Table of Contents

Disclaimer: Asian Century Stocks uses information sources believed to be reliable, but their accuracy cannot be guaranteed. The information contained in this publication is not intended to constitute individual investment advice and is not designed to meet your personal financial situation. The opinions expressed in such publications are those of the publisher and are subject to change without notice. You are advised to discuss your investment options with your financial advisers. Consult your financial adviser to understand whether any investment is suitable for your specific needs. I may, from time to time, have positions in the securities covered in the articles on this website. This is not a recommendation to buy or sell stocks.

Welcome, Jamie! Tell us about your background: where did you grow up and what led you to investing?

I grew up in South Auckland, New Zealand, in a semi-rural area. We had six acres with 20-odd sheep, a duck pond, and a tonne of fruit trees. It was a great place to grow up, playing rugby and cricket with my father, brothers and cousins, and (in hindsight) the constant labour required to keep the place in order helped with the work ethic for later in life.

In 2008, at the age of 25 I moved to Sydney for a job with a boutique fund manager on the buy side. I am not sure I ever really thought about how long I would be staying, but I am still here and somewhere along the way Sydney became home for me.

I first really learned about investing through reading “Rich Dad, Poor Dad”. I was lucky enough that my father handed it to me and told me to read it. Something clicked in my brain and I started looking for opportunities.

Then in my third year at Auckland University, I met another student in one of my classes who, after we got on to our common interest in investing, recommended I read Peter Lynch’s “One Up on Wall Street”. That was it – I was hooked. After that, I became addicted to reading about the stock market, financial history, and investing generally - in between reading annual reports and looking at company presentations.

After a few years in my first job in Sydney, I joined the publicly listed global equities manager, Platinum Asset Management, where I became a senior portfolio manager, running ~$1bn across a global equities long/short fund and a Japan equities long / short fund. I also headed up the global consumer, and Japan equities research teams which were responsible for generating ideas for the flagship Platinum International Fund and the other funds.

Platinum was a great learning ground, with a bunch of really smart people, and fantastic mentors. The main founder, Kerr Neilson, is a hall-of-fame fund manager in Australia and has this ability to look at a situation and see things entirely differently to how everyone else sees them.

He and co-founder Andrew Clifford came out of Bankers Trust with a great track record and seed money from George Soros, then grew the business to >$30bn AUM at one point following an incredible run post the popping of the dotcom bubble.

Andrew was the first PM to buy one of the stocks I pitched as an analyst - the theme park operator Six Flags. Thankfully he made good money on that position, as later he became CEO & CIO, and has been a big supporter of mine over time.

Another mentor of mine at Platinum, Jacob Mitchell, was key in my picking up more coverage of Japanese stocks (he managed Platinum’s Japan strategies from around 2008/9 through to his departure at the end of 2014). Jacob is also excellent at cutting through the noise and distilling issues to their essence. He went on to found the successful global equities manager Antipodes Partners, which now manages >$20bn.

Can you tell us about Senjin Capital and its strategy?

Senjin Capital was founded in 2024 by Umezaki Tsubasa and I, to focus on the amazing deep value opportunity in Japanese small caps. The deep value has existed in that space for a long time, but in recent years, thanks to the government’s corporate governance reform, it has become easier to unlock it via shareholder activism.

Before, the vast majority of these opportunities were just value traps – cheap stocks that stay cheap. Now, it is possible to effect real change in management policies around capital allocation and business execution.

When I say deep value, I am talking about stocks trading at sizable discounts to their liquid net assets and real estate, with a decent cash generative business attached that you are effectively being paid to buy at the prevailing market price. The opportunity and market transition to more shareholder-focused capitalism is similar to that experienced in markets like the US, UK, and Australia from the late 1970s, through the 1980s and beyond.

We buy substantial positions in a concentrated portfolio of these opportunities, and engage with management constructively to see that value reflected in the share prices. We do not do any public campaigns unless we have to – generally where a management team is refusing to change or grudgingly make only small / very easy changes, and other approaches to rectify this situation do not work.

