from third-party analysts:

Bloomberg Intelligence expects a 2023 increase in the supply of 190 kilotonnes of lithium carbonate equivalent (LCE) or roughly +34%

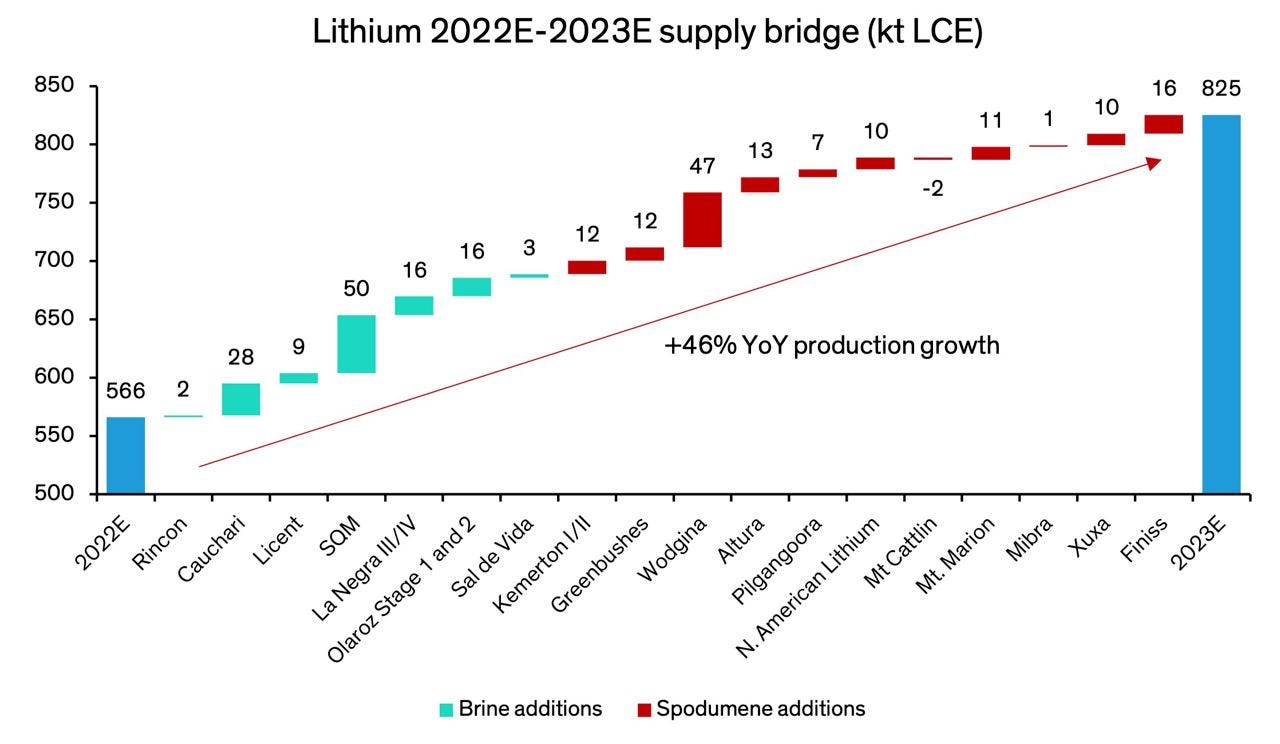

Bernstein expects a 2023 increase in the supply of 259 kilotonnes LCE, +46%. You can see the reasoning behind this estimate through the following chart:

Let’s review the major components of Bernstein’s supply bridge:

SQM’s Salar de Atacama: In late 2022, a local regulator allowed SQM to reach 270 kilotonnes capacity in the Salar de Atacama, from roughly 210 kilotonnes currently. But this capacity will probably occur across two years, making me think a 35 kilotonnes increase per year is more realistic.

Cauchari: Lithium America’s Cauchari-Olaroz project in Argentina is likely to start production at the end of 1Q2023 with full production of about 20 kilotonnes/year. Bernstein’s estimate seems a bit high, yet again.

Wodgina III: Train three has already been commissioned and will go into operation in 2023, though the planned lithium hydroxide plant with a 50 kilotonnes capacity has not yet been built.

These are just a few of the assumptions in Bernstein’s model. It does seem aggressive. I’d rather go with Bloomberg Intelligence’s estimate of +190 kilotonnes.

But we could also see further supply response developing throughout the year. I’m seeing such commentary across the industry:

“An approaching supply glut of both batteries and the raw metal input this year.” - Liu Jincheng, Eve Energy in November 2022

“The EV market has got a bit overheated the last two years, certainly since COVID. Of course, China is the hotbed of that, the top end price in lithium, if you like, is a perfect example of that, moving to $80,000 a ton last year from a time 3, 4 years ago when we were used to $10,000 a ton… We're coming maybe to the end of this overheated market that's going to be a bit of reality that sets in this year.” - Simon Moores, Benchmark Minerals, 13 January 2023

“All the car companies can actually get sufficient supply of the batteries. For us, regarding the lithium resources, we have seen some lithium resource enter the market in the past year.” - Li Bin, NIO 3Q2022 earnings call

