Table of Contents

Disclaimer: This article constitutes the author’s personal views and is for entertainment and educational purposes only. It is not to be construed as financial advice in any shape or form. Please do your own research and seek your own advice from a qualified financial advisor. From time to time, the author might hold positions in the stocks mentioned below consistent with the views and opinions expressed in this article. This is a disclosure, not a recommendation to buy or sell stocks.

In Bloomberg's recent profile of Brevan Howard's Minal Bathwal, it was argued that part of his success stemmed from studying Nobel Prize winner Daniel Kahneman's book Thinking, Fast and Slow.

Over the past two weeks, I read the book to see what I could learn from it. And think about what the book might teach me about how to invest.

According to the old view of the human brain, we're for the most part rational. But in some cases, emotions lead us astray, making our decisions sub-optimal.

Daniel Kahneman's work challenged this view. He spent decades together with fellow Israeli psychologist Amos Tversky to understand the human mind. Are we really as rational as we think? Are there perhaps patterns in the biases and the mistakes that we fall prey to?

Their answer was unequivocally "yes". We make the same mistakes over and over, simply because of the way that our brains are wired.

In the book, Kahneman argues that the brain employs two types of thinking:

- There's an automatic, subconscious part of the brain that works through associations. It operates quickly, effortlessly, and without voluntary control. This is the realm of intuition, or in Kahneman's terminology, "System 1".

- Then there's the logical brain, which can perform complex computations, requiring attention and effort. He called this part of the brain "System 2". It's activated whenever an event surprises us, and the subconscious brain is unable to cope.

According to Kahneman, people spend 95% of their waking hours using System 1, our subconscious. Since it relies on associations and heuristics, we often end up making decisions that are inconsistent at best. Or illogical at worst.

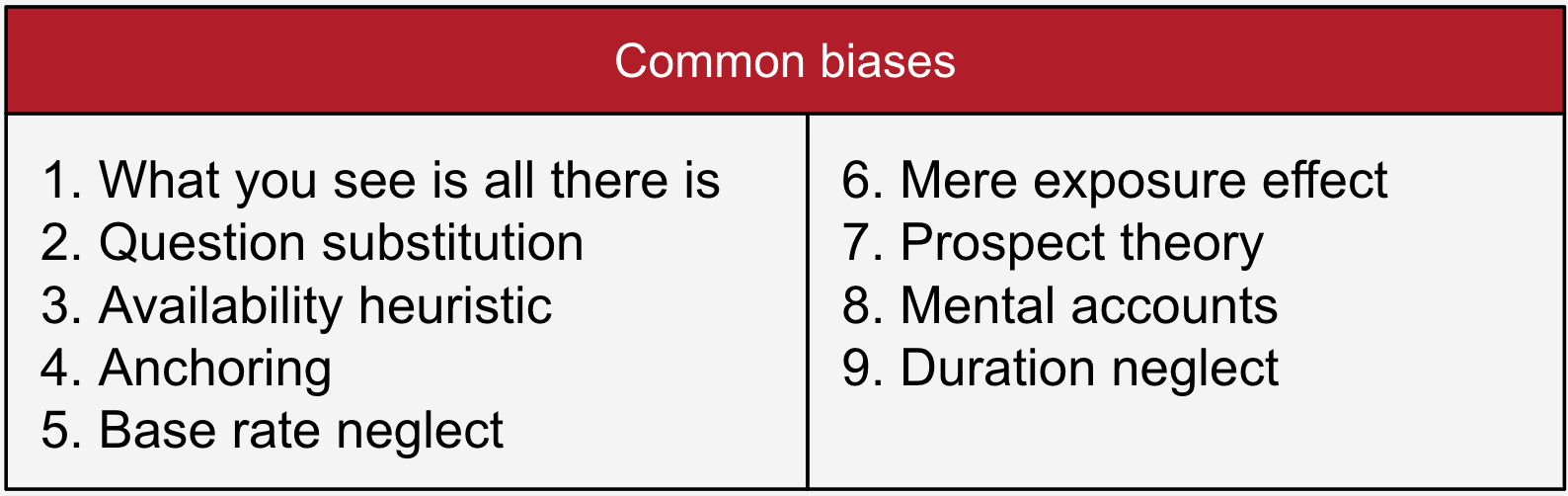

In the book, Kahneman lists a set of biases that we tend to fall prey to:

One of Kahneman's most important ideas is that our minds try to build coherent stories from information that's available to us. They often fail to allow for the possibility that information is missing. Kahneman calls this tendency What You See Is All There Is (WYSIATI). In other words, we assume that what we can see is all that's needed to make a decision. And that can lead us astray, unless we dig deeper.

