Hikari Tsushin's portfolio

Estimated reading time: 16 minutes

Disclaimer: Asian Century Stocks uses information sources believed to be reliable, but their accuracy cannot be guaranteed. The information contained in this publication is not intended to constitute individual investment advice and is not designed to meet your personal financial situation. The opinions expressed in such publications are those of the publisher and are subject to change without notice. You are advised to discuss your investment options with your financial advisers. Consult your financial adviser to understand whether any investment is suitable for your specific needs. I may, from time to time, have positions in the securities covered in the articles on this website. This is not a recommendation to buy or sell stocks.

Summary

- This write-up is about Hikari Tsushin — a Japanese sales organization run by a visionary founder called Yasumitsu Shigeta

- It’s been much talked about on Twitter and Substack, but few of the write-ups discuss Hikari Tsushin’s portfolio of publicly listed equities

- I am personally not particularly interested in Hikari Tsushin itself, as it is primarily a sales organization helping other businesses find customers

- But what I am impressed by is Hikari Tsushin’s capital allocation and investing discipline. You’ll find them on the shareholder register of some of Japan’s best-performing small caps.

- In this post, I identify 218 publicly listed Japanese companies where Hikari Tsushin is a 5% or larger shareholder. These companies are small, but often undervalued, and growing.

- In the past week, I’ve gone through this entire list and narrowed it down to ten companies that I think warrant further attention. It includes larger companies such as Daito Trust but also SaaS companies like Broadleaf.

In this post, I go through Hikari Tsushin’s history, its current valuation, its investment portfolio and ten holdings that I think warrant greater attention.

Table of contents

1. The company's background

2. Hikari Tsushin as an investment

3. The current portfolio

4. Ten Hikari stocks on my watch list

5. Conclusion1. The company's background

Japanese compounder stock Hikari Tsushin (9435 JP — US$13 billion) has been the subject of much discussion on Twitter.

Some people call it the “Berkshire of Japan”. Many find it encouraging to see a Japanese company that finally understands capital allocation. I am not sure I’d go that far, but the company is certainly worth a deeper look.

Hikari Tsushin was set up by an entrepreneur called Yasumitsu Shigeta back in 1988. He had just dropped out of college and was looking to make money fast. So he teamed up with a few friends to sell office phones door-to-door across Tokyo.

He chose the name “Hikari Tsushin”, meaning “light communication” in Japanese. At the time, Japan had just deregulated the telecom industry, so it was a market ripe for disruption. It terminated the monopoly that NTT had once had and allowed companies like Hikari to start selling telecom products to the general public.

The company was a sales organization from the start. Yasumitsu Shigeta hired young and hungry individuals eager to make a mark on the world, paying them nothing but commission and encouraging them to use hard sales tactics.

From 1993 onwards, Hikari Tsushin added mobile contracts to the mix, and growth took off like a rocket. By the late 1990s, it had set up 1,500 phone shops across Japan, becoming an Internet darling just a few years after its IPO.

At the peak of the Dotcom bubble, Yasumitsu Shigeta became one of Japan’s richest men. Investors competed with each other to figure out how big an impact the Internet could eventually have on our society.

And it all came crashing down. In the late 1990s, Hikari had increasingly turned to aggressive accounting to spur growth. For example, it had sold mobile phone contracts and booked all revenues on day one. It had fabricated contracts with the predecessor of Telecom company KDDI. Finally, Hikari had stuffed franchisee stores with inventory to boost quarterly revenue numbers.

The original guidance of JPY 6 billion in profit for the year 2000 turned into a loss of JPY 13 billion. In just six weeks, the stock price had lost 96% of its value. Shareholder lawsuits continued for years, and Hikari Tsushin’s reputation was shattered.

Part of the blame could surely be put on the company’s high-pressure sales tactics. Shigeta had hired high school graduates without career prospects and asked them to achieve his vision no matter what. The sales staff were likened to “street fighters”, doing whatever it takes to close deals.

After the crash, Shigeta sat down with his lieutenants to try to reimagine the business. He expanded beyond telecom into office suppliers to small- and medium-sized enterprises. The focus was now on recurring revenue business — anything that would make earnings stable and predictable.