We are looking for quite obvious 150%+ upside from the time we first start purchasing a stock.

Umezaki-san was most recently with Taiyo Pacific, a US Japan-focused friendly activist fund. He had a very interesting experience there, as during COVID he was seconded to one of their portfolio companies for three years, helping to drive its operational turnaround. Later, he was very involved in the execution of Taiyo’s acquisition of that company in a “white knight” transaction. He previously worked with BCG in the private equity team and KPMG in M&A advisory, so has a very well-rounded skillset.

Umezaki-san is based in Tokyo and takes the lead on our engagement efforts.

What’s the broad bull case for Japanese equities as of early 2026?

The ongoing corporate governance reform, coupled with rising interest rates has seen foreign capital flood into Japanese equities. Rising rates have caused super-depressed financial stocks, including the mega-banks to massively re-rate upwards - the banks index is up ~5x over 5 years.

The corporate governance reform has led to increased cash returns to shareholders via dividends & buybacks, and made companies much more focused on managing their capital base appropriately, including to the extent of many now pursuing business portfolio restructuring to exit subscale and loss-making or weakly profitable operations.

The broad bull case is that this continues acting as a tailwind for stocks - though I am not particularly bullish on the large cap space in general as valuations have massively re-rated. The market may have got a little ahead of itself there.

We still see plenty of opportunity amongst the small caps though, but even here the impact of greater amounts of capital being put to work is starting to become evident. Where we might have regularly been finding things with quite obvious 300% upside, that is now more like 150%-200%.

Any tips for people who want to find great ideas in Japan, where do you suggest starting? For example, if you use screens, what screens would you recommend?

It really depends on your investment style. I would not necessarily recommend buying the types of stocks we do if you do not have the capability or scale to pursue activism, unless you are willing to take a broad basket approach and rely on general improving trends in the market, bolstered by occasional & unexpected, but at a broad level inevitable, activist interventions.

This is not a bad strategy necessarily, but is not one I would recommend to anyone who does not really know the Japanese market well and understand the different activists and their approaches.

There are many different philosophies, even amongst activists who generally see things similarly. For example, some activists are happy to buy stocks where a large shareholder has control, in the hope they can badger and/or shame the shareholder into action that produces a good outcome for the stock. We prefer to have significantly more control over the ultimate outcome, so avoid such situations.

Shadow activism (ie: following activists into positions) can be very profitable if done well, but again you need to really know the activists and do your own work on the target so as not to get caught out. Some activists have famously sold their positions into the price spike caused by their substantial holder filings, causing investors who were attempting to front-run their future purposes to take big short-term losses. Other activists sell their large positions back to the companies on less than a day’s notice. Investors need to be cognisant that activists may exit at any time, and that may not be good for the individual retail investor.

I am obviously talking my own book here, but you may be better off considering an activist fund rather than trying to do it yourself.

Which sectors do you think offer the greatest opportunities at this point, and why?

We are sector agnostic, and are really looking for investments that make sense on the balance sheet alone, but where the company also owns a decent, relatively stable, cash-generative business. The opportunity we see is less in having an investment edge - we are buying obviously cheap things - but more in how we go about ensuring that shareholders actually get to see that value reflected in the share price. This will likely evolve over time, say the next several years, as the obvious balance sheet opportunities become fewer, but for now they are abundant.

That said, there are tonnes of potential opportunities out there in different areas. For example, if you can get comfortable with the AI risks, this could be a very interesting entry point for many of the SaaS and IT services stocks, based on future growth in sticky cash flows. That is not the area we are focused on though.

I know you can’t discuss individual holdings, but overall - which Japanese companies do you think stand out in terms of their strategic focus, capital allocation, etc?

It’s an interesting question, as historically very successful Japanese companies with great strategic focus often did not care almost at all about capital allocation. The market has changed a lot in that respect, but many of the great companies could do a lot better for shareholders.

