Table of Contents

Disclaimer: This article constitutes the author’s personal views and is for entertainment and educational purposes only. It is not to be construed as financial advice in any shape or form. Please do your own research and seek your own advice from a qualified financial advisor. From time to time, the author might hold positions in the stocks mentioned below consistent with the views and opinions expressed in this article. This is a disclosure, not a recommendation to buy or sell stocks.

In early 2024, South Korea's Financial Services Commission decided to emulate Japan's shareholder reforms by launching its own "Corporate Value-Up" program.

At the center of the program were voluntary disclosures by Korea's listed companies. Just like in Japan, listed companies were encouraged to publish long-term "Value-Up plans" that outlined how management would improve capital allocation and the company's valuation.

The best-scoring companies were included in a new "Korea Value-Up Index" sponsored by the Korea Exchange. Scores were calculated based on profitability and whether companies are actively improving their corporate governance. It became a bigger success than I had expected. If you go to the Korea Exchange website today, the first number you'll see is the Korea Value-Up Index, and only then, KOSPI. So it shows you how seriously the exchange is taking the new program.

The Value-Up Index is now used as a benchmark for many ETFs and financial products bought by Korean pension funds and other institutional investors. So if a company is included, its valuation is likely to rise.

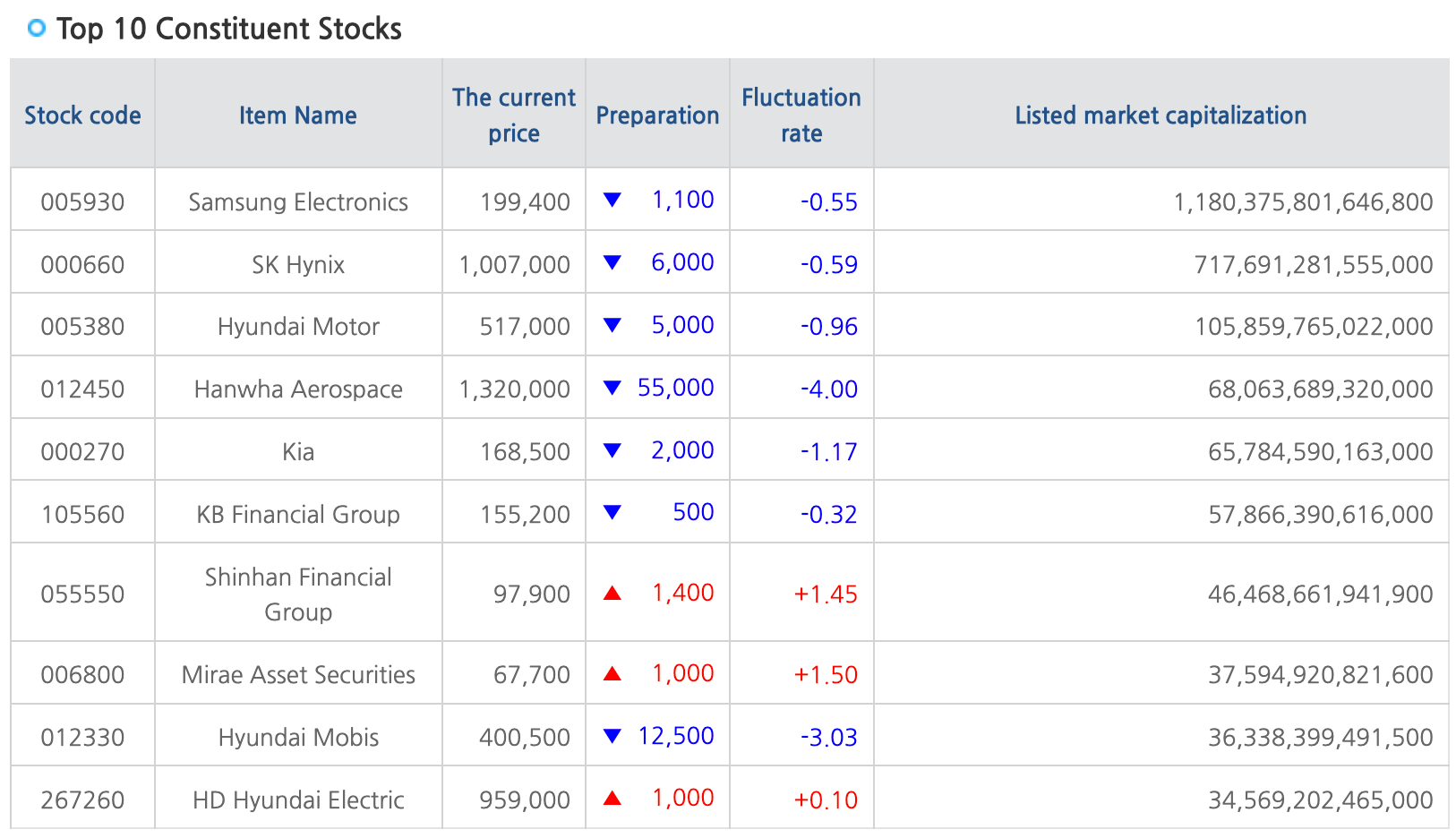

Today, the top 10 constituents include SK Hynix, Shinhan Financial, and Hanwha Aerospace:

Separately, the Korea Exchange also built a website where listed companies are ranked on Price/Book, Price/Earnings, return on equity, and dividend payout ratios.

