"I'm a new investor. Where do I begin?"

Disclaimer: This article constitutes the author’s personal views only and is for entertainment purposes only. It is not to be construed as financial advice in any shape or form. Please do your own research and seek your own advice from a qualified financial advisor. This is a disclosure - not recommendations to buy or sell financial assets.

I received this question from a local friend:

“I have money in the bank that I don’t know what to do with. I have never invested in stocks before. Where do I begin?”

The issue that I think she and many other retail investors face is that they want to avoid making major mistakes. They don’t want to gamble away their hard-earned cash. So instead they keep their money in the bank, where it loses purchasing power year after year.

I will try to provide an alternative: a step-by-step guide on how you can invest your capital even if you don’t have a lot of experience.

Disclaimer: This information is general in nature and has not taken into account your personal financial position or objectives. This article is for information purposes only and is not intended to be investment advice. Before proceeding please refer to a licensed professional adviser.

Some general advice

Here are a few general principles that I think are key:

- Diversify broadly. If you don’t know what you’re doing, you need to diversify broadly: across asset classes, across geographies and across industry sectors. After a few years of experience, you can start to concentrate and make specific bets.

- Avoid leverage. For proper compounding of wealth, you’ll want to avoid any risk of ruin. If you take on full-recourse margin debt in your stock portfolio and the market falls 50%, your entire portfolio could well blow up. If you buy a house, some leverage is fine.

- Make contrarian bets. The only way a stock can go up if is other people agree with you - after you’ve bought the stock. Don’t buy Tesla just because everybody else is.

- Focus on long-term value. You can’t predict short-term stock prices. But you can predict certain underlying long-term trends. Buying a high-quality company at a low price and then wait for a few years is the easiest way to make money.

1. First invest in freehold property with leverage

Most individuals who buy property tend to do well over the long run. There are two reasons: annual inflation of 3-4% and leverage.

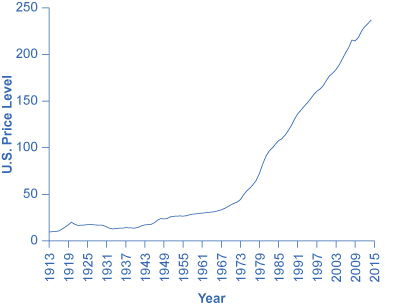

The inflation rate in the US since the end of the gold standard in 1971 has been high. Headline inflation numbers understate true underlying inflation through hedonic price adjustments. Also, inflation is skewed in the sense that goods price inflation has kept coming down over the past few decades, yet the price of services such as healthcare and college has skyrocketed.

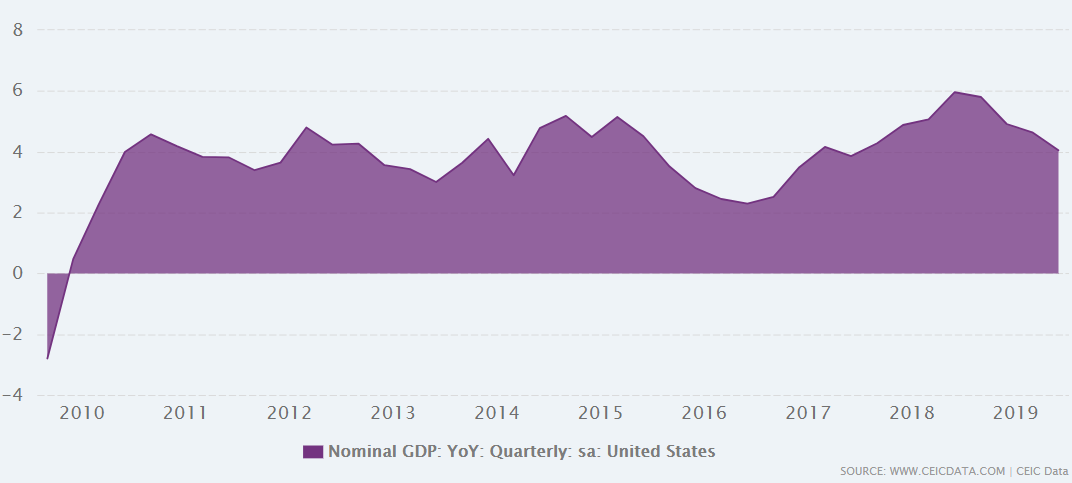

The value of land should in theory rise in line with nominal incomes, or at least with median nominal income. In the aggregate, nominal GDP in the US has grown about 4% per year and somewhat lower in the Eurozone and Japan. So I think you can expect the value of land to rise as much as 4% per year, depending on where you live.