However, the street fighter mentality remains. If you survive Hikari Tsushin’s Darwinian environment, you can achieve anything. The high-pressure sales model remains, often helping other companies sell products door-to-door. The sales tactics employed by Hikari Tsushin work, and despite the post-1999 crash, the company survived and has continued to thrive to this day.

2. Hikari Tsushin as an investment

In 2025, Hikari Tsushin continues to be a sales organization, with great success. It employs 20,000 people selling electricity and gas, telecom products, mineral water, insurance, office equipment and more. The contracts are long-term in nature, with 80% of revenue considered recurring. And the business throws off huge amounts of cash, which is then reinvested into stocks.

In the past few years, I’ve written about a large number of Japanese small caps. I’ve often been surprised to find Hikari Tsushin in the shareholder register, across niche businesses such as pet insurance company Anicom and SaaS company Poper. They clearly know what they’re doing.

Yasumitsu Shigeta has now stepped down, but CEO Hideaki Wada has similar views on investing and capital allocation. Jake Barfield’s interview with Wada was among the most refreshing I’ve ever heard in my life. Finally, someone who gets it!

Hideaki Wada and Yasumitsu Shigeta see capitalism as the answer to Japan’s troubles. They think that a lack of understanding of capital allocation is the reason why Japan, as a market, has been underperforming. Companies have been unable to lay off employees. CEOs do not need to take shareholder interests into account to retain their jobs.

At the same time, that spells opportunity for Hikari Tsushin itself. It’s able to buy stakes in high-quality companies cheaply, and then guide them in the right direction. In their main businesses, they strive for a 30% internal rate of return over a five-year period. And the equity portfolio has compounded at 17% per year over the past seven years, far above TOPIX. And they’ve been able to employ leverage, juicing returns further.

I’m not that interested in Hikari Tsushin itself. It does look undervalued, with the company quoting an intrinsic value of JPY 56,000 — far above the current share price of JPY 42,000. In its presentation materials, it reports look-through earnings on its investment portfolio of JPY 115 billion, which, along with core earnings, leads to total look-through earnings of JPY 193 billion.

Compared with Hikari Tsushin’s total market cap of JPY 1.8 trillion, you can therefore see the stock as trading at an adjusted P/E of 9x.

That said, I wonder how much of a “moat” Hikari Tsushin has when it comes to its main businesses. Why don’t power companies sell electricity themselves? Or why do companies making mineral water not sell the water themselves? One Yahoo message board user commented that other companies use Hikari Tsushin to employ high-pressure sales tactics on their behalf, with the company taking the hit if there’s ever any reputational damage from these types of activities. Someone else likened the sales model to multi-level marketing schemes. I have read Cialdini’s books, so I can imagine what tactics they refer to.

So my research into Hikari Tsushin itself has made me less keen on the company itself, and more keen on its investment portfolio. If they can achieve a +17% internal rate of return over time, then we should be able to copy their approach and achieve similar — if not better — results.

3. The current portfolio

To that end, I’ve gone to great lengths trying to identify Hikari Tsushin’s current investment portfolio. Its stocks carry the following characteristics:

- Recurring revenues and consistently rising profitability

- Strong balance sheets that can endure crises

- Smaller, and sometimes illiquid companies

- Earnings yields of 15% or higher

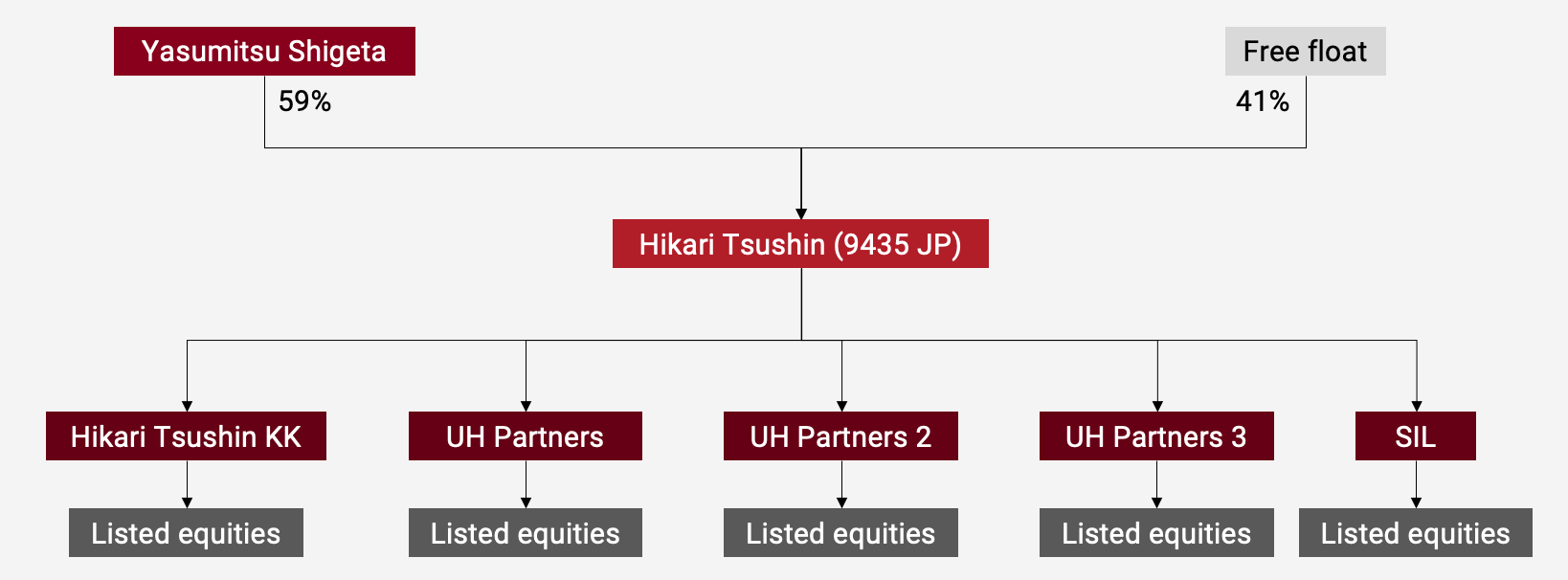

Its investment activities are mostly done through key subsidiaries “Hikari Tsushin KK” and “UH Partners 2”:

If you go through Hikari Tsushin’s investor relations materials, you won’t find the full list. But luckily, Japanese securities law requires companies accumulating 5% stakes to disclose that information within five days.

This information ends up on EDINET — the “electronic disclosures for investors network”. But to make it easier for myself, I’ve instead used the website IRBank.net to download the data for each of Hikari Tsushin’s subsidiaries. And by triangulating, I ended up with a list of 219 Japanese publicly listed stocks currently owned by Hikari Tsushin.

Other than the recurring nature of their revenues, there is no common denominator. The stocks are in industries as varied as industrials, distribution, financials, software, consumer and more. Here is the entire spreadsheet, with the stocks listed from the highest market cap to the lowest:

4. Ten Hikari stocks on my watch list

I’ve gone through the entire list over the past few days and found a few that I think warrant greater attention, ranked in order of size. Some of these market caps are tiny, but the liquidity is in most cases enough for personal accounts.

4.1. Daito Trust Construction (1878 JP)

Daito Trust Construction (1878 JP — US$7.1 billion) constructs rental properties on behalf of landlords. After the construction is over, a one-off construction fee is paid. Daito then rents the properties from landlords for ~30 years and sublets the apartments to the actual tenants. Roughly 2/3 of revenues come from rental income and the rest from new construction.

After the bubble burst in the early 1990s, the Japanese became less keen on buying properties and more interested in renting. It’s also advantageous in that in Japan, landlords are not allowed to raise rents more than inflation. But the flip side of that equation is that Daito Trust benefits from deflation and is hurt by inflation. Daito’s profits have also been hurt by the weak yen, which has raised the cost of imported materials.

Since Daito doesn’t own the land or the properties itself, it’s an asset-light business, enabling it to earn a return on capital above 20% consistently. That’s very impressive, at least in a Japanese context.

The business has recovered nicely since COVID-19, with FY2025 earnings per share finally exceeding the pre-COVID level. On trailing numbers, it now trades at a P/E of 10.8x, with a dividend yield of 4.5%.