Lithium prices remain lofty

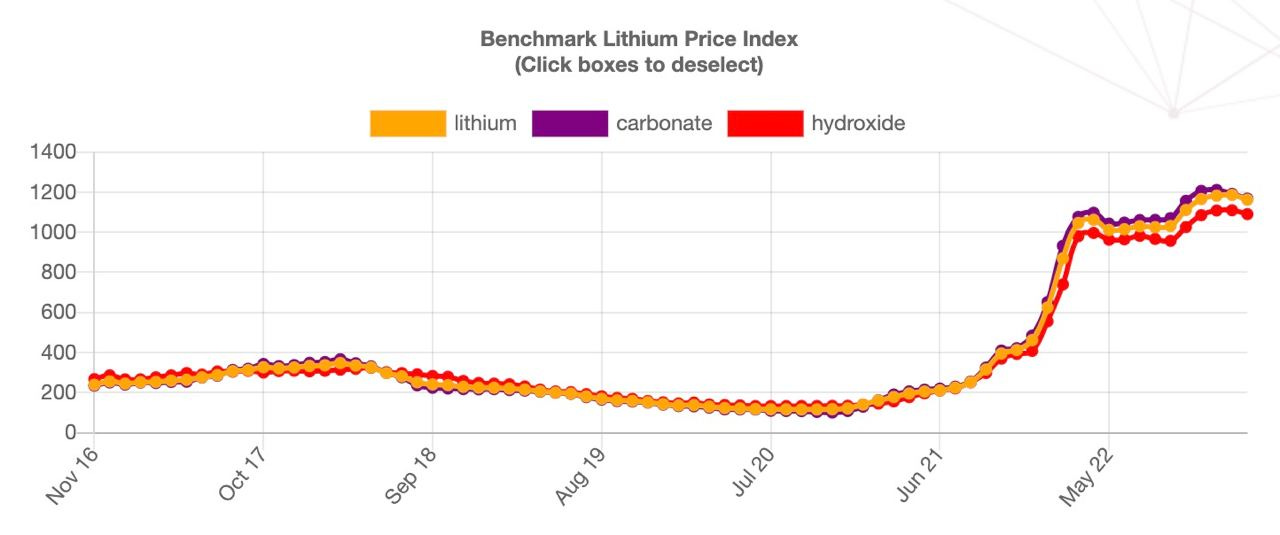

Pricing in the lithium sector is not transparent. 80% of the market sits in longer-term contracts that are continuously negotiated. According to industry analytics firm Benchmark Minerals, these negotiated lithium prices remain high:

The spot market that exists in China is significantly more volatile, with a downtrend that’s started to occur since the fourth quarter of 2022 due to ballooning domestic supply of lithium carbonate. And there’s also been a weakness in China’s EV market after the financial subsidies lapsed at the end of 2022. China is the most important market for lithium, so one should take this recent weakness seriously.

The investable universe of stocks

The lithium market is dominated by four major companies: Albemarle, SQM, Ganfeng Lithium and Tianqi Lithium.

Albemarle (ALB US - US$32 billion) is a North Carolina-based speciality chemicals producer with large exposure to lithium, including assets in Chile’s Salar de Atacama and a brine resource in Nevada, United States. It also owns a stake in spodumene miner Talison Lithium in Australia.

Sociedad Química y Minera de Chile or SQM (SQM US - US$24 billion) is a Chile-based lithium producer that’s developing the Salar de Atacama brine resource. It’s owned by Augusto Pinochet’s former son-in-law and has a difficult relationship with government body Corfo. It also doesn’t own its resources but rather leases it from the government, with a lease renewal due in 2030.

Ganfang Lithium (1772 HK - US$22 billion) from Jiangxi Province in China started out as a lithium metal smelter, but thanks to state support, it’s been able to use state bank funding to acquire lithium resources across the world, including Australia’s Mt Marion spodumene resource and several projects in Argentina.

Sichuan-based Tianqi Lithium (9696 HK - US$21 billion) owns a majority share in Australia’s high-grade Greenbushes resource and also a 24% stake in SQM.

Looking at their valuation multiples, neither Ganfeng nor Tianqi Lithium look particularly expensive. The real froth is in the smaller Australian lithium miners such as Pilbara, IGO, Mineral Resources and Allkem, in my personal view. Among the larger producers, Albemarle and SQM also trade at lofty levels.

Fellow Substack author Jonah Lupton recently pushed the case for Albemarle, stating that its multiples are attractive given its growth profile. However, gross profit margins of 45% are unlikely to be sustainable, so expect volatility in EPS on the downside.

A company that would benefit from lower lithium prices is electric bike manufacturer Niu Technologies, which I did a deep-dive on here:

Conclusion

Today’s lithium market is not unlike that in 2018, when lithium prices reached incredible levels and eventually came down to earth. The catalyst back then was SQM increasing its production after the government body Corfo hiked its quotas.

This time around, it’s unclear exactly where the new supply will come from. But incredible returns on capital and IRRs will almost certainly bring greater supply to the market, causing lithium prices to eventually correct. From what I can tell, supply operates with a 6-18 month lag.

Looking at volume projections, I’m sceptical that EV demand will keep up with the standard industry assumption 30% increase per year. Especially given the ongoing subsidy cuts in China and Europe. Any shortfall in demand or surprise on the supply side would then lead to a lower China onshore spot price for lithium chemicals, followed by lower negotiated prices.

I see the most amount of froth among the Australian producers, but also Albemarle and SQM, which itself has a number of issues which I think aren’t fully appreciated by investors, including its 2030 lease renewal.

If you would like to support me and get 20x high-quality deep-dives per year and other thematic reports like this, try out the Asian Century Stocks subscription service - all for the price of a few weekly cappuccinos.