Building structures do depreciate, so this 4% estimate is probably a ceiling in how fast the value of your house can appreciate.

Another factor that makes housing a great investment is leverage. Housing often carries initial loan-to-value ratios of up to 80%. So a 3% yearly increase in value at 5x leverage implies a 15% yearly return on your initial deposit. The exact calculations get more complex because of the opportunity cost from not renting as well as other factors such as maintenance. But roughly speaking, this is what you should expect. And while you might feel tempted to sell your stocks in a stock market panic, you’re unlikely to sell your house just because the value of it drops temporarily.

I’d say though, if housing prices get to extreme levels, you might want to hold off buying. The best way to measure housing prices in my view is the rental yield (how much your property could be rented out for per year / the purchase price).

If the rental yield goes below say ~4%, expect the above 15% yearly return on your housing deposit to drop. At a 2% rental yield and a 3% yearly rent increase, it will take over 20 years for the rental yield to hit a more “normal” 4% level.

My recommendation is that if rental yields are much lower than 4%, perhaps wait to buy a house until prices become a bit more attractive. The best time to buy a house is usually when unemployment is high or when interest rates spike.

Also, note that I’m talking about freehold property here. China’s 70-year land leases and Singapore’s 99-year HDB leaseholds depreciate significantly every year. In these cases, leverage actually works against you. So if leaseholds are your only options, then focusing on stocks might be a better way to grow your wealth.

2. Set up an online brokerage account

Online brokerage platforms Interactive Brokers and Saxo Bank are both decent for developed markets. In Asia, I find Monex (Japan) or Boom Securities (Hong Kong) the best for retail investors. I don’t get any money for recommending them. I just think they’re good because of their low commission rates and acceptable trade execution.

The more you venture into emerging markets, the more careful you should be. Many platforms charge >1% for FX transactions with very little transparency about pricing. Add commission & poor stock trading execution and you might end up paying several per cent for a single transaction. While you can trade developed market stocks actively, you’ll want to be more long-term when it comes to investing in emerging markets. In such markets, FX transaction fees, commissions and bid-ask spreads can kill your portfolio if you trade too actively.

3. Diversify broadly

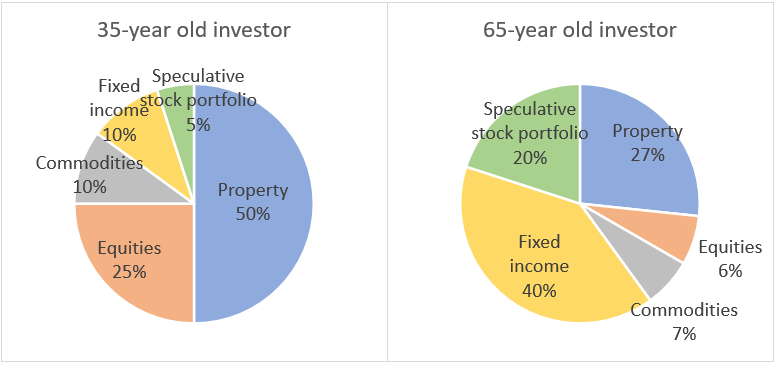

The average investor should diversify broadly across the major asset classes: property, equities, cash (short-term fixed income securities), bonds (long-term fixed income securities), and commodities.

Make sure that you have enough liquidity to meet short-term obligations, but enough long-term investments (property, stocks) to build capital gains in inflationary environments. Investors near retirement should be weighted more towards fixed-income securities. Younger investors should be weighted more towards more volatile but inflation-protected securities such as stocks.

ETF can help you with broad diversification. They’re great in that they keep fees low and enable you to diversify across a range of assets. But I’d still be very selective when it comes to ETFs, for the following reasons:

- Distorted exposure: Most ETFs are heavily weighted towards large caps, heavily weighted towards US stocks and heavily weighted towards tech. Almost all major indices are now value-weighted. ETFs tracking the MSCI World index now has a 67% allocation to the United States compared to America’s 16% share of world GDP. Top positions in MSCI China’s Value Index include NIO and Meituan - stocks that I think no professional investor would consider being value stocks. ETFs are not always what they seem to be.