One question mark is Japan’s inheritance tax. According to the rulebook, owners of land can reduce their inheritance tax by building apartment blocks, as they are valued lower than their actual market price. So if the owner passes away, the Daito-operated apartment blocks help landlords reduce taxes, while Daito captures some of the economics through its long-term rental contract arrangement. So far, there are no plans to change the current inheritance tax system, but if the rules are ever changed, that could pose a threat to Daito’s business.

4.2. Broadleaf (3673 JP)

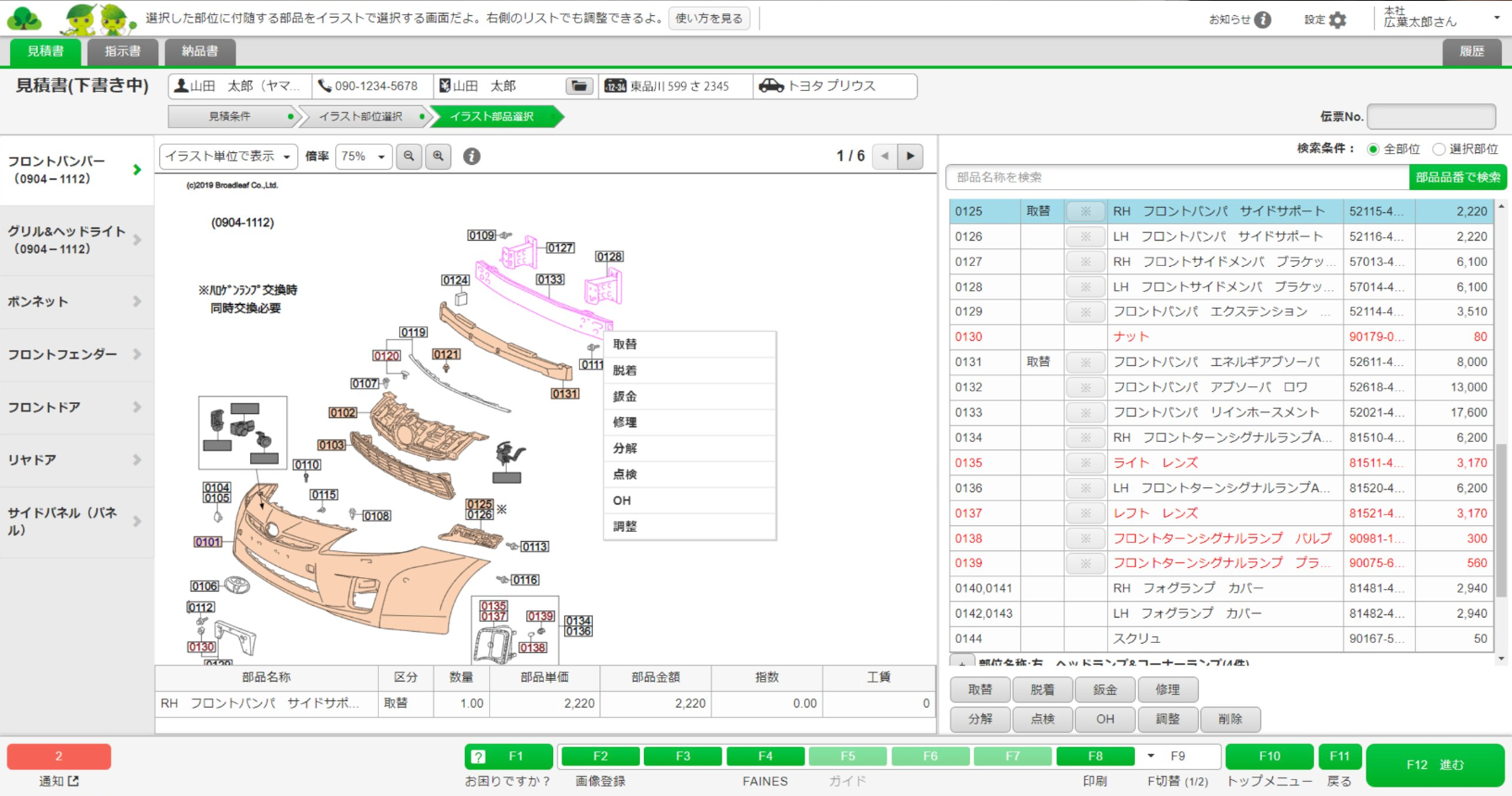

Broadleaf (3673 JP — US$438 million) is a software provider to the Japanese automotive aftermarket. In 2009, it was privatized through an MBO thanks to the support of The Carlyle Group, before being listed again in 2013.

