Borrowing ideas from funds, part 1

Disclaimer: Asian Century Stocks uses information sources believed to be reliable, but their accuracy cannot be guaranteed. The information contained in this publication is not intended to constitute individual investment advice and is not designed to meet your personal financial situation. The opinions expressed in such publications are those of the publisher and are subject to change without notice. You are advised to discuss your investment options with your financial advisers. Consult your financial adviser to understand whether any investment is suitable for your specific needs. I may from time to time have positions in the securities covered in the articles on this website. This is disclosure and not a recommendation to buy or sell.

I recently asked my Twitter followers what funds might be worth tracking here in Asia and received many suggestions.

Since then, I have tried to identify what stocks each of these funds own. While mutual funds disclose their holdings, hedge funds rarely do. Luckily, in Japan and Hong Kong, funds have to disclose any stake that exceeds 5% of shares outstanding. Large hedge funds registered with the US SEC are also required to file 13F filings to disclose key positions such as their Chinese ADRs. Also, note that some data might be outdated.

But here are the fund holdings that I have been able to identify so far:

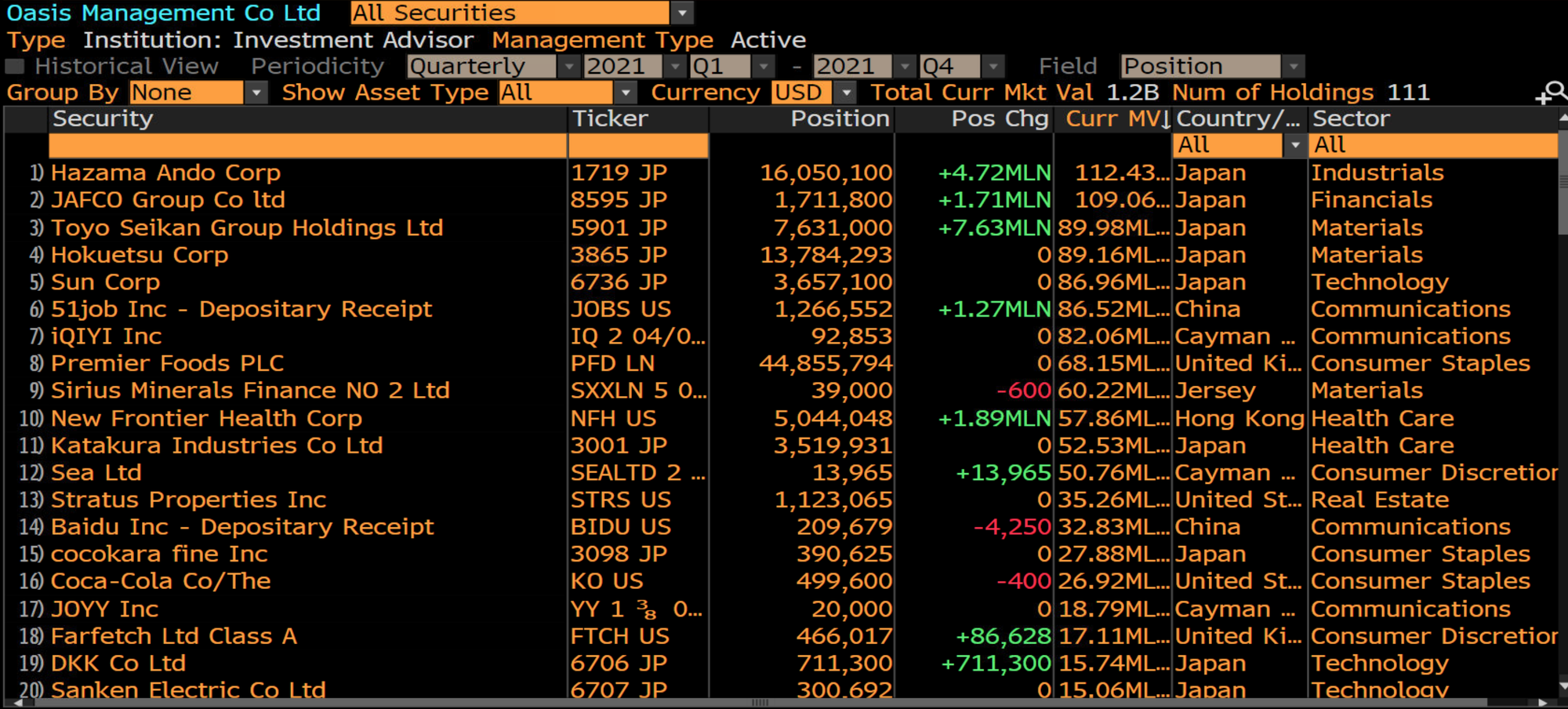

Oasis Management

Oasis Management is a Hong Kong-based hedge fund run by American Seth Fischer since 2002. Before starting Oasis, Fischer ran Asian portfolios for Highbridge Capital Management. The company runs market-neutral multi-strategy funds but has become famous for its Japan activist campaigns.

