Table of Contents

Disclaimer: Asian Century Stocks uses information sources believed to be reliable, but their accuracy cannot be guaranteed. The information contained in this publication is not intended to constitute individual investment advice and is not designed to meet your personal financial situation. The opinions expressed in such publications are those of the publisher and are subject to change without notice. You are advised to discuss your investment options with your financial advisers. Consult your financial adviser to understand whether any investment is suitable for your specific needs. I may, from time to time, have positions in the securities covered in the articles on this website. This is disclosure and not a recommendation to buy or sell.

Here’s another edition of my review of the key holdings of Asia-focused funds.

I will release new editions as I find more high-quality funds to track.

Executive summary

- Leading Korean lens manufacturer Sam Yung Trading trades at a P/E multiple of 7x and enjoys high-single digits top-line growth for a product with significant pricing power.

- Several Asian conglomerates trade at significant discounts to NAV, including CK Hutchison, Jardine Cycle & Carriage, COSCO Capital, LG Corp and Samsung C&T.

- US sanctions have hit Chinese SOEs such as CNOOC and China Mobile, and they now trade at single-digit P/E multiples.

- Korean home appliance company Coway enjoys recurring and steadily growing revenues yet trades at P/E 11x - at the lower end of its historical P/E range.

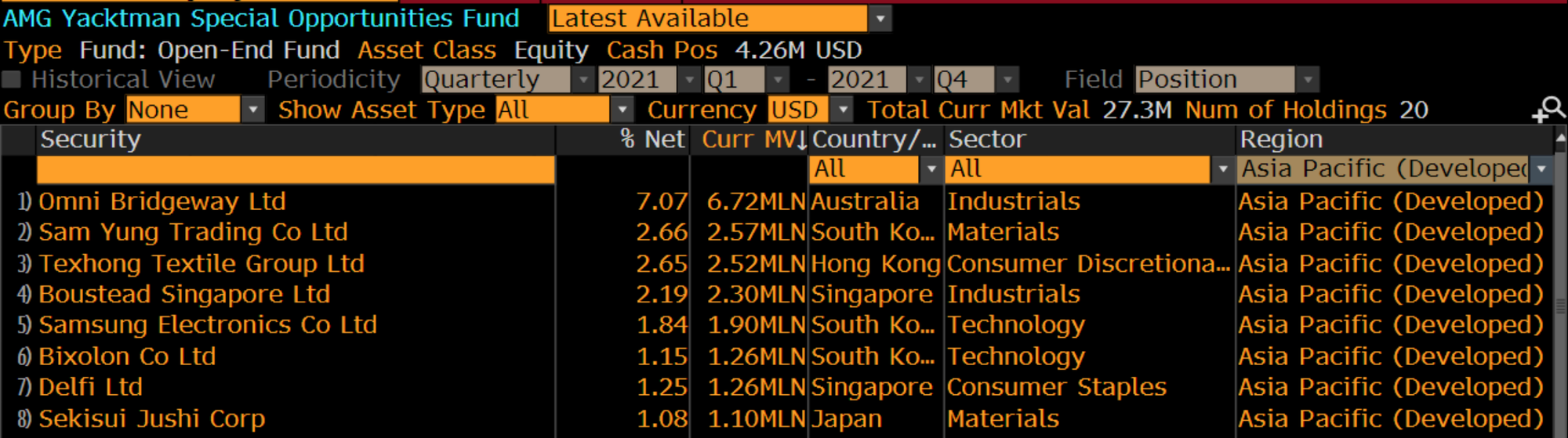

Yacktman Special Opportunities Fund

Yacktman Asset Management is a Texas-based asset management company founded by Donald Yactkman in 1992. The flagship fund AMG Yacktman Fund primarily invests in US companies, but the smaller AMG Yacktman Special Opportunities Fund has more of a global mandate.

The Special Opportunities Fund started just over five years ago and has performed in line with the MSCI ACWI All Cap Index.

Within Asia’s developed markets, the Special Opportunities Fund’s largest positions include the following stocks:

Sam Yung Trading is an eyeglass lens manufacturer in South Korea. It has a 50/50 JV with EssilorLuxottica for the production of eyeglass lenses. The eyeglass lens JV has grown its top-line revenues at a 7% CAGR over the past five years, and the eyeglass lens business seems to be more or less recession-proof. The stock trades at a P/E ratio of 7x.