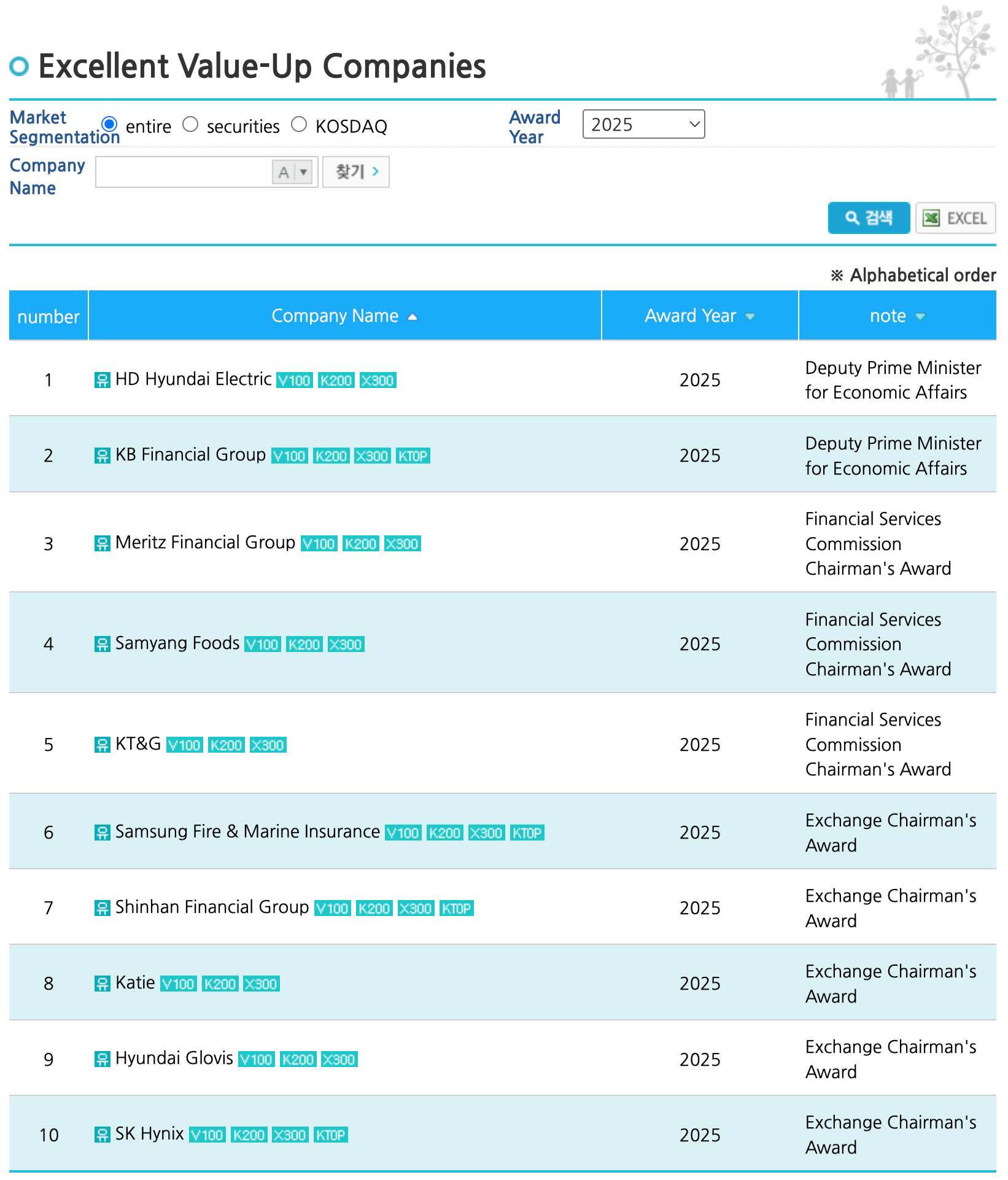

The same website also has a list of the companies that received Excellent Value-Up Company Awards in 2025:

To receive this award, companies needed strong disclosures, a feasible plan to improve corporate returns, and key performance indicators that beat their sector peers.