One of Oasis’s recent campaigns is engineering company Hazama Ando, pitched on Bloomberg here. Fischer mentions a low valuation multiple, company execution issues and Oasis’s recommendation to buy back stock.

I am personally more interested in Sony Corporation, another stock that Seth Fischer has been pushing for several years.

Other stocks in Oasis’s portfolio:

- JAFCO is a venture capital company trading at 1x book.

- Toyo Seikan produces food and beverage packaging products and containers with tiny margins, trading at 10x earnings and 0.4x EV/Sales.

- Hokuetsu manufactures paper products and trades at 7x earnings, though with a certain debt burden.

- SUN Corporation sells pachinko machines, an industry in long-term decline.

- Katakura is a conglomerate spanning auto, clothing, pharma at 9x earnings.

- DKK is an antenna producer trading at close to net cash.

- Baidu is China’s dominating search engine whose underlying earnings are weighed down by its online video subsidiary iQiyi and may benefit from the opening up of Alibaba’s and Tencent’s walled gardens.

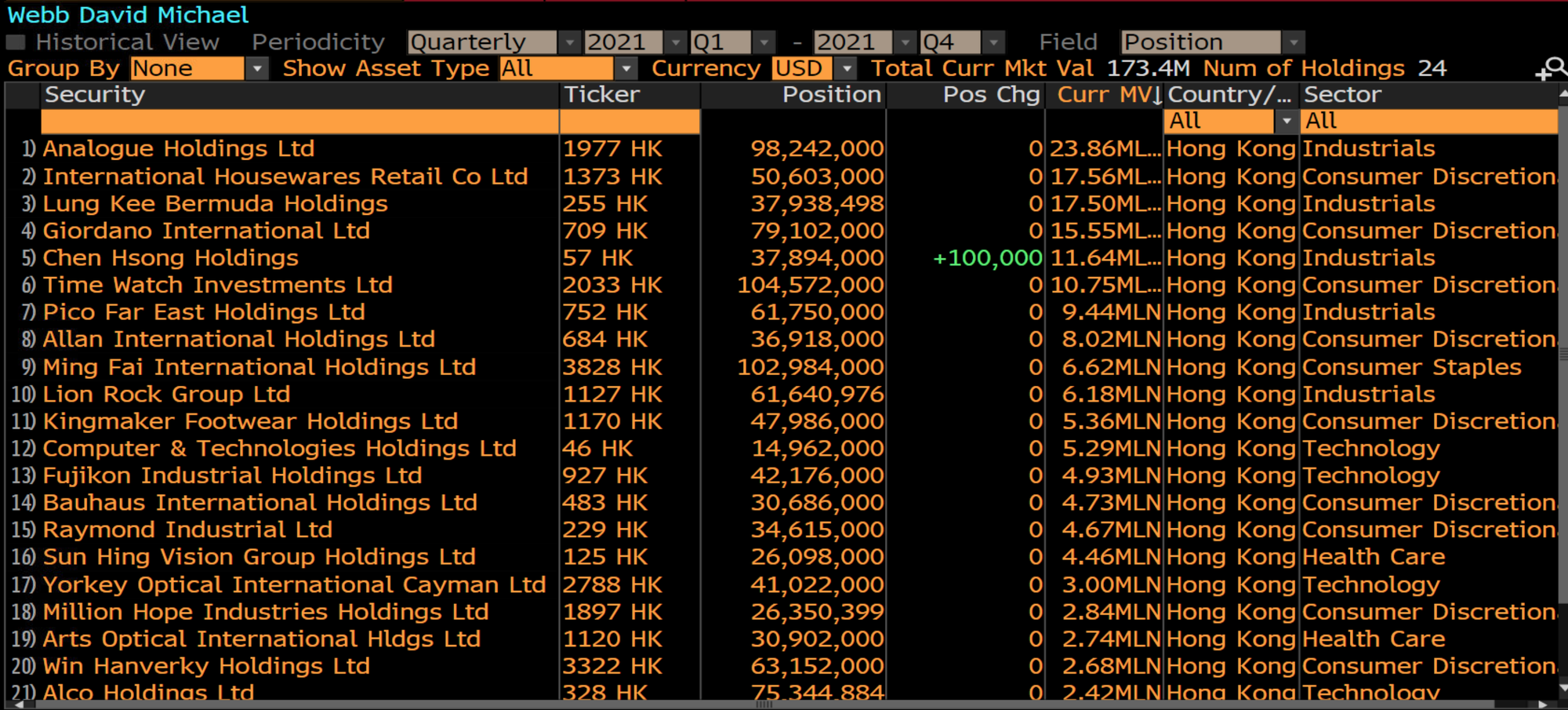

David Webb

David Webb is a Hong Kong-based activist investor with an excellent track record in Hong Kong small-caps. He has been brilliant at spotting companies with decent corporate governance trading at low multiples and seeing them rerate. His 2001-2009 Christmas picks were legendary.

His Webb-site.com is an excellent resource for articles regarding Hong Kong corporate governance reforms, but it also has a database of officer, adviser and shareholder relationships across Hong Kong corporates.