Chinese yarn manufacturer Texhong is primarily involved in the capital-intensive, upstream part of the textile industry. Texhong was early in its efforts to outsource manufacturing to Vietnam back in the mid-2000s. Thanks to these efforts, the company now sits at the lower end of the cost curve. Texhong’s enterprise value is in line with the average level of the past five years, so the stock is not necessarily trading at a rock-bottom valuation. The near-term P/E is 4x with a dividend yield of 7%.

I covered Indonesian chocolate producer Delfi in this prior write-up. The business was hurt by falling orders from mom & pop shops during the pandemic. The stock trades at P/E 12x on pre-COVID earnings and even lower if you deduct the net cash.

Other stocks in the portfolio such as engineering business Boustead Singapore, Japanese road sign manufacturer Sekisui Jushi, consumer electronics giant Samsung Electronics and Korean receipt printer manufacturer Bixolon trade close to their historical valuation multiples.

The fund’s Asia emerging market holdings include the following three stocks:

CB Industrial is a Malaysian manufacturer of palm oil mill equipment. It also has a small oil palm cultivation business. The fund purchased its shares close to the bottom in 2019. But the stock still trades at just 8x P/E despite a strong balance sheet and rising palm oil prices.

Link Net is the largest broadband provider in Indonesia, with a 25,000km cable network connecting to 1.9 million homes. The long-term growth story is excellent, with Indonesia’s broadband penetration rate remaining at just 8%. While many investors distrust Riady family companies, corporate governance concerns in Link Net may be mitigated by the fact that CVC is a significant shareholder. The stock trades at a P/E ratio of 13x.

COSCO Capital is a holding company for Philippine business magnate Lucio Co. It’s the majority owner of Philippine grocery retailer Puregold. COSCO just spun off liquor distributor business Keepers via a share swap and follow-on offering. In addition to these businesses, COSCO Capital also owns commercial real estate and a speciality retailing business called Office Warehouse. The company claims that its post-spin NAV is about PHP 146 billion, compared to a market cap of PHP 36 billion.