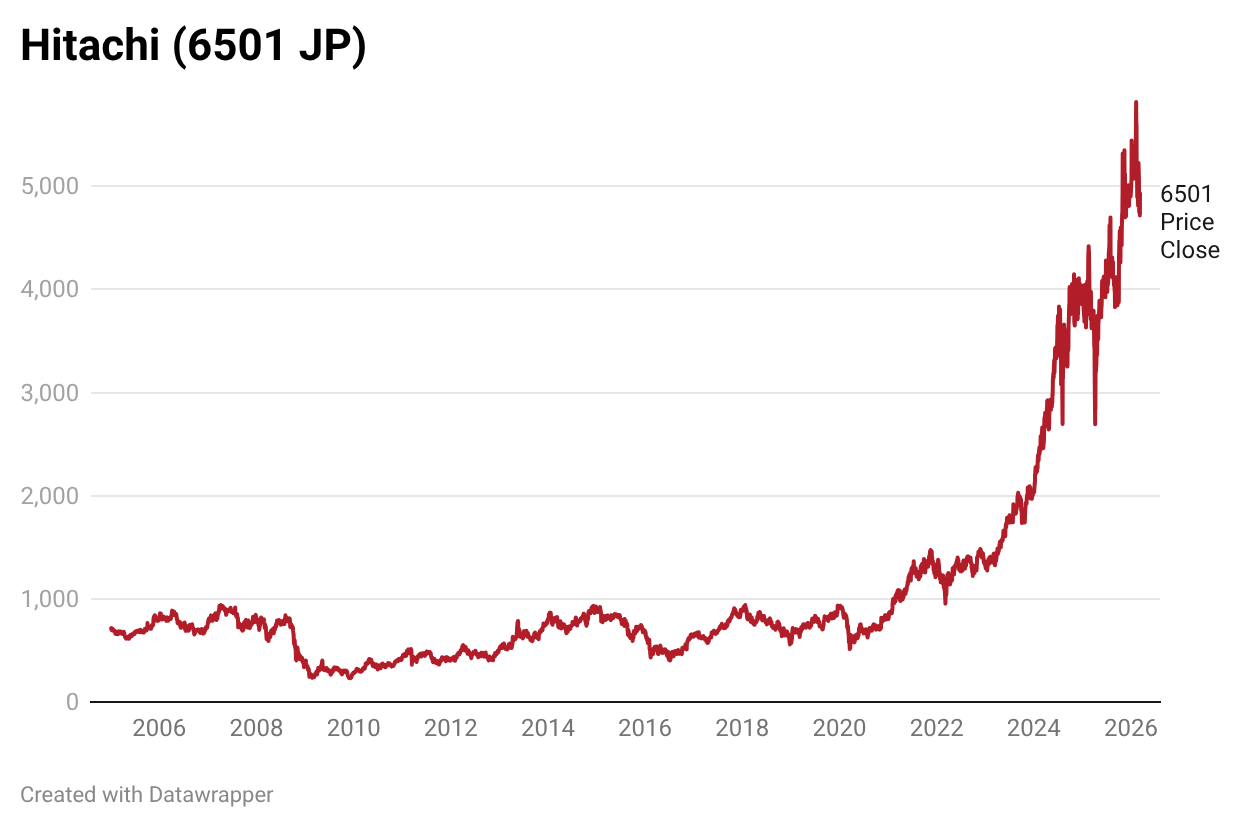

Hitachi is probably the poster-child for corporate reinvention. It had a near-death experience around 2009, and has since spent the better part of two decades selling off non-core businesses, and implementing a coherent growth strategy. The stock has performed amazingly well, and deservedly so. The interesting contrast of Hitachi’s experience to present day market conditions, is that Hitachi’s stock went almost nowhere from 2010-2016 (from memory), whereas the conglomerates who announce a restructuring plan now see their stocks rerate well ahead of delivering any tangible results.