Unfortunately, David Webb has recently been diagnosed with cancer, but he remains active in the markets.

Analogue Holdings provides escalator installation and maintenance. The company has grown enormously over the past few years yet continues to trade at 8x P/E despite a large cash pile. I cannot help wonder whether it might benefit from Carrie Lam’s proposed “Northern Metropolis” in the New Territories, where almost 1 million flats are built. Perhaps Analogue Holdings will be a beneficiary, perhaps not.

Being Swedish, I know International Housewares Retail very well since it used to be owned by Stockholm-based private equity firm EQT. International Housewares Retail runs the retail chain Japan Home, which has a profitable Hong Kong operation but is less successful in other parts of Asia. I like the long-term story, but I fear that the current earnings might have been boosted temporarily by pandemic-related home furnishing demand and, therefore, not sustainable.

Lung Kee manufactures metal products. The dividend yield of 9% is attractive. Otherwise, I don’t quite understand why one would bother with such a commodity business. CNC machine maker Chen Hsong seems to be a commodity business as well.

I covered Giordano in brief in this prior thematic. Very cheap indeed. But a business in decline. It may be worth something, even in run-off mode. Hard to get excited about it, however.

I pitched Pico Far East in this prior deep-dive, and I consider the stock undervalued in a scenario where the Chinese borders open up completely.