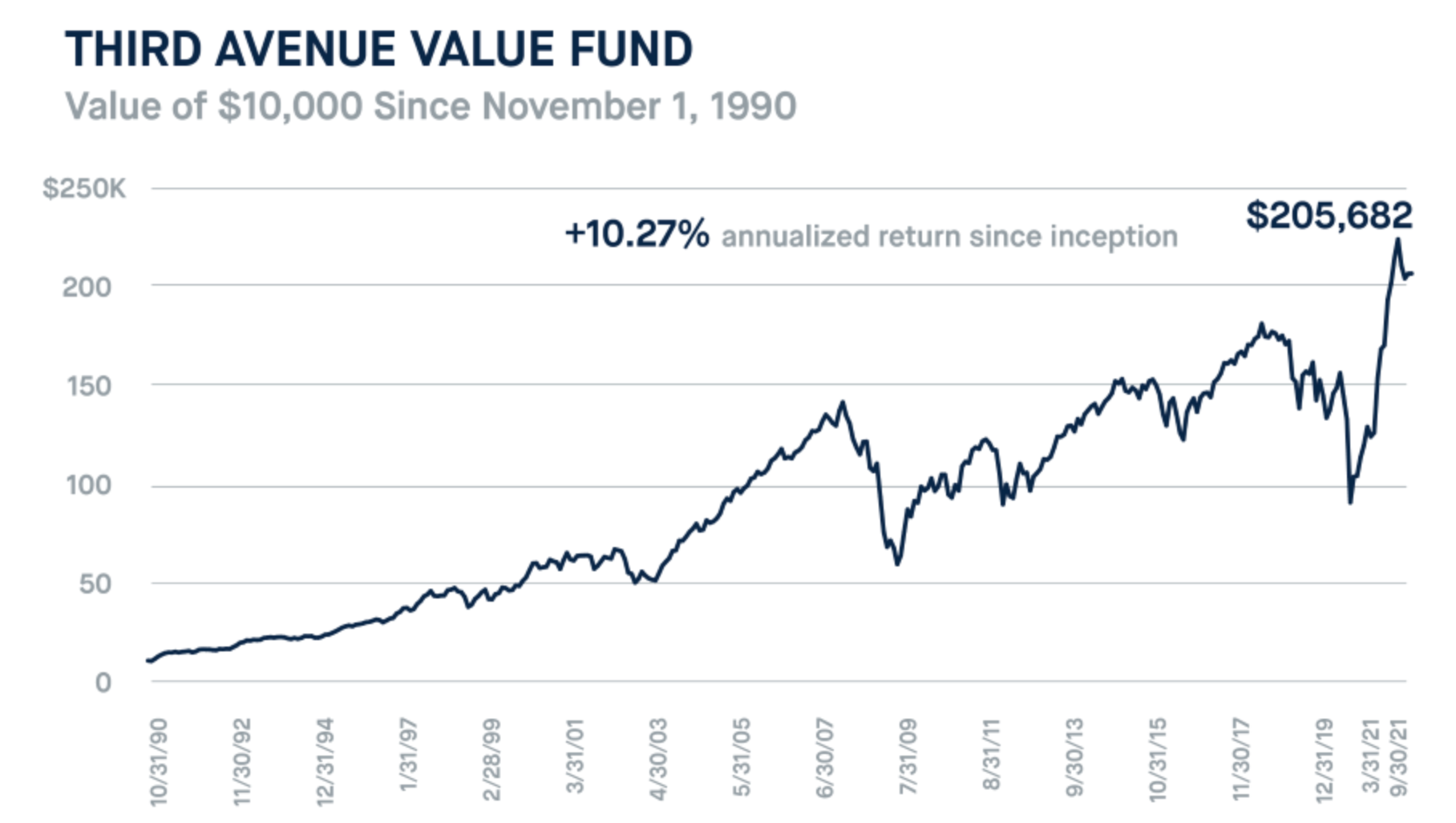

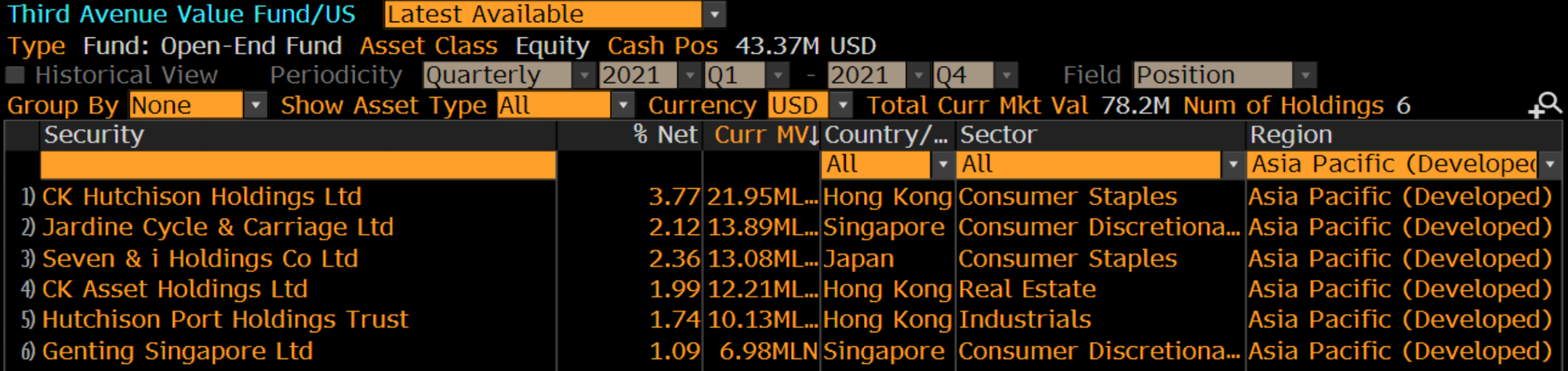

Third Avenue Value Fund

Third Avenue Management was founded by investing legend Marty Whitman, author of The Aggressive Conservative Investor. Whitman was a portfolio manager of the company’s flagship Third Avenue Value Fund for many years. It is a value-focused fund with a global mandate. One of the fund’s recent investor letters can be found here.

Third Avenue’s performance has been decent but not markedly different from that of the MSCI World index.

In the Asia-Pacific region, the fund has invested in the following stocks.

