Borrowing ideas from funds, part 2

Disclaimer: Asian Century Stocks uses information sources believed to be reliable, but their accuracy cannot be guaranteed. The information contained in this publication is not intended to constitute individual investment advice and is not designed to meet your personal financial situation. The opinions expressed in such publications are those of the publisher and are subject to change without notice. You are advised to discuss your investment options with your financial advisers. Consult your financial adviser to understand whether any investment is suitable for your specific needs. I may from time to time have positions in the securities covered in the articles on this website. This is disclosure and not a recommendation to buy or sell.

Here’s another edition of my review of the key holdings of Asia-focused funds.

I will release new editions as I find more high-quality funds to track.

Executive summary

- Digital Garage looks attractive, given its significant stake in leading price comparison website Kakuku.com and its growing payment business.

- Japanese video game producer Nihon Falcom looks inexpensive at just 4.4x EBIT and with several tailwinds such as the Playstation 5 console cycle and a shift towards higher-margin digital games.

- Philippine gin producer Ginebra San Miguel seems undervalued at 8x P/E and 5.4x EV/EBIT.

- For those who are liquidity-constrained, Taiwanese food & beverage giant Uni-President Enterprises and China KFC franchisee Yum China stand out to me as high-quality ideas with growth-at-a-reasonable price.

AVI Japan Opportunity Trust

AVI Japan Opportunity Trust is a British activist fund focusing on smaller Japanese companies. Their latest 2021 interim report has information on their current activist campaigns and what stocks they believe in the most. Their approach seems to be to invest in companies with low EV/EBIT and then push management to adopt shareholder-friendly corporate governance practices.

AVI’s largest position Hasegawa manufactures fragrances for cosmetics and toiletries. It also produces flavourings for food and beverage products. The company’s international peers Robertet, Givaudan and IFF trade at very high multiples. Hasegawa itself trades at 19x P/E, though with the backdrop of a mid-single-digit return on equity.

The second-largest position DTS is an outsourced IT services provider, offering upgrades to corporate IT systems. It’s a beneficiary of the trend towards the digital transformation of Japanese companies. The EV/EBIT is only 8x compared to the peer group’s 14x. A buyback has now been initiated, but AVI is pushing for additional reform.

Fujitec manufacturers elevators and escalators. AVI had reached out to Fujitec’s management team to improve corporate governance standards. It seems like the story has already played out at this point, with the stock doubling and now trading at 20x P/E.

Digital Garage is another stock that has performed well. The company is involved in card payment processing, online marketing and venture investments. It’s been successful at incubating businesses. For example, it holds a stake in the online price comparison site Kakaku.com worth 63% of the market cap. A complex holding structure has led to a large discount despite a growing payments business and its stake in Kakaku.com. The company’s headline EV/EBIT is 13.0x.

C Uyemura is a manufacturer of chemicals used in electronic devices. AVI has been pushing for reforms for a while, and over the past year, the company has finally announced stock-based compensation for the board, a stock split and a new buyback program. The stock is still trading at just 6.4x EBIT, meaning there is still further upside. The company is now a candidate for promotion to the Tokyo Stock Exchange’s Prime Section - a positive sign given the requirements for qualifying for it.

Number 13 on the list, the Bank of Kyoto, happens to be one of AVI’s major activist campaigns and a stock I wrote an article about here. The bank is a major shareholder of Nintendo, Nidec and several other high-quality Japanese companies. That portfolio of stock is worth around JPY 1 trillion in current market prices. If the company were to sell the portfolio of stocks and after 30% corporate tax on the gains, the company could in theory pay out a JPY 700 billion special dividend - roughly twice the current market cap and still maintain its current capital adequacy ratio. The only question is whether AVI will succeed in convincing management in doing so.

Blue Tower Asset Management

Blue Tower Asset Management is a Texas-based fund investing in a concentrated portfolio of equities through the Blue Tower Global Value Strategy. They seem to be focusing on quantitative metrics with a major focus on the balance sheet. The fund has a global mandate but includes several stocks in Japan.

Fujita Engineering constructs and maintains buildings and plant facilities. Its installs and maintains air-conditioning systems, security, electricity and water supply. The stock trades at a P/E of 7x and enjoys a strong balance sheet as well.