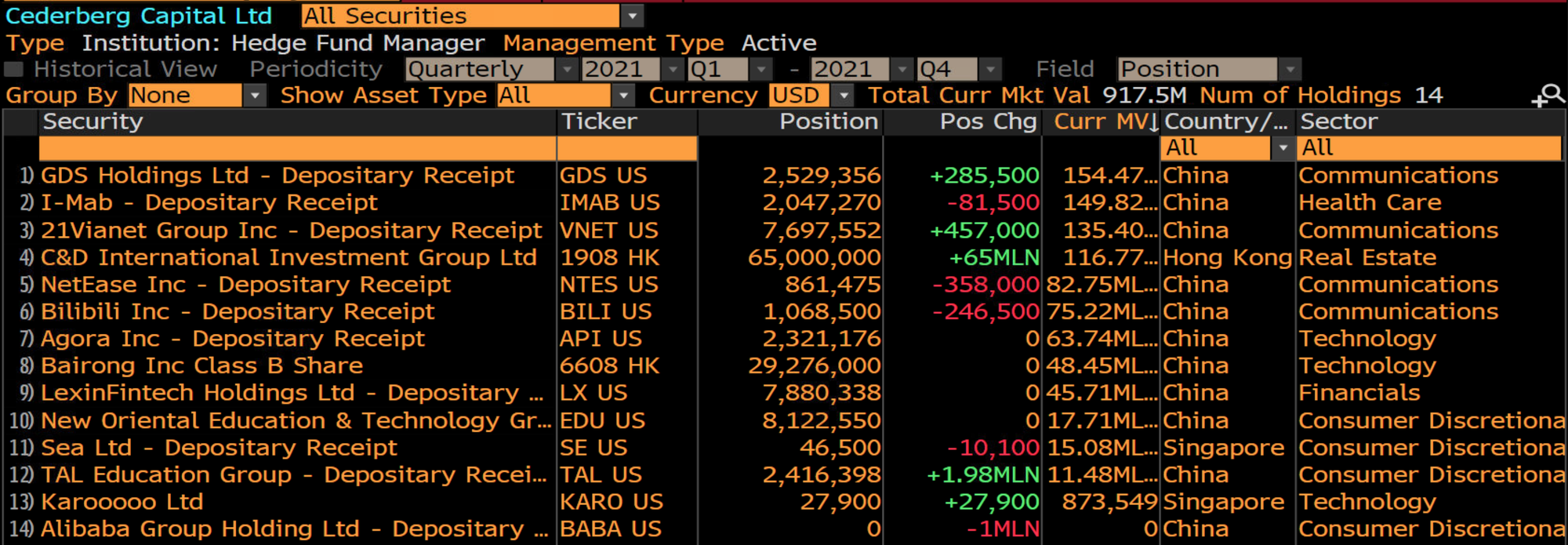

Cederberg Capital

Cederberg Capital is one of my favourite China-focused fund managers out there. The company is run by South African Dawid Krige, who runs the business out of London. Here is a recent interview with Dawid Krige for those who want to learn more about him. I believe that the funds are long-only, including the flagship Cederberg Greater China Equity Fund.

Cederberg’s analyst Skye Chen pitched oncology-focused biotech company I-Mab in a recent video on Vimeo. Analysing biotech companies - especially Chinese biotech companies - is beyond my capabilities, so I will not offer a view.

The rent of Cederberg’s portfolio is a who’s-who of China Internet, with high-quality stocks such as NetEase, Bilibili, 21Vianet and GDS Holdings. There is also ownership of Chinese tuition companies TAL Education and New Oriental, which have recently fallen from grace due to new government regulations.

The stock that stands out to me the most is Singapore-based Karooooo Ltd (yes, with five o’s). Karooooo is a holding company for “Cartrack”, a data analytics company. The stock is trading at 12x EBITDA, which I guess should be considered inexpensive in the SaaS world. Here is a recent write-up on Cartrack.

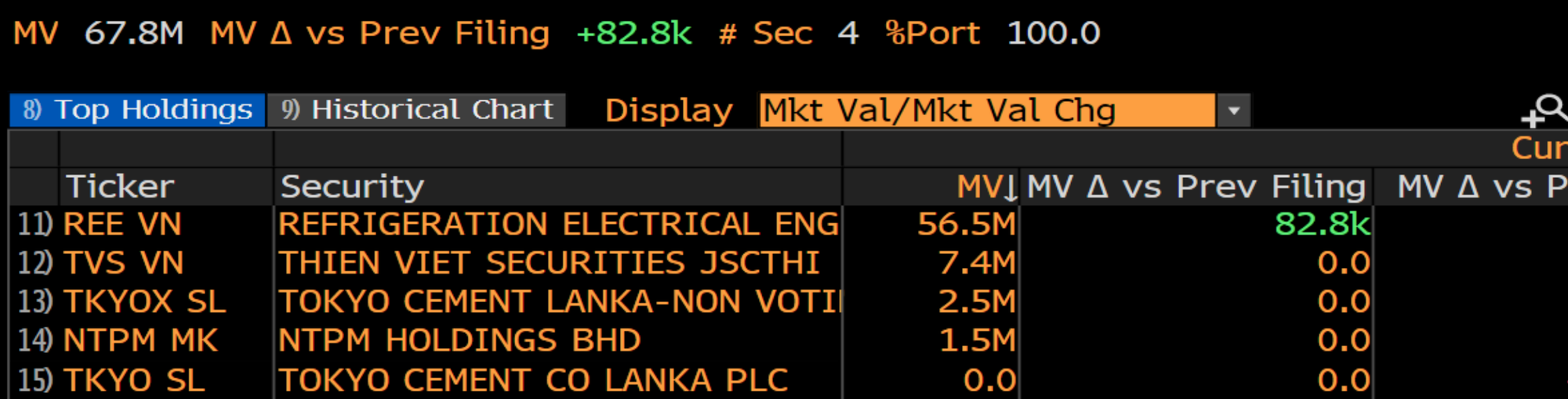

Apollo Investment

Malaysia-based investor Claire Barnes has an incredible track record since starting her Apollo Asia Fund in 1997. I wrote about her 1995 book Asia’s Investment Prophets here. Today, the Apollo Asia Fund has 37% of its portfolio in Vietnamese stocks, which happens to be one of the strongest performing stock markets globally over the past year.