CK Hutchison, CK Asset and Hutchison Port are all Li Ka-Shing owned enterprises. CK Hutchison focuses on retail, transport infrastructure, energy and telecom. The vast majority of earnings come from overseas. Most sell-side firms quote a NAV/share of around HK$100, and the ongoing share buybacks could increase this number further. Investors are concerned about a fall-out between Li Ka-Shing and the top Communist Party leadership in Beijing.

I’ve written about Jardine Cycle & Carriage in this previous deep-dive. The company’s most significant asset is a majority stake in Indonesian auto producer and retailer Astra International. Astra controls 55% of Indonesia’s auto market in JVs with Japan’s Toyota and Honda. While the auto market has suffered during the pandemic, the long-term growth prospects are positive. Most sell-side firms put the net asset value of Jardine C&C at around SG$40/share - significantly above the current share price.

Japan’s Seven & i is the owner of the global convenience chain 7-Eleven. It was previously known as Ito-Yakado but changed its name after its 1991 acquisition of Dallas-based 7-Eleven. The convenience store market is growing strongly across the emerging market universe, taking share from mom & pop stores. The forward 2023e P/E of 14x is lower than the historical level of 20x.

Genting Singapore owns casino operator Resorts World Sentosa. It’s an incredible asset, with a shopping mall development on Sentosa island and only one of two casinos in the city-state. The speed at which the company recovers from COVID-19 will depend on the timing of China’s opening up to the outside world. If Genting Sentosa returns to its pre-COVID profitability, it will trade at P/E 14x and EV/EBIT 8x.