Our brains are lazy. Faced with a hard question, we'll often try to substitute the question with an easier one. For example, retail investors want to find out whether a stock is worth buying. But instead of thinking about whether the stock is worth it, they'll often default to simpler questions, like whether they like the product (e.g., Tesla) or whether they believe in the CEO (e.g., Elon Musk).

A related bias is what he calls the availability heuristic. We often have trouble estimating frequencies because we simply do not have the information at hand. And instead, we approximate the frequency by the ease with which an instance comes to mind. The result is that the probability of frightening events is often overestimated.

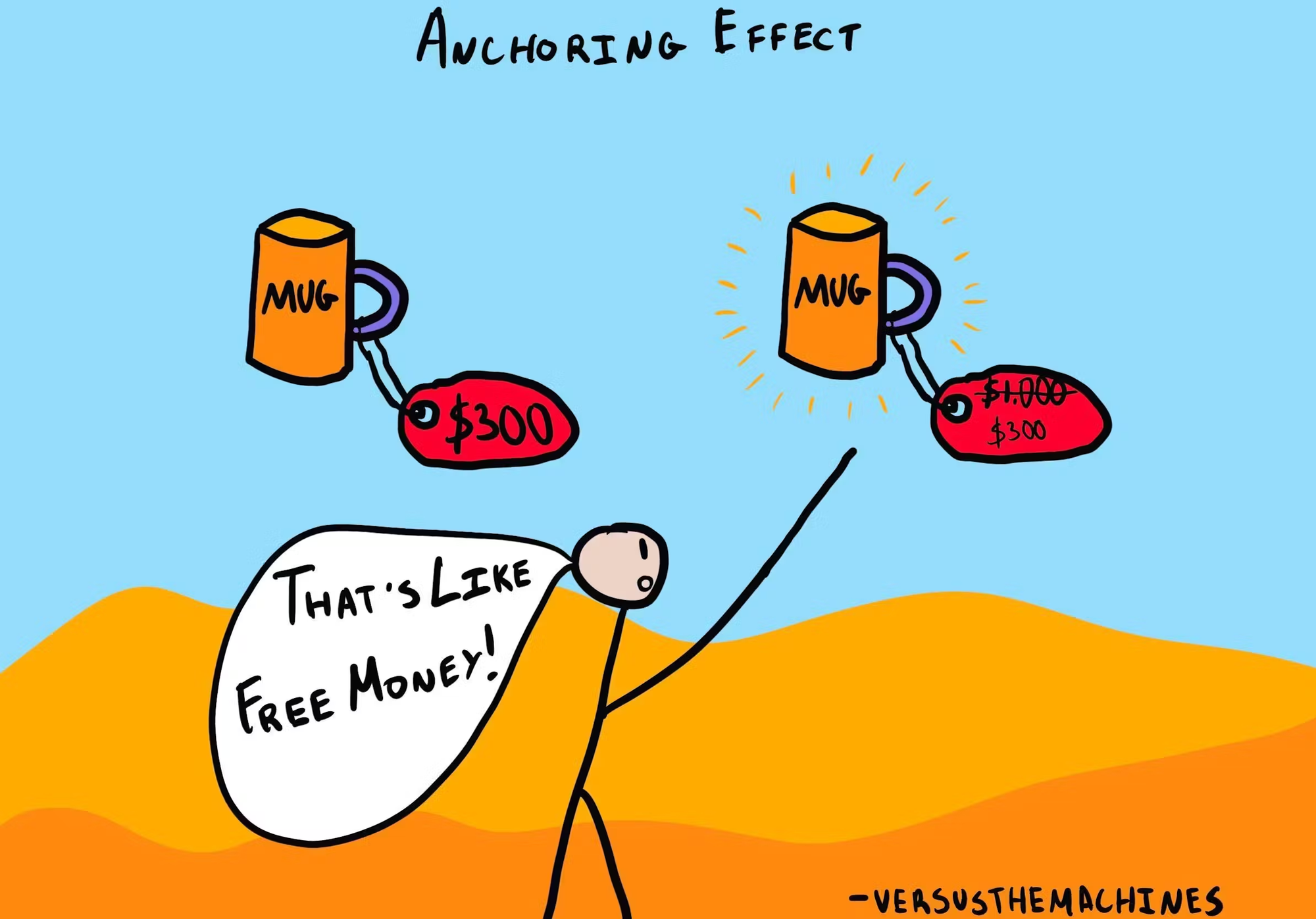

People tend to anchor to reference points. Merely showing a number can skew subsequent judgments, even if the number is completely unrelated. For example, analyst estimates tend to be adjusted very slowly to new information. That could be why we continue to see near-term momentum in individual stocks.