Refrigeration Electrical Engineering (REEC) produces central air conditioning systems, owns power generation assets, and develops property. Though the stock has more than doubled in the past year, it still trades at just 12x earnings. Another major shareholder of REEC is Jardine Cycle & Carriage, which I wrote about in this deep-dive.

Thien Viet Securities (TVS) is a Hanoi-based investment bank trading at 7x P/E and with ROEs in the high teens. Although there are several positive long-term trends, including a higher market cap/GDP for Vietnam and a growing derivatives market, the stock now trades at 2.3x book vs 1.0x historically.

Tokyo Cement Lanka manufactures cement products in Sri Lanka. Although I don’t know much about either cement or Sri Lanka, the stock appears inexpensive at 4x P/E and 5x EV/EBIT.

NTPM Holdings manufactures tissue papers, toilet rolls and similar paper products. The stock trades at 11x trailing EBIT and 9x trailing EPS, though I’m not sure if the pandemic temporarily boosted the current level of earnings.

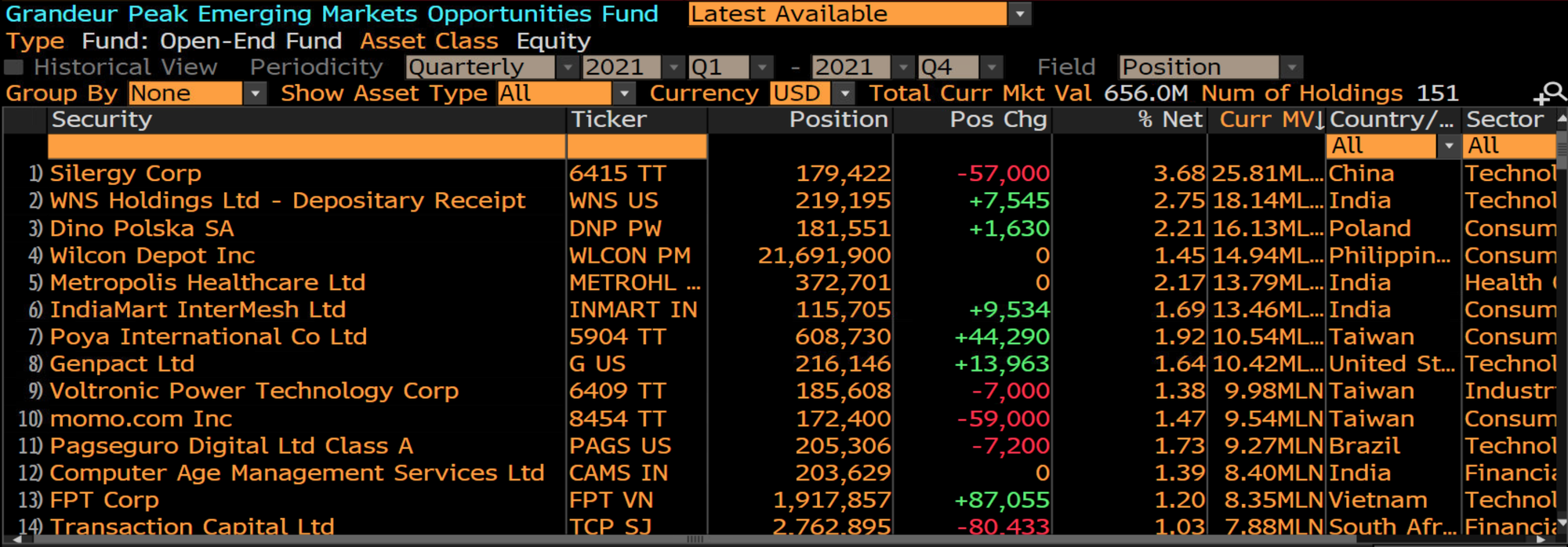

Grandeur Peak EM Opportunities Fund

Grandeur Peak is a global mid-cap fund run out of Denver, Colorado, in the United States. Their Emerging Markets Opportunities Fund has compounded at a 9% rate since 2013, several percentage points higher than the index. It has a significant Asia focus, despite little exposure to Chinese tech stocks.

One of the fund’s largest positions is Taiwan-listed Silergy, which produces analogue semiconductor chips used in LED lights. While growth has accelerated during the pandemic, it now trades at 71x forward earnings.