Long-time readers of Asian Century Stocks probably remember Samyang Foods, the buldak ramen maker I wrote about in 2024. Samyang Foods issued its first Value-Up plan on 26 March 2025, outlining ambitions to expand its production capacity and drive higher returns on equity through higher sales volumes and factory automation.

Being curious about the plans that have been announced, I went to the Korea Investors' Network of Disclosure (KIND) website to get the full list of recently announced Corporate Value-Up plans.

Within the KOSPI, I found 304 announcements of Corporate Value-Up plans since May 2024. Out of those, I managed to download 132 companies that released full Value-Up investment decks. You can download my full list here:

I only included each company's latest Value-Up plans, ignoring the originals. Many are in Korean language, so if you don't speak Korean you will have to use Google Translate or NotebookLM to understand their content.

I went through the list today, and narrowed it down to five stocks worth highlighting. Some of these stocks have also been mentioned by Douglas Kim over at Smartkarma.

KT&G (033780 KS)

First, let's talk about KT&G, or Korea Tobacco & Ginseng (033780 KS — US$11 billion). It's South Korea's largest tobacco company, holding a 68% market share. It used to be an absolute monopoly, but it still has a distribution advantage. KT&G also has a global operation with sales in 50 countries and manufacturing hubs in Indonesia and Kazakhstan. Cigarettes are the mainstay product, but they also sell heat-not-burn devices in a partnership with Philip Morris.

What makes KT&G's Value-Up plan unique is its aggressiveness. Its 2025 target was to achieve a total cash return of over 100%, including a dividend above KRW 6,000. Such a payout ratio is unusual in South Korea. Consensus estimates the dividend to reach 6,345 per share in 2026. In addition to these shareholder returns, KT&G is now targeting returns from the sale of non-core assets. In 2026, KT&G targets a KRW 300 billion share buyback. And in March, KT&G announced that it will cancel its entire Treasury stock, equivalent to 9.5% of shares outstanding.

After the share cancellation, it will have just north of 100 million shares outstanding. Against the 2026 consensus net income, KT&G will then trade at 12.7x P/E. If capital returns hit 100%, we could see an almost 8% dividend/buyback yield.

Nongshim (004370 KS)

Nongshim (004370 KS KS — US$1.5 billion) is a Korean packaged food company, most known for its ramyeon noodles. But it also makes chips, crackers, bottled water, and ready-to-eat food. 72% of revenue is domestic, and 28% is from overseas customers. It also has a holding company with a similar name that the family uses to control the operating business.

The company is currently building a new factory in Busan serving the export market. International businesses are growing by +14% per year, and it looks like they're benefiting from the broad popularity of Korean food overseas.