Toyota is obviously an outstanding company that has executed well on its hybrids strategy, and in recent years has become much more shareholder friendly in returning cash via dividends and buybacks, but you only need to look at the Toyota Industries transaction to see that capital allocation decisions may not necessarily be made in the best interests of all shareholders.

Nintendo has executed very well with consolidating its gaming platforms, transitioning to digital distribution, and licensing its IP, but it is a step too far to say they have great capital allocation given their huge cash balance.

Keyence is a world leading business, but leaves a lot to be desired when it comes to returning cash to shareholders.

I like IT services firm Shift Inc’s management and roll-up / serial acquirer story.

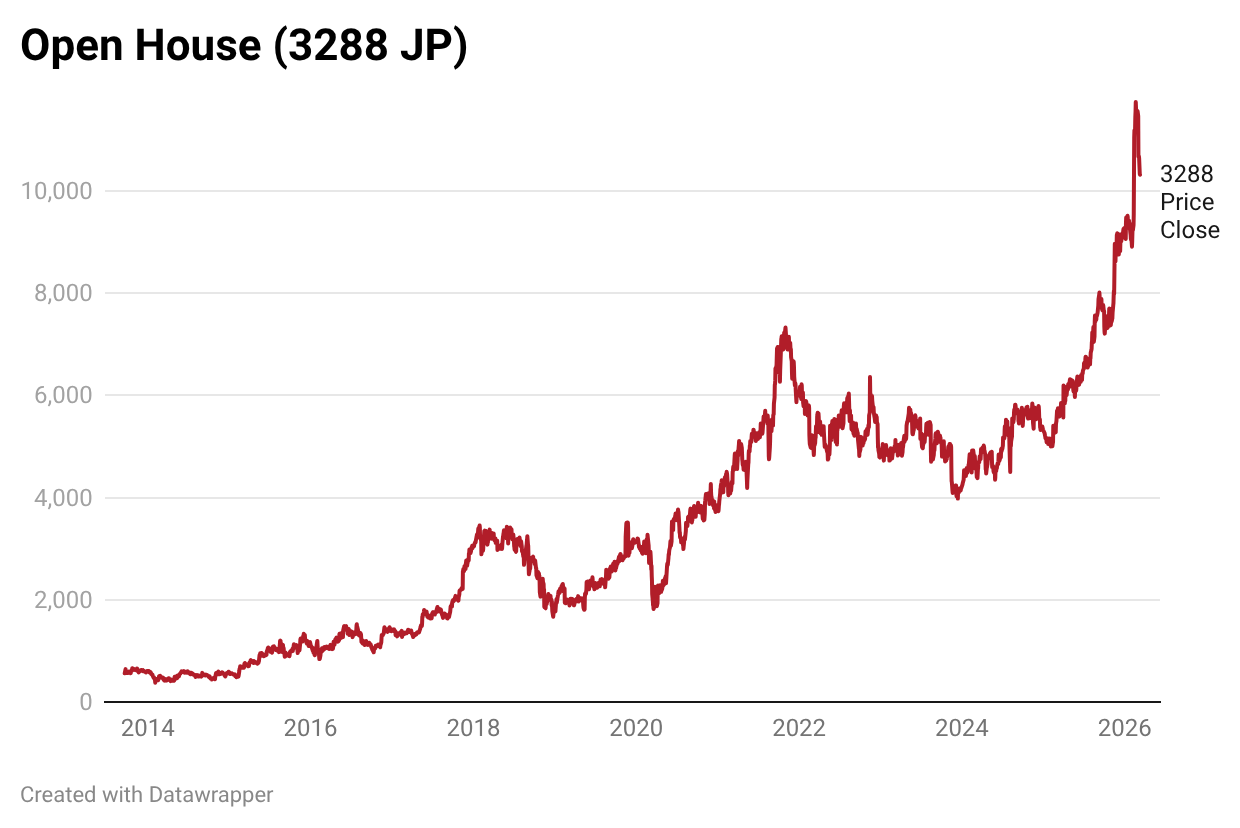

Similarly with property developer Open House Group, which has an innovative vertically integrated model and has made a bunch of sensible acquisitions.