Another large holding is the Philippines company Wilcon Depot, which may have become a significant shareholding through the near-doubling in the stock price over the past year. The company produces home improvement and construction materials and has seen strong demand during the pandemic.

The fund is also a significant shareholder of well-run e-commerce company momo.com, which has strength in women’s products and dominated the Taiwanese e-commerce market before Shopee entered the scene.

Another significant holding is Vietnamese software outsourcing company and telecom operator FPT, which has more than doubled over from a very low multiple over the past year.

Outside of the fund’s top-15 list, I’m most intrigued by their investments in Indonesian auto supplier Selamat Sempurna, Indonesian dairy company Ultrajaya (deep-dive here), Indonesian flooring maker Arwana Citramulia, Philippine grocery retailer Puregold and Philippine mall operator Robinson Land.

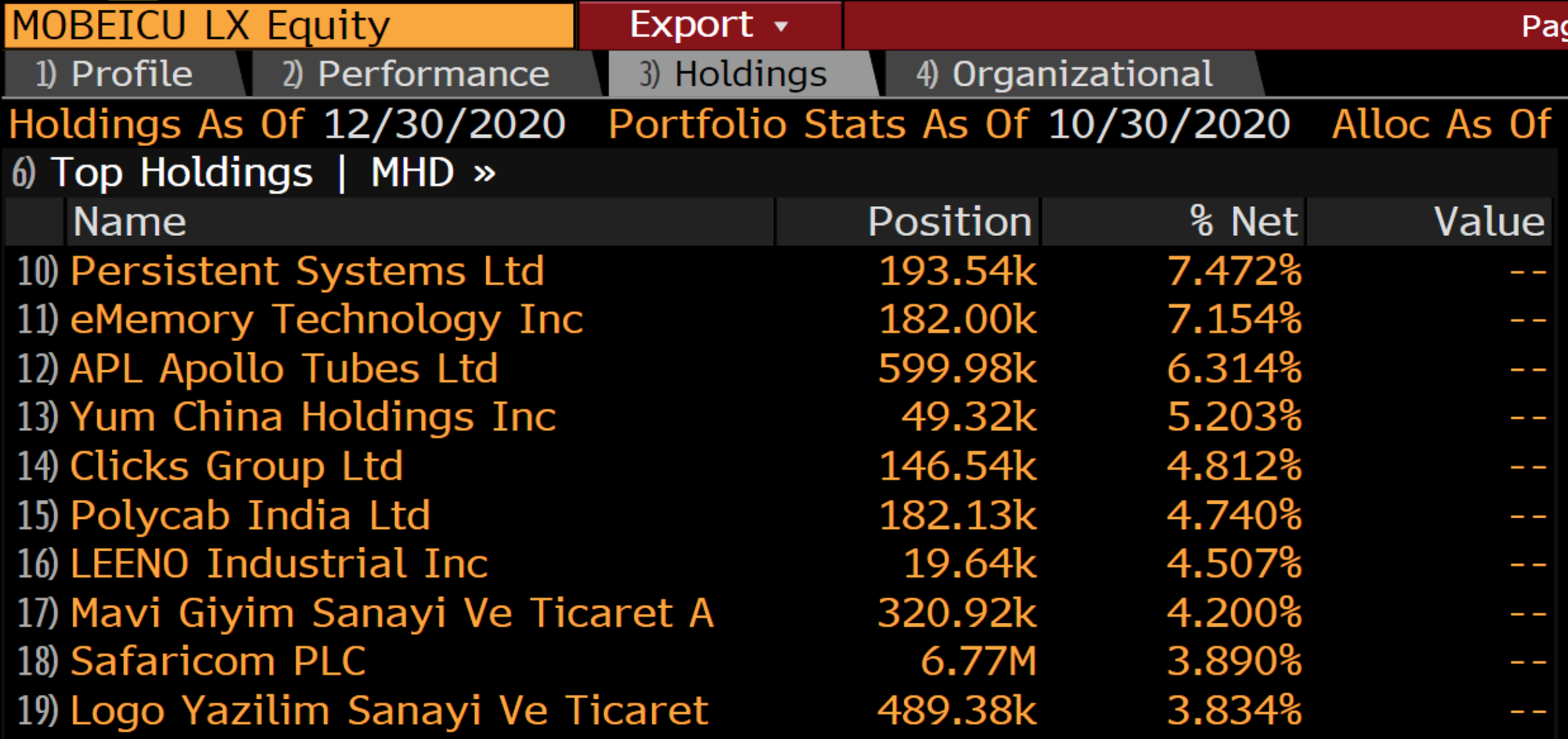

Mobius Emerging Markets Fund

Mark Mobius is an American with a German passport that took over the Templeton Emerging Market Investment Trust in 1987. He has written several books about his experiences investing in emerging markets, including Passport for Profits.

