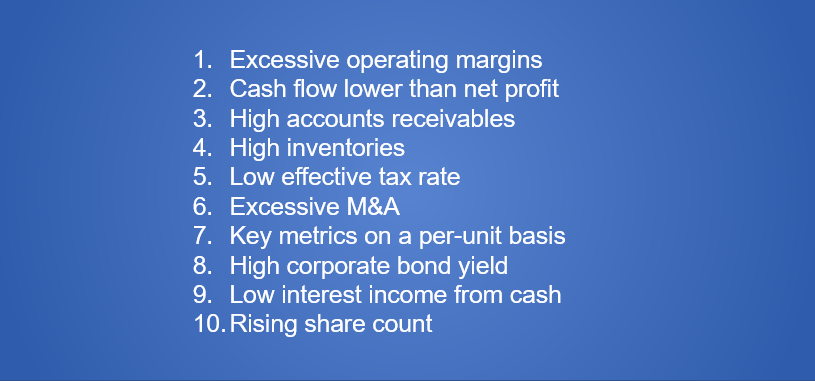

Simple tricks to spot fraud

Five stocks with insider buying in China, South Korea, Indonesia and Thailand

The leader in cinema equipment at 9x P/E

No signs of disruption from generative AI

Port terminal operating system developer at 6x P/E