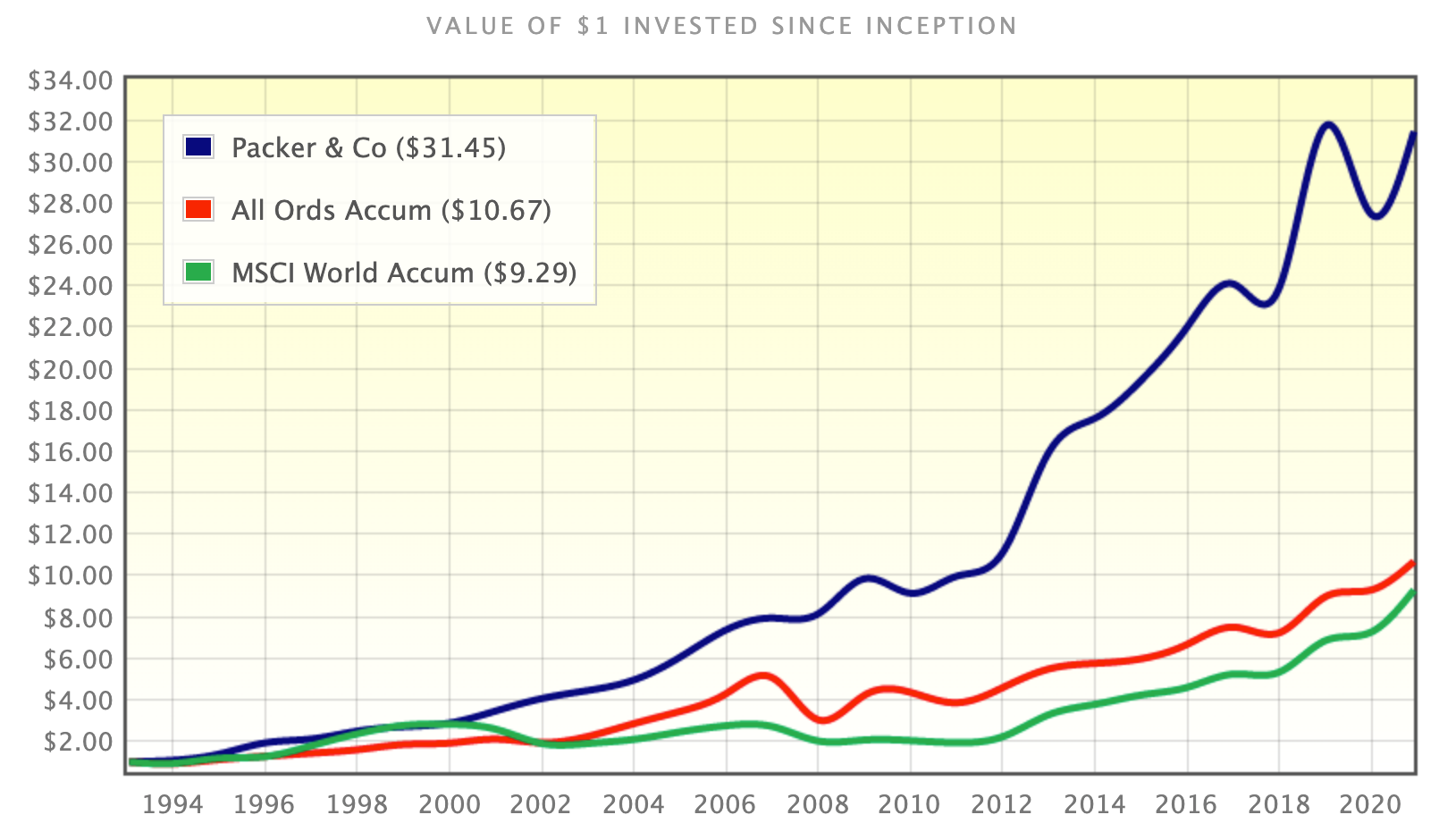

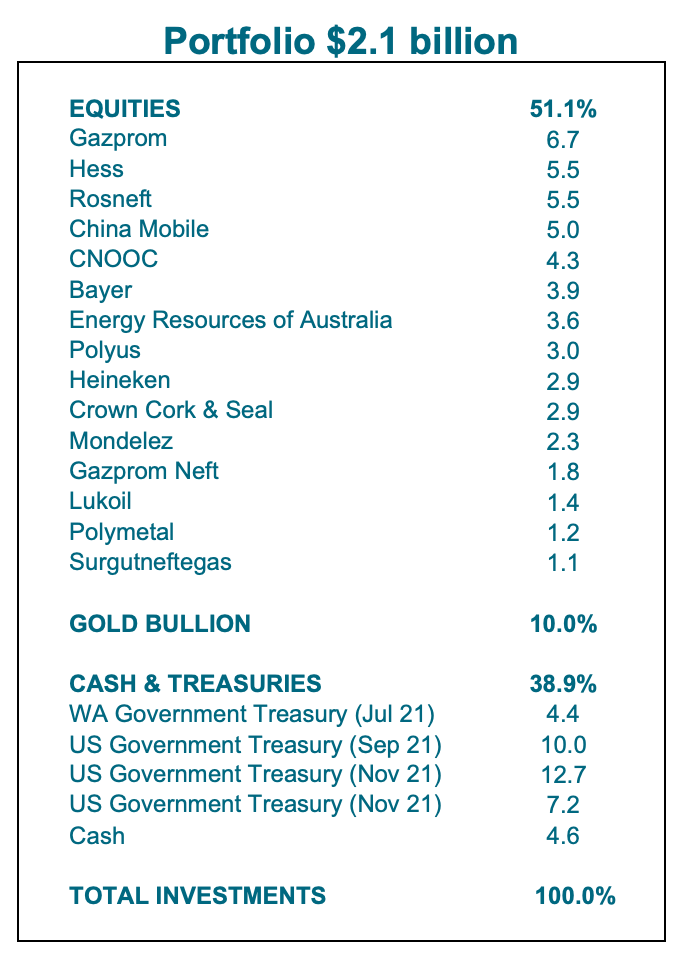

Packer & Co. Investigator Trust

Packer & Co is a Perth, Australia-based fund manager managing a single fund: the Investigator Trust. The fund invests globally in a counter-cyclical fashion. The aim is to buy assets when they are out of favour and sell them when investors become exuberant. The Investigator Trust’s performance has been solid.

The company’s June 2021 letter describes the fund’s current outlook. It believes that we are in a giant stock market bubble with asset prices at ridiculously high valuations. Packer & Co believes that “we have rarely seen a riskier cocktail”.

So as you can probably guess, the fund’s multi-billion dollar portfolio is invested in a conservative fashion. About half of the portfolio is invested in fixed income securities, cash and gold bullion. The other half is invested in low P/E stocks or stable consumer products franchises. The fund seems to have a positive view on oil prices.