There are not many companies in Japan that consistently execute M&A well and are rolling up their industries.

Perhaps a better question to ask in terms of prospective investment returns, is which companies have not been great, but look set to improve a lot in that respect. The ones that are already the best, are generally already well-liked by the market. Identifying these opportunities is not an area I have been focusing on for a couple of years now due to our balance-sheet driven activist approach, but is certainly something individual investors should be thinking about.

What do you think the concerns have been among investors, and why are they wrong?

There were concerns for a long time over whether the corporate governance reform is real, but I think we are past that point for most people that have spent any time looking at Japan in a meaningful way.

More recently I get more questions on the currency, inflation, and the big move in rates at the long end of the curve. We see the yen as fundamentally cheap. Japan’s reform is about improving productivity of both labour and capital, which should help boost GDP per capita and ultimately be supportive of the currency.

I think many investors also missed the less obvious plays on the Japanese semiconductor supply chain. TEL, Advantest, Lasertec, and even DISCO have been quite well-loved for some time, but it is only more recently I am seeing plenty of smaller names with dominant positions in critical inputs bandied around on FinTwit.

What shareholder activists in Japan do you admire, and what is it that they do right?

I admire a lot of the different players. There are so many distinctive approaches, people doing things slightly differently. The bigger players (EG: Effissimo, Oasis, Dalton/NAVF) have obviously had the combination of huge success + duration to get into the position they are in, so their approaches have clearly worked well.

As fund sizes get larger, activists have to deploy bigger amounts per investment, so their universe naturally shrinks and their tactics must change. Excess returns will always reduce with scale, but it is still a fertile field they are playing in, so I would not be betting against them still doing well.

There has certainly been some adaptation - for example, Effissimo, which has historically engaged behind-closed-doors, launched a hostile takeover offer for Soft99 after it announced an MBO at a low price (see my Op Ed for Nikkei Asia on this here)

Other “friendly activist” funds have adapted as well. Taiyo Pacific for example seems to be undertaking more PIPE and public-to-private transactions. Whether that is good for governance and the market overall is another question.

Can you give examples of past activist campaigns, and how you interacted with management?

I have always tried to be polite and constructive, but also to use my “gaijin pass” to clarify what is meant when management gives vague non-answers to specific questions, and to reiterate our views on things. It is generally not very well accepted when Japanese people do this because of expectations around how they should interact in a formal setting. The Murakamis may break this mould, but for most others, it is typically much more tolerable for the gaijin to ask tougher questions, than it is for a Japanese person to do the same thing.