Shinoken builds condos and apartments for clients and later becomes a property manager for those same properties, offering recurring maintenance services to them. Shinoken has grown at a rapid rate over the past decade. Today, the stock trades at just 7x P/E, though in line with history An explanation could be a reliance on pro-cyclical demand for investment properties. And indeed, the company suffered greatly in the aftermath of the Great Financial Crisis of 2008.

The case for Nihon Falcom was detailed in Blue Tower’s recent 3Q21 letter. In short, the company is a major Japanese producer of console games with franchises such as “Legend of Heroes” and “Ys”. It enjoys secular tailwinds thanks to the transition to higher-margin digital games. Since it largely focuses on the domestic Japanese market, it is relatively unknown compared to other Japanese game developers such has Konami and Bandai-Namco. The stock trades at 4.4x EBIT, a fraction of the peer group average.

Shinnihon is a China-based contractor for condos and civil engineering projects. The stock has a net cash position that exceeds the current market cap. However, I’m not sure if the company has additional operating liabilities that could reduce the value of this cash over time. Even if you exclude cash, the stock still only trades at P/E 5x, somewhat below the historical average of 6-7x.

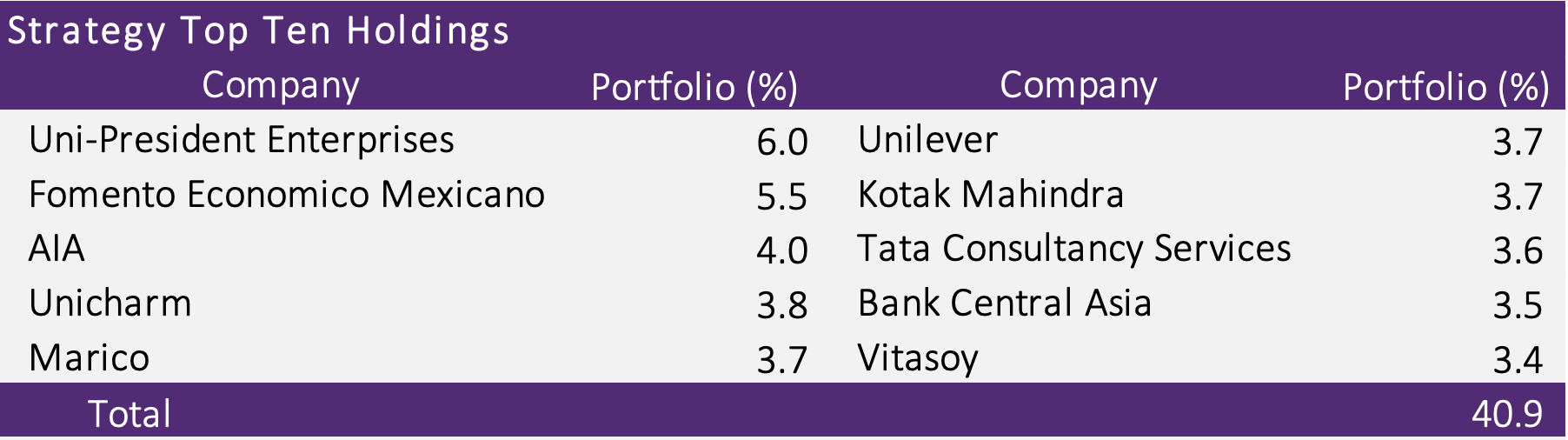

Aikya Emerging Markets Strategy

Aikya Investment Management is a specialised emerging markets fund manager headquartered in London. The team came from Stewart Investors and also has several alumni of Fidelity International.

Aikya’s largest position is Taiwanese food & beverage giant Uni-President Enterprises. The corporate structure is complex, as made evident in this Seeking Alpha post about the company. It has exposure to convenience stores via separately listed subsidiary President Chain Stores. The company also has exposure to beverages and instant noodles industries via separately listed Uni-President China. As well as several other businesses such as bottled water, securities brokerage, biotech and property development. Successful fund manager and soon-to-be-author Richard Lawrence’s Overlook Partners Fund have also maintained a very large position in Uni-President Enterprises over the past year. The stock trades at a 2022e P/E of 17x.