In 2018, he resigned from Franklin Templeton and started his own company Mobius Capital Partners, which runs the Mobius Emerging Markets Fund. The fund is geared towards growth stocks with an average P/E of 31x.

As of late 2020, the fund has significant exposure to India through software outsourcing company Persistent Systems, steel tube maker Apollo Tubes and electronic equipment maker Polycab India. All trading at very high multiples.

He has also invested in the computer memory company eMemory Technology, a LogicNVM flash memory technology developer. I will be the first to admit that I don’t know whether the company’s LogicNVM technology is significant or not.

Other stocks in the portfolio include Chinese KFC and Pizza Hut franchisee Yum China, which in my view, is one of the best-run companies in China I have ever come across. There is great potential for the number of KFC outlets to increase, though much of that growth is already priced-in at P/E 35x.

Korean semiconductor testing equipment maker LEENO Industrial. Leeno is delivering 35% operating margins against a peer average of mid-teens in a highly fragmented industry. It does not appear cheap at first glance, having tripled in a year and trading at 34x P/E.

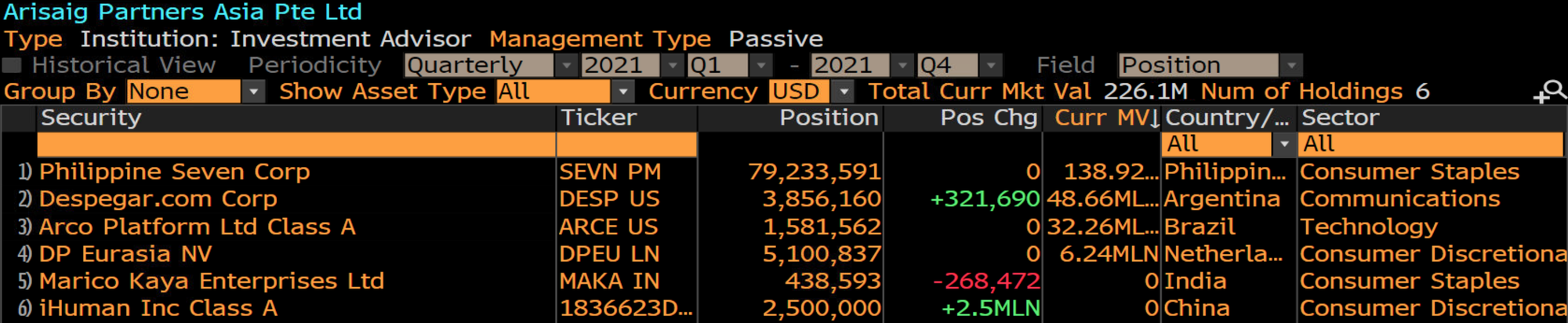

Arisaig Partners

Arisaig Partners is a Singapore-based fund manager with a 25-year track record and an AUM of US$3.1 billion. The track record of their Asia Fund is decent, with a 13% annualised return over 20 years. I appreciated their thoughtful commentary about investing in China published earlier this year.

There is limited disclosure about Arisaig’s investments, but I’m noting that they own 79 million shares of Philippine Seven Corp, a 7-Eleven franchisee in the Philippines. Too pricey for me at 51x 2019 actual earnings.