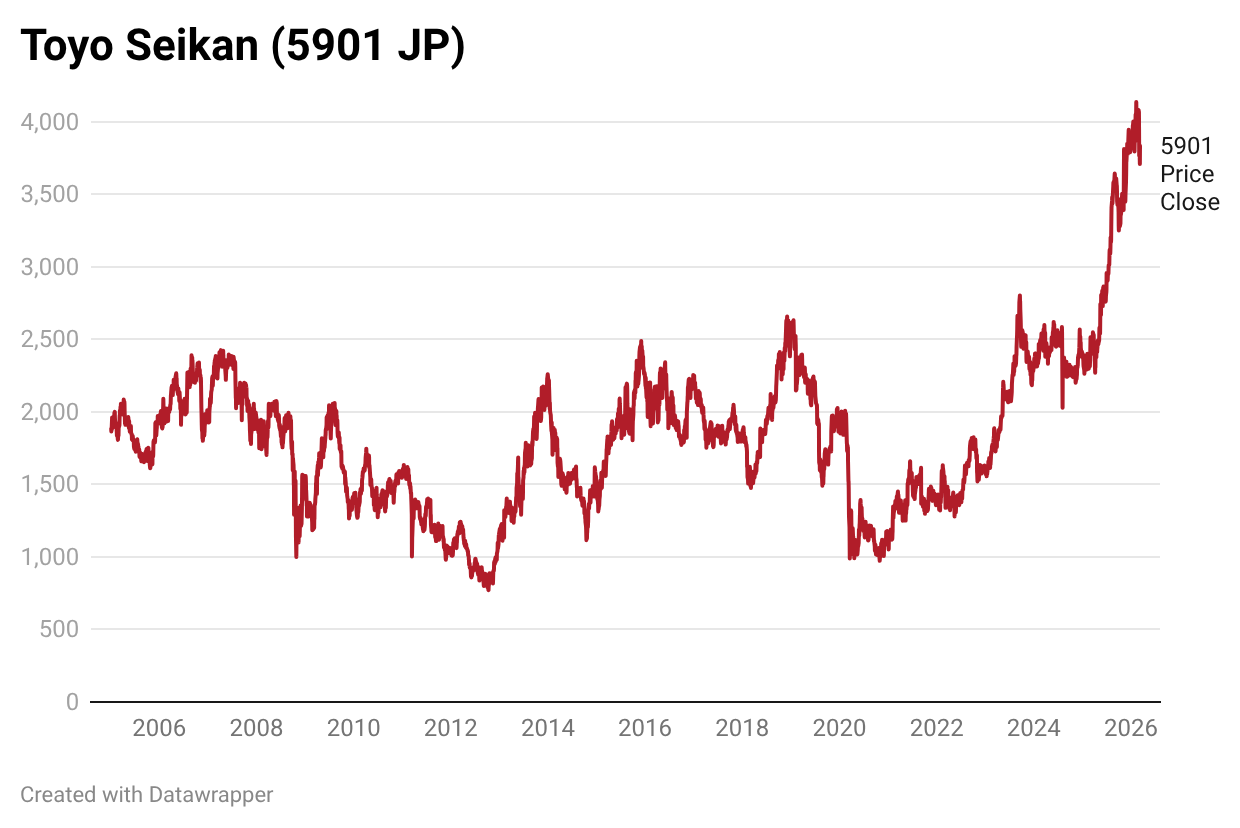

While I was at Platinum we built a large position in packaging manufacturer Toyo Seikan across the Japan strategies and International Fund, which we accumulated when the company had suffered a margin squeeze from the COVID & Ukraine war-related spikes in commodity costs, compounded by the weak yen.

The company had, in rough numbers, a $2bn market cap with almost no net-debt vs $8bn of sales, $1.4bn of investment real estate, $1bn of cross shareholdings, and $1bn of excess working capital. They had begun selling down cross shareholdings, and said they were trying to raise prices to cover the commodity costs. We engaged consistently and constructively on points around pricing, managing capacity, and capital allocation.

The company was probably hearing a similar message from Marathon Asset Management who also had a large position. They are not activists, but do engage on these issues in Japan.

We gradually saw the price increases come through, and then the company announced a dramatic reshaping of its capital policies - essentially promising to return 55% of the then market cap in cash via dividends & buybacks over the following five years, as well as increasing its profit targets, and promising a review of its real estate business. The stock has roughly tripled over five years and paid out a tonne in dividends along the way, without doing much on the top line.

Currently we have one position where we have publicly filed as substantial. We are engaging constructively with the management team via regular meetings.

Thanks for your time, Jamie! Where can people go to learn more about you and your fund?

People can visit our website www.senjincap.com and/or follow me on X.com @jamiehalse or Linkedin.

I post quite regularly on topics related to Japanese markets, the corporate governance reform, and shareholder activism.

Our fund is open to investors who qualify as “wholesale” per the Australian Corporations Act. Typically that means investors need >AU$2.5m in net assets (including primary residence) or >AU$250kpa gross income for the prior two years.

{kind=link}