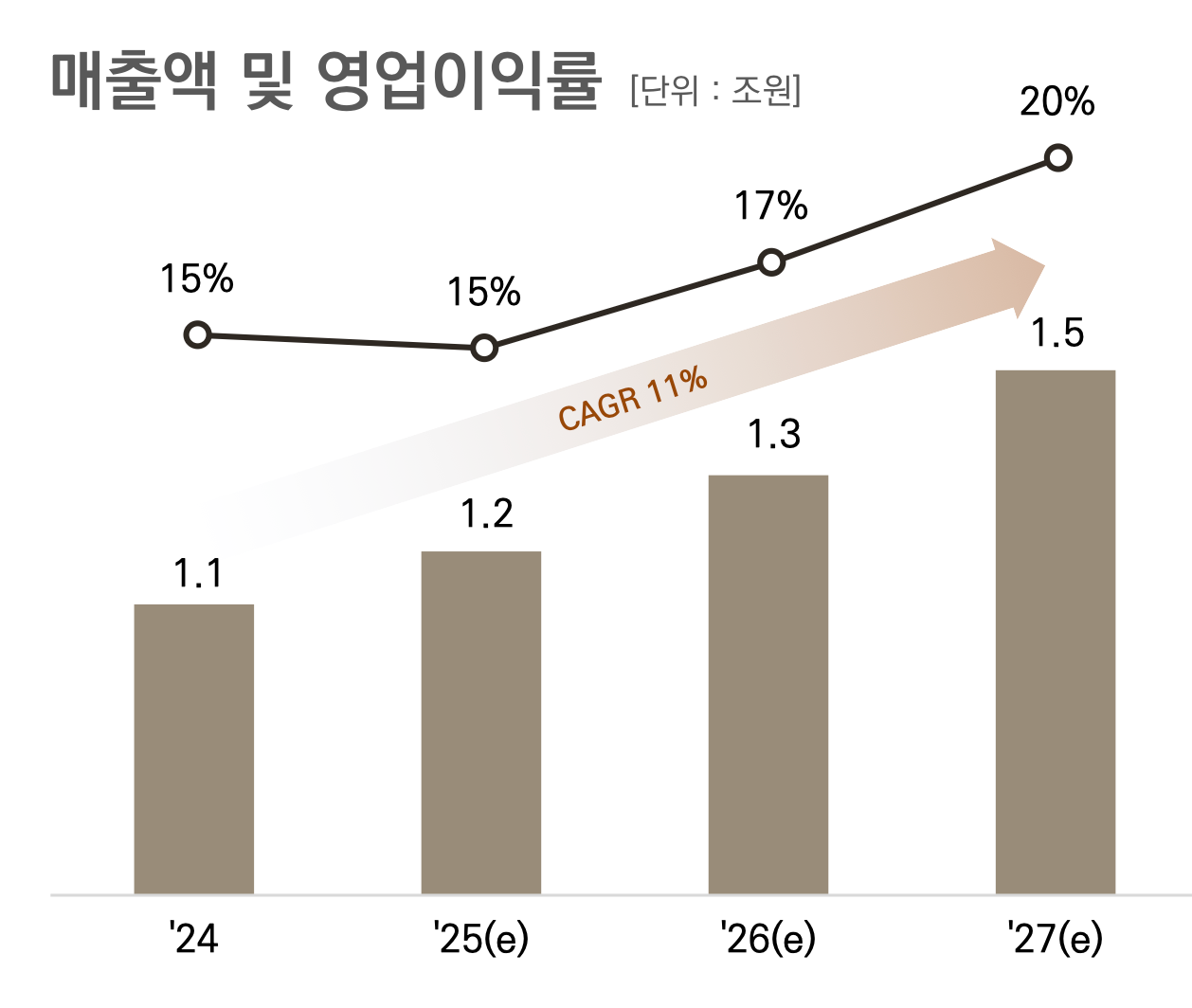

Nongshim's Value-Up plan targets KRW 7.3 trillion in revenues and an operating margin of 10% by 2030. What's fascinating about the plan to me is that they want to increase the overseas share to 61%, up from only 28% today. Capital returns are more modest, targeting only 25% and a return on equity of only 10%.

Still, KRW 730 billion in operating profit implies an EV/EBIT of 3.0x. Against today's earnings, the P/E is a more normal 12.4x. We have seen some modest insider buying this year, including a cluster buy in January 2026.

Paradise (034230 KS)

Casino operator Paradise (034230 KS — US$1.1 billion) is almost a monopoly in the market for foreigner-only casinos. It owns four casinos across Seoul, Incheon, Busan, and Jeju Island. Its flagship, Paradise City, is a joint venture with Japan's Sega Sammy and an integrated resort featuring 5-star hotels, a theme park, exhibition centers, and other facilities.

Many of its customers come from Japan and China. It should therefore benefit from the easing of Korean visa rules and the rerouting of Chinese tourism away from Japan to South Korea.

Paradise's Value-Up plan targets KRW 1.5 trillion in sales and an operating margin of 20% by 2027e. That would imply an EV/EBIT of 8.3x.

NICE Information Service (030190 KS)

NICE Information Service (030190 KS — US$665 million) operates South Korea's largest credit bureau, collecting data on borrowers and selling it to banks and corporations. The company has scoring models that help banks figure out which borrowers are likely to default. Their market share is about 70% for individuals and 34% for the corporate market, where it's competing with Korea Ratings.

The Value-Up plan targets a 5% annual increase in dividends. It's committed to paying out 35% of earnings as dividends and reducing the share count by 1% per year. NICE has also mentioned revenue and operating profit targets of KRW 690 billion and KRW 110 billion, respectively, for 2027.

The stock currently trades at 11.2x P/E. If the operating profit target is reached, however, it will end up at 7.7x EV/EBIT.

Muhak (033920 KS)

South Korea's Muhak (033920 KS — US$162 million) is the leading soju brand in the Southeast. While HiteJinro dominates Korea overall, Muhak's "Good Day" soju brand has its loyal fans across Busan, Ulsan and surrounding areas. The product portfolio includes fruit-flavored soju, distilled soju and traditional rice wine.

Muhak's Value-Up Plan aims to resolve its chronic undervaluation by improving its return on equity to 10%. It's also introduced a target Price/Book of 0.7x. And while Muhak's products are primarily domestically oriented (I can't find its soju in Singapore), it's now trying to increase the export share to 15%. While the annual dividend of KRW 520 is modest, Muhak is also committed to allocating 5% of net income to share buybacks and cancelling the shares purchased.

The stock now trades at 9.1x and 0.4x book. If they ever reach their 10% return on equity target, the P/E multiple would compress significantly. While the company isn't growing much, Muhak now offers a 6.3% dividend yield, which is high by Korean standards.

But there are tons of other Value-Up plans on my list. If you've identified any other companies with ambitious targets, I'd be very curious to hear about them.

{kind=link}