- Commodity ETFs investing in derivatives: Most retail investors think that they’re buying oil in an ETF such as the United States Oil fund (USO) or the ProShares Ultra Bloomberg Crude Oil ETF (UCO). But they’re not. They are buying a portfolio of derivatives that typically lose value every month even if the commodity price stays flat (a negative so-called roll-yield). That’s true for many commodity ETFs, if not most.

- Liquidity mismatches: Some ETFs are invested in illiquid underlying securities. That could be a problem in case there is a panic. While ETFs can be sold in a millisecond, that is not always the case for their underlying assets. So in a panic, with value-insensitive ETF owners selling their ETFs at any price, that could lead to a cascade of lower prices in underlying securities. Corporate bond ETFs come to mind.

I suggest buying equal-weighted ETFs for stocks. The reason is that I think we’re in a tech bubble at the moment. Value-weighted ETFs will then overweight the stocks that are currently the most overvalued. Equal-weighted ETFs offer equal exposure to stocks regardless of their market capitalization. They also offer better diversification.

Here are a few suggestions on US-focused equal-weighted stock index ETFs:

- Invesco S&P 500 Equal Weight ETF (RSP US)

- iShares Russell MidCap ETF (IWR US)

- S&P 600 Small Cap Equal Weight ETF (EWSC US)

- Russell 1000 Equal Weight ETF (EWRI US)

Here are a few equal-weighted US sector ETFs if you want specific industry exposure:

- Invesco S&P 500 Equal Weight Materials ETF (Basic Materials) (RTM US)

- Invesco S&P 500 Equal Weight Consumer ETF (Consumer Discretionary) (RCD US)

- Invesco S&P 500 Equal Weight Consumer Staples ETF (Consumer Staples) (RHS US)

- Invesco S&P 500 Equal Weight Energy ETF (Energy) (RYE US)

- Invesco S&P 500 Equal Weight Financial Services ETF (Financial Services) (RYF US)

- Invesco S&P 500 Equal Weight Health Care ETF (Health Care) (RYH US)

- Invesco S&P 500 Equal Weight Industrials ETF (Industrials) (RGI US)

- Invesco S&P 500 Equal Weight Technology ETF (Technology) (RYT US)

- Invesco S&P 500 Equal Weight Utilities ETF (Utilities) (RYU US)

Here are a few global equal-weighted stock index ETFs:

- VanEck Vectors Global Equal Weight ETF (TGET NA)

- VanEck Vectors European Equal Weight UCITS ETF (TEET NA)

- Invesco FTSE International Low Beta Equal Weight ETF (IDLB US)

- KraneShares Emerging Markets Consumer Technology Index ETF (KEMQ)

- iShares MSCI Japan Equal Weighted ETF (EWJE)

- Yinhua SSE (Shanghai) 50 Equal Weight Index ETF (510430 CH)

- First Trust India NIFTY 50 Equal Weight ETF (NFTY)

As for commodities, you can either own shares in miners or funds that own the actual underlying commodity. Commodities tend to do best when inflation surprises to the upside, as it did during the 1970s and the 1910s. In these types of environments, growth stocks don’t do as well. So you’ll need some type of commodity exposure, regardless of where you are in life.

- Sprott Physical Gold and Silver Trust (CEF US)

- Sprott Physical Gold Trust (PHYS US)

- Yellowcake uranium fund (YCA LN)

A few suggestions on fixed income instruments:

- iShares Global Government Bond UCITS ETF (IGLO LN)

- iShares Global Corporate Bond Index UCITS ETF (IBCQ GY)

How should you construct your portfolio?

- If you’re young and just purchased a house, the majority of your wealth should be tied up in a deposit for a house. The rest of your portfolio should be tied to assets that protect against inflation, including equities and commodities. Fixed income will be a drag on your portfolio and you won’t need the cash until your children go to college or you retire. Since at 35 you are unlikely to have accumulated much experience speculating in stocks, keep your active stock trading account a small percentage of your overall portfolio.

- If you’re close to retirement, a significant portion of your portfolio should be in fixed income instruments. This is to guarantee that you’ll be able to sustain your lifestyle for yet another 20 or so years. At this point, your mortgage will have been paid off, meaning that your the money tied up in your house will have grown in absolute terms. At this point, you are likely a much better stock picker and the part of your portfolio invested in individual stocks can be greater than before.