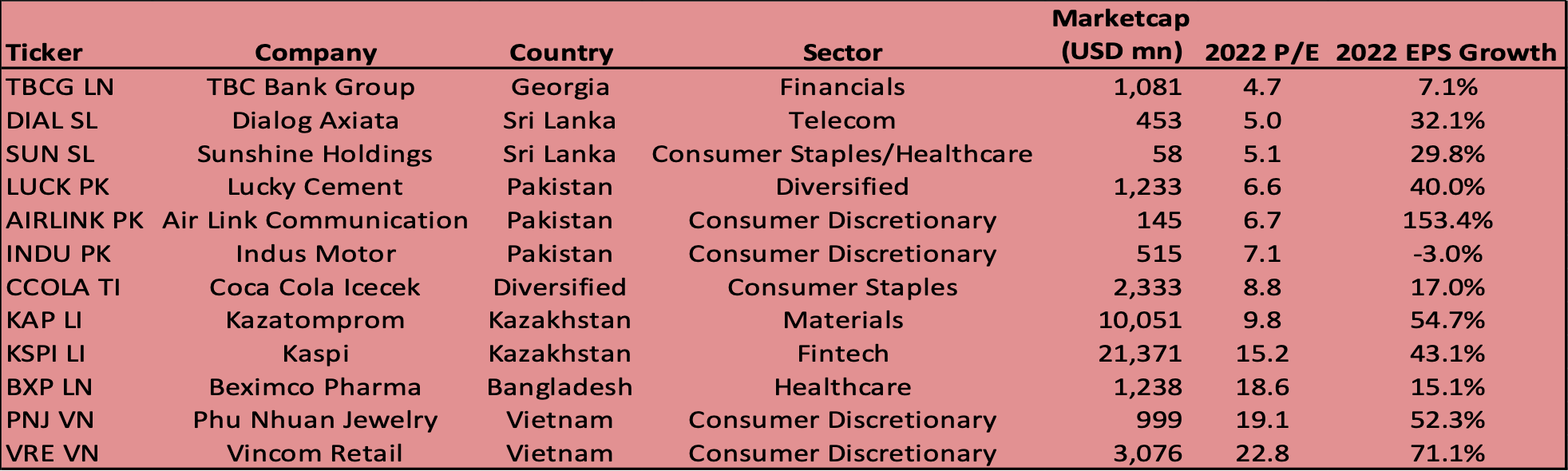

AFC Asia Frontier Fund

Asia Frontier Capital runs the AFC Asia Frontier Fund, which invests in frontier markets such as Bangladesh, Kazakhstan, Pakistan, Sri Lanka and Vietnam. The company was founded by a European called Thomas Hugger. The fund’s holdings were disclosed in a recent investor presentation available here.

In Sri Lanka, AFC Asia Frontier Fund owns Dialog Axiata, a Sri Lankan telecom operator trading at P/E 6x and a 7.6% dividend yield. The company has doubled earnings in the past six years in US Dollar terms. It also owns Sunshine Holdings distributes pharmaceuticals, and runs a retail pharmacy chain called Healthguard. While earnings benefitted from the pandemic, even against 2019 numbers, the P/E multiple is not more than 12x.

In Pakistan, the fund owns Lucky Cement trades at 10x earnings, though against record-high profits following the pandemic. Air Link Communication retails mobile phones, a seemingly commoditised business, and trades at 7x P/E. Indus Motor is a JV partner of Toyota in Pakistan, offering assembly and retailing of autos. A P/E of 6x looks very attractive to me.

In Kazakhstan, AFC Asia Frontier Fund owns the online payment platform and lender Kaspi and uranium mining giant Kazatomprom, which trade at P/E 24x and 20x, respectively.

For Vietnam, the fund owns Vincom Retail, which owns and develops shopping malls. Vingroup is a well-connected company, but the stock does not seem mispriced at 28x P/E. Gold merchant Phu Nhuan Jewelry is another high-quality company. Still, the big question is whether it has a brand name protecting it from the competition and how much jewellery consumption will rise from already-high levels. It has a P/E of 21x.

Conclusions

- I’m intrigued by Hong Kong elevator service company Analogue Holdings and can’t wait to dig deeper.

- In Japan, I’m interested in JAFCO as I suspect its book value may understate NAV in this ongoing tech bull market. Toyo Seikan was disrupted by COVID-19 and may someday recover.

- In Indonesia, I have added Arwana Citramulia to my to-do list, given the ongoing turnaround in the Indonesian property market.

- In the Philippines, Puregold and Robinson Land are already on my radar. Puregold is trading at a low multiple, and its subsidiary S&R is like a Philippine version of Costco. Robinson Land may not own top-tier malls, but the company will soon be on a recovery path from COVID-19, and there is significant insider buying.

- Among frontier markets, Indus Motor at P/E 7x looks like a steal. Same with Tokyo Cement Lanka at P/E 4x. Developed market cement companies tend to trade at mid-teens multiples, and I believe the quality of cement businesses is higher than generally recognised.

Thanks for reading!

Sign up for over 20 deep-dive reports on Asian stocks per year and full disclosure of my personal portfolio.