Dealers and maintenance use the platform to trade auto parts. Broadleaf’s classification of car parts has become the industry standard. In 2022, Broadleaf stopped selling on-premise software and moved towards a SaaS model, a transition that is not yet complete.

The stock has come up gradually, yet it continues to trade at just 3.6x EV/Sales. Long-term margins are likely to end up at 30-40%. You can read Alexander Eliasson’s Twitter thread on Broadleaf here and Japan Business Insights’s 2020 Substack post here.

4.3. Fullcast (4848 JP)

Fullcast (4848 JP — US$382 million) runs a platform for short-term staffing services. Roughly 8 million workers are registered on the platform. Companies can fill a shift within a few hours. Fullcast bills the client an hourly rate and pays parts of the proceeds to the worker while keeping the rest for itself. You can think of Fullcast as an Uber for day labor. In addition, it has call-center crews that sell phone/broadband plans for telecom companies, and also rents out guards to events and public sites.

Revenues have doubled in the past seven years, meaning that the platform is growing steadily. Margins are currently about 10%, though higher in the past. The problem is that from April 2023, the government widened mandatory social-insurance coverage for short-hour workers. Costs have been rising due to a tight labor market. Competitors include Recruit’s TownWork, Pason’s JobHub and even Timee.

On the positive side, the stock trades at just 12.3x P/E, it earns a 20% return on equity, and the company is paying out 40% of earnings as dividends. The total return ratio is above 50%, with Fullcast buying back shares as recently as March 2025.

4.4. Business Brain Showa-Ota (9658 JP)

Amiral Gestion has previously owned Business Brain Showa-Ota (9658 JP — US$191 million). I’ve paid attention to it but never invested. Yet the company has continued to perform.

Business Brain Showa-Ota (“BBS”) is a consulting company helping clients with finance-related enquiries. It designs and writes code for accounting software and then installs it at the client's premises. It also has a routine business taking care of payroll, bookkeeping, HR paperwork, and IT maintenance for other Japanese companies, leading to recurring revenues. It’s been around for 50 years and trusted by governments and many of Japan’s largest corporations.

BBS has performed well over time, with EPS on a steadily rising trajectory. The stock now trades at a P/E of 11.9x with growth around 10% per year. On the look of it, it feels like it’s on a safe trajectory to higher earnings.

4.5. Temairazu (2477 JP)

Temairazu (2477 JP — US$132 million) is a software suite used by hotels to manage customer bookings. Hotels pay a fixed monthly fee to use the service, as well as on a per-reservation basis.

The benefit of the service is that the inventory can be managed across several booking sites, without any risk of overbooking. And it’s a cloud service, so hotels can access the data on any device at any time. It also owns an e-commerce price comparison site called Hikaku.com.

Temairazu enjoys incredible margins of 92% (gross profit) and 60% (operating profit). Hence, a 5.1x EV/Sales means that the stock now trades below 10x EV/EBIT. In early 2025, the company announced a 4% share buyback program, and it has since completed most of the buyback. You can find a recent write-up on Temairazu on the Value Investors Club here.

4.6. Auto Server (5589 JP)

Auto Server (5589 JP — US$117 million) owns ASNET, a used car distribution network. Dealers join the network to list or bid on cars, and Auto Server collects a fee every time a vehicle changes hands.

Auto Server’s system bids at 140 physical auctions, settles the payment and does the paperwork without taking on any inventory. ASNET also collects money when a dealer posts a new car to the platform, or when another dealer decides to purchase. About 80,000 dealers are connected to the platform and trade with each other. Given that Auto Server doesn’t hold any inventory, it’s been able to earn a 20% return on equity.

The stock now trades at 12.0x P/E and a 2.7% dividend yield. The payout ratio is meager at just 30%, and it’s also invested in a fancy new headquarters in Toyohashi. But I still think the valuation is on the low side, given the platform nature of its business.