Within the Asia-Pacific, Packer & Co has invested in China Mobile. Like the other Chinese telcos, the stock trades at a low multiple of 7x and a dividend yield of 7%. One headwind has been heavy investments into the company’s new 5G network. But it seems that 5g-related capex has started to plateau. Another issue has been Trump’s ban on US investment in Chinese military-linked companies, which has caused forced selling in China Mobile and the other two telcos listed in Hong Kong.

The Investigator Trust has also invested in CNOOC, which I discussed in this prior deep-dive. CNOOC has a near-monopoly in the exploration and production of oil in offshore China. It has grown production and reserves in the single digits while maintaining strong cash flows. The stock trades at a P/E ratio of about 4x.

FPA Crescent

FPA is a Los Angeles-based fund manager investing US$29 billion across several strategies. The company’s high-profile FPA Crescent fund is run by value investor Steve Romick. The fund has matched the performance of the S&P 500 but with much lower drawdowns. It has achieved this by maintaining a significant cash position in the fund and investing that cash counter-cyclically.

FPA Crescent’s developed Asia portfolio includes the following stocks:

The common theme among most of these stocks is that they trade far below the value of their underlying parts. LG Corp, Samsung C&T, SoftBank, Swire Pacific A all trade far below typical sell-side estimates of net asset value per share. But I struggle to see any catalysts for revaluation.

Korean video game producer Nexon focuses on massively multiplayer online games, primarily on PC. Its game franchises include Dungeon Fighter Online and Maple Story. While the company has been slow in the transition to mobile, the company is now catching up. FPA Crescent purchased its shares before 2019 and has been selling into strength. Today, the stock trades at 13x EBITDA.

Japanese medical device company Olympus is a margin expansion bet. San Francisco-based activist investor ValueAct took a stake and reshuffled the board in 2019 in the hope of increasing the operating margin from 10% to over 20%. Since then, the EV/Sales multiple has increased from roughly 2x sales to 4x sales. By now, FPA Crescent has already sold nearly half of its stake.

In emerging Asia, FPA Crescent owns Alibaba and Baidu. Knowing how sell-side typically values these companies, I suspect that FPA is attracted to the large discounts to their sum-of-their-parts valuations. Baidu might conceivably also benefits from the regulatory tear-down of “walled gardens” within China’s Internet universe.

Harding Loevner Emerging Markets Equity

Harding Loevner is an American mutual fund group focusing on global investments. I pay the greatest attention to the company’s Emerging Markets Equity fund, which invests across Latin America, the CIS, Africa and Asia.

The fund's performance in US Dollars has been more or less in line with the index.

Judging from the portfolio composition of the Emerging Markets Equity Fund in their 3Q21 letter, it looks like the fund is hugging the index. The portfolio is conventional, with significant positions in TSMC, Samsung Electronics, Alibaba and Tencent. Those positions have most likely been justified by their large MSCI Emerging Markets Index weights.

What does stand out in the portfolio is South Korean consumer goods company LG Household & Health. What makes LG H&H unique in a Korean context is the company’s shareholder-friendly CEO Suk Cha, whose capital allocation has been excellent. At a P/E ratio of 19x, the stock trades at the lower end of its historical range. LG Household & Health’s preferred shares trade at an even lower multiple.

ASM Pacific has often been seen as the ugly duckling between lithography giant ASML and itself. ASM Pacific focuses on assembly and packaging machines for semiconductors, an industry that has historically been seen as low-margin and commoditised. But perhaps that will change as the front end increasingly struggles to scale geometry and packaging becomes the new frontier in semiconductor development. The stock trades at 15x P/E on normalised margins.

Korean home appliance company Coway also stands out. Coway focuses on water filters, air filters and related appliances. But it’s not a normal home appliance manufacturer - what makes Coway unique is that it is essentially a subscription business. Customers rent the equipment for tens of USD per month and typically replace the equipment after a few years. The business model seems to work as churn remains low at around 1% per month. Coway trades at a forward P/E of 11x despite stable recurring revenues and a historical median P/E of 19x.

Thanks for reading!

If you enjoyed this post, join 202 other intelligent investors as full subscribers of Asian Century Stocks. You will then have immediate access to over 20 deep-dives per year, thematic industry reports and access to to my personal Asia-focused portfolio.

{kind=link}