Hong Kong-based insurance company AIA Group is considered to be the best-run life insurance company in China. It was spun off from US insurance giant AIG in 2009. AIA has unique access to the Chinese market and continues to gain licenses in more and more regions across China while maintaining a relatively clean balance sheet. That said, the stock trades at a fairly high multiple of 19x forward 2022 earnings.

Japan’s Unicharm is another very high-quality company that’s perhaps not undervalued at a forward P/E of 33x. The company produces baby diapers and pet care products with large exposure to the Chinese market.

In India, Aikya has invested in hair products company Marico at 55x P/E, Kotak Mahindra Bank at 41x P/E and Tata Consultancy Services at 33x P/E.

Bank Central Asia is another high-quality company. It’s long been the preferred bank of Indonesian-Chinese and perceived to be better run than state-owned peer Bank Rakyat, though their returns on equity have not been all that different. The stock trades at 2022e P/E of 26x - far above the peer group.

Soy milk beverage producer Vitasoy is an interesting case. It used to be a high-flying stock but fell from grace after an employee of Vitasoy publicly supported the anti-government protests in Hong Kong. A consumer backlash on mainland China soon followed. The products are still on the shelves but out of patriotism, consumers are choosing other options. The stock is down from HK$46/share at the peak to HK$19/share today but still trades at 48x (now-40%-lower) earnings.