4. If you have an interest in stock speculation, experiment with small money and increase your exposure gradually

Now that you have constructed a well-diversified portfolio of assets, I suggest you create a sub-account purely for speculation in individual stocks. Prepare to spend at least three hours per week on it. It will take 1-2 market cycles before you can have confidence that you’ll be able to do well in all market climates. Increase your exposure to this sub-account gradually.

I suggest screening for stocks with the following characteristics:

- The company’s main product is unique and faces no direct competition. Customers are willing to pay way more than the price of it.

- The company still has the potential to double in size, if not more.

- The PE ratio should be below 20x. You can make an exception for stocks whose underlying growth rate is more than 20%. Just make sure that observed growth is sustainable and not just cyclical.

- Debt/revenue should be below 50% (the Rocketfinancial platform shows each stock’s net debt, just divide this number by last year’s revenues).

- Your retail investor friends should not know the company’s ticker, or be sceptical for whatever - typically unfounded - reason.

You will have a difficult time finding stocks that fulfil all of the above criteria. That’s okay. Keep looking and eventually, you will find say 5 stocks in that will be needed for enough diversification in a speculative portfolio. You can start by putting 20% of your portfolio in each stock you’ve chosen.

The best places to hunt for stocks are in your immediate vicinity. Look at companies that do something new or different and add value to customers. Pay attention to what products you buy or what products you are planning to buy. Get into the habit of Googling the company behind specific products that you love and then read up on them on Seeking Alpha or via the company presentation by Googling “[company] investor relations”.

Just to demonstrate the thinking process, here are a few examples of products that I know and love, having seen them in my immediate vicinity here in Singapore:

- Tiger balm, full write-up here

- Delfi chocolate, full write-up here

- Genki Sushi, full write-up here ($)

I’m not saying that this is the only way to make money in stocks. But it’s probably the only way that you - as a retail investor - have an edge. If you go into commodity speculation, FX trading, distressed debt etc. you’ll be facing tough competition by pros who have spent years honing their skills.

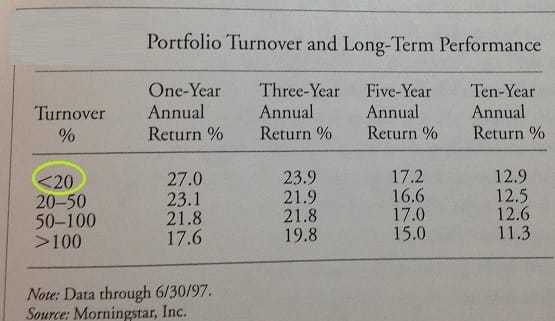

5. Check your portfolio a maximum 4x per year

The less you check your portfolio the better you will do. For an investor focused on fundamental analysis, checking stock prices more often than 4x per year is probably counter-productive. You’ll be tempted to sell when the stock price goes up and keen to buy more whenever the stock price goes down. That’s a terrible strategy. You’ll want to let your winners run - at least for a few years.

Why 4x per year? Because most companies report earnings quarterly. After quarterly earnings are released, check whether fundamentals are improving or deteriorating:

- Are they executing their strategy according to plan?

- Does their updated forward guidance suggest improving or deteriorating growth?

- Are margins expanding or contracting and why?

- Any major positive or negative surprise, and what does it imply for the future?

If fundamentals are improving and the stock price goes down, you buy more. If fundamentals are deteriorating and the stock price goes up, you sell. If there has been a massive shift in the company’s fundamentals you will want to act regardless of where the stock price has been trading recently.

The key information sources are the published results, accessible by Googling “[company name] investor relations” and 2) their earnings call transcript, typically available here. Margins can be gleaned from TIKR or Rocketfinancial.

Over time you’ll learn the pattern recognition needed to interpret quarterly results.

Conclusion

You don’t have to speculate in stocks just because your friends are. If your risk tolerance is low, diversify broadly and keep investing the same amount every month in your diversified portfolio. Freehold property should be your major focus. If you enjoy the challenge of picking stocks, go with small companies whose products you love while making sure the PE ratio is not yet in crazy territory. Or pick some of the ideas I have described on my Substack in the past, available here. Feel free to reach out at any time by replying to this e-mail or contact me via Twitter @Fritz844.

If you enjoyed this post and would like to read more, try the Asian Century Stocks subscription service - for the price of just a few weekly cappuccinos. Over 20x deep-dives per year, industry thematic reports and other Asia stock-related content.

Thanks for reading!

I love any feedback: just let me know what you think here.

If you found this post valuable, consider sharing it with your friends.