4.7. Heian Ceremony Service (2344 JP)

Heian Ceremony (2344 JP — US$74 million) provides funeral services. It has 62 halls in Kanagawa and Shizuoka that are used for ceremonies. Heian charges one-off fees for each funeral, as well as membership dues for the prepaid plan.

In addition, Heian has a nursing care business, which offers home visits to senior citizens. Finally, Heian helps organize weddings with two chapels and costume rental services.

But the vast majority of profits come from the funeral hall business. While only a portion of the revenues are recurring, Japan’s death rate is rising steadily as the country continues to age.

While growth has been low, the stock now trades at 7.9x P/E and 0.5x book. Earnings have come back strongly since the depths of the COVID-19 pandemic, yet the stock has languished.

In May 2025, Heian started another share buyback program in modest amounts. I’m hoping that it will soon find religion when it comes to capital allocation and re-rate to a higher multiple.

4.8. Property Data Bank (4389 JP)

Hikari Tsushin just increased its stake in Property Data Bank (4389 JP — US$64 million) to 12.8%.

The company provides a niche service: an enterprise resource planning system for property management services. Customers can log into an online dashboard for tracking leases, rents, maintenance jobs, energy bills, documents, etc, on a building-to-building basis.

50% of Japan’s publicly listed REITs are customers. And several large corporations are using their service, including 70% of Japan’s top 15 railroad networks. Property Data Bank’s revenues are recurring, with a monthly fee per building.

According to Made in Japan, who wrote about Property Data Bank in 2024, Property Data Bank’s guidance came down recently due to large customization orders. But the revenue recognition was simply delayed, meaning that revenue growth is likely to accelerate from this year onwards.

The stock is cheap at only 17.0x P/E. The founder, Sadahisa Takeno, is still involved, so that’s a big plus. The medium-term margin target is 22%. You can read more about Property Data Bank at Made in Japan’s post here ($).

4.9. TVE (6466 JP)

TVE (6466 JP — US$34 million) makes valves for nuclear power plants. 60% of revenues come from the replacement and maintenance of existing facilities, many of which have been restarted after the Fukushima disaster.

TVE’s biggest competitor is Okano Valve Manufacturing, which is also benefitting from the ongoing restart process. But TVE is stronger in pressurized water reactors, used in plants that will restart faster than the rest. TVE’s valves are also used for thermal power plants, some overseas.

The stock trades at 13.8x P/E, but earnings are lumpy. Also, TVE has net cash roughly equal to the current market cap. It’s currently reducing cross-shareholdings, which in theory should be positive for its governance. Andy from The Magic Bakery Substack thinks TVE might be the target of a takeover by shareholder Seika at some point, given that it launched a nuclear power business in 2023. Read more at the Magic Bakery Substack here.

4.10. Porters (5126 JP)

Porters (5126 JP — US$21 million) is a company selling workflow software for staffing and recruitment firms. Clients use the system to keep track of recruits and clients. Each client pays about US$800 per year, and 95% of revenues are recurring based on the number of IDs. Porters has an AI search module, which should help identify the right fit for any job. In addition, there are one-off project fees for data migration, API integrations, etc. The software has excellent reviews from clients and seems to dominate the industry.

The company is tiny, but trades at 1.3x EV/Sales, and 13.1x P/E. Porters’ top-line growth was 21% in 2024, but margins have compressed. Hikari Tsushin showed up as a 5.0% shareholder in early 2025, and the stake has been increased to at least 6%. You can find a great write-up on the stock at The Magic Bakery Substack here.

5. Conclusion

I strongly urge you to take the spreadsheet of Hikari Tsushin’s portfolio of publicly listed stocks. They know how to pick stocks, so why not piggyback on their efforts?

We all have different investing styles, portfolio constraints and risk appetites. I think that Heian Ceremony could be undervalued, at least if Hikari Tsushin inspires it to finally increase its shareholder returns.

Thanks for reading,

Michael

Further material:

- Longriver’s 3Q2024 letter, which discusses Hikari Tsushin at length

- Jake Barfield’s interview with Hideaki Wada, the CEO of Hikari Tsushin

- Made in Japan’s two-part introduction to Hikari Tsushin: Part 1 & Part 2 ($)