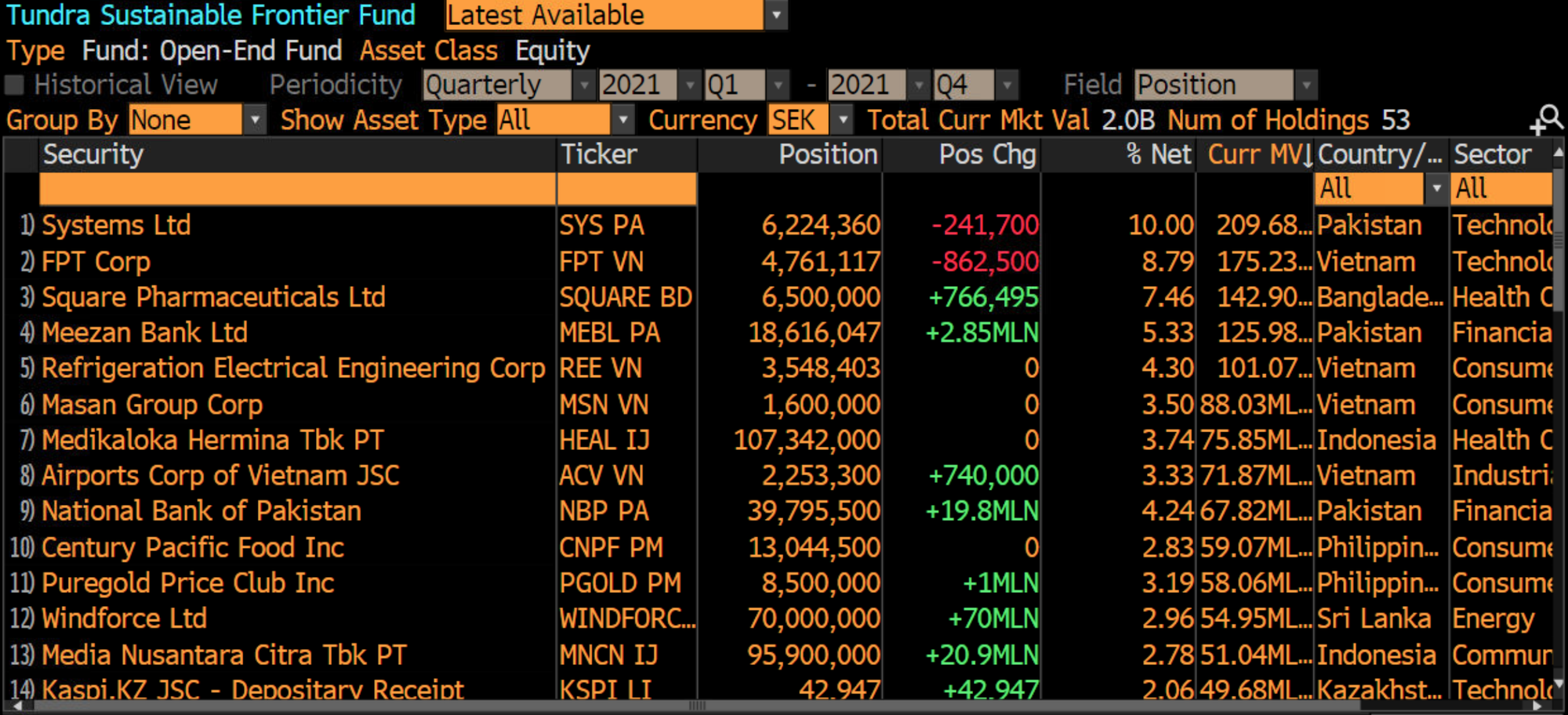

Tundra Sustainable Frontier Fund

Tundra is a Stockholm-based fund manager focusing on frontier markets such as Pakistan, Vietnam, Bangladesh and Indonesia. It has recently merged its funds into one diversified frontier fund.

Systems Ltd is a Pakistani software company focusing on enterprise support services. Key customers include financial institutions, the government and apparel companies. The stock has been growing at a 30-40% clip for many years and trades at a P/E ratio of around 21x on 2022e consensus earnings.

Vietnam’s FPT is also a tech company but more of a conglomerate. Its exposure includes software outsourcing (primarily to Japanese clients), broadband and wireless telecom services, retailing, digital content as well as education. The stock has had an incredible run but still trades at just 18x 2022e consensus.

Other stocks in the portfolio include Square Pharmaceuticals in Bangladesh at 12x P/E, Pakistani Islamic bank Meezan Bank at P/E 8x and Refrigeration Electrical Engineering, a producer of central air conditioning systems that also owns power generation and property assets and trades at 12x 2022e earnings.

Fundsmith Emerging Equities Trust

Terry Smith’s Fundsmith has become a household name among value investors, who admire Terry’s approach of buying quality stocks and holding them for the long term. The quality of the companies in his portfolio is high. But I can’t help thinking that the stocks seem overpriced - pretty much across the board.

Foshan Haitian is one of the largest producers of soy sauce in China. It has a range of other products as well such as vinegar, flavouring sauces, chicken stock and pure monosodium glutamate. It reminds me very much of Ajinomoto, but at an earlier stage of its development. While the company’s track record is impressive, a P/E ratio of 58x on 2022e consensus earnings is undoubtedly on the high side.

I mentioned the controversy about soy milk producer Vitasoy in a few paragraphs above. Still suffering from the backlash, the stock still trades at trailing 48x and 29x peak earnings.

Fundsmith’s portfolio of Indian consumer stocks such as Nestle India, Asian Paints, Hindustan Unilever, Godrej Consumer Products, Info Edge India and Marico all trade at over 50x P/E.

Philippine 7-Eleven franchisee Philippine Seven also trades at a high multiple of 48x pre-pandemic earnings. But note that its parent President Chain Stores is owned by Uni-President Enterprises, so you can get exposure to its growth through these listings as well.

Amiral Gestion Sextant Asie

Amiral Gestion is a Paris-based asset manager. They recently launched an Asia-focused strategy called Sextant Asie, which is run out of Paris and Singapore.

The largest position has Indonesian sporting goods company Map Aktif selling shoes, and apparel. The stock trades at a 2022e consensus earnings of 15x.

His second-largest position is Ginebra San Miguel, the Philippine gin producer. Thanks to its ongoing turnaround, earnings have shot up and the stock now trades at just 8x trailing earnings - despite a clean balance sheet.

The third-largest position is Business Brain Showa-Ota, which provides consulting and system development services for company financials. It trades at just 14x P/E.

Pro-Ship is a Japanese company developing software for the asset management, sales management and accounting industries. A P/E ratio of just 18x.

Last, the company has invested in Singapore-based e-commerce and game developer Sea Limited. The stock is undoubtedly high-flying and trading at 20x current-year revenue. Still, the management team is highly regarded, and the company’s Shopee e-commerce platform has been successful in almost all the markets it has entered.

Thanks for reading!

Sign up for over 20 deep-dive reports on Asian stocks per year and full disclosure of my personal portfolio.