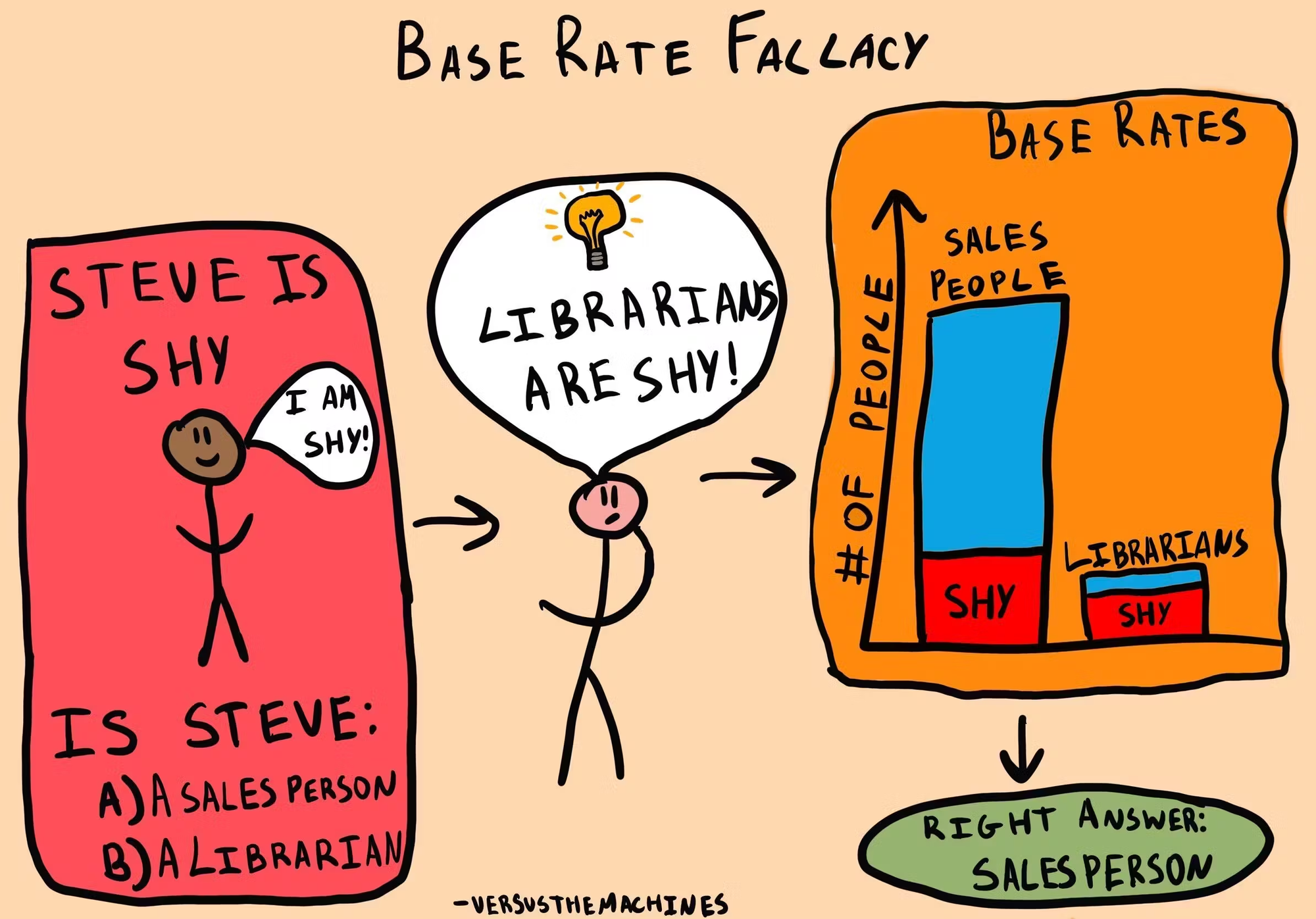

Our brains have trouble understanding statistics. That leads to base rate neglect. It means that we tend to ignore statistical background information, instead preferring causal relationships that help us generate if-then stories.

For example, if someone is tall, we like to attribute it to diet and lifestyle rather than mere chance. And we tend to underestimate the tendency for outcomes to regress to the mean. In investing, that could include a company being hurt by macro factors and extrapolating recent poor numbers into the future.

A property of our subconscious brain, System 1, is that we start by trying to understand what an idea would mean if it were true. According to Kahneman, it takes deliberate effort from System 2 to "unbelieve it". So if our cognitive load is high and we don't have the energy to question narratives floating around, we might simply accept them as true. The implication is that mere repetition can cause people to believe in outright lies. Kahneman calls this the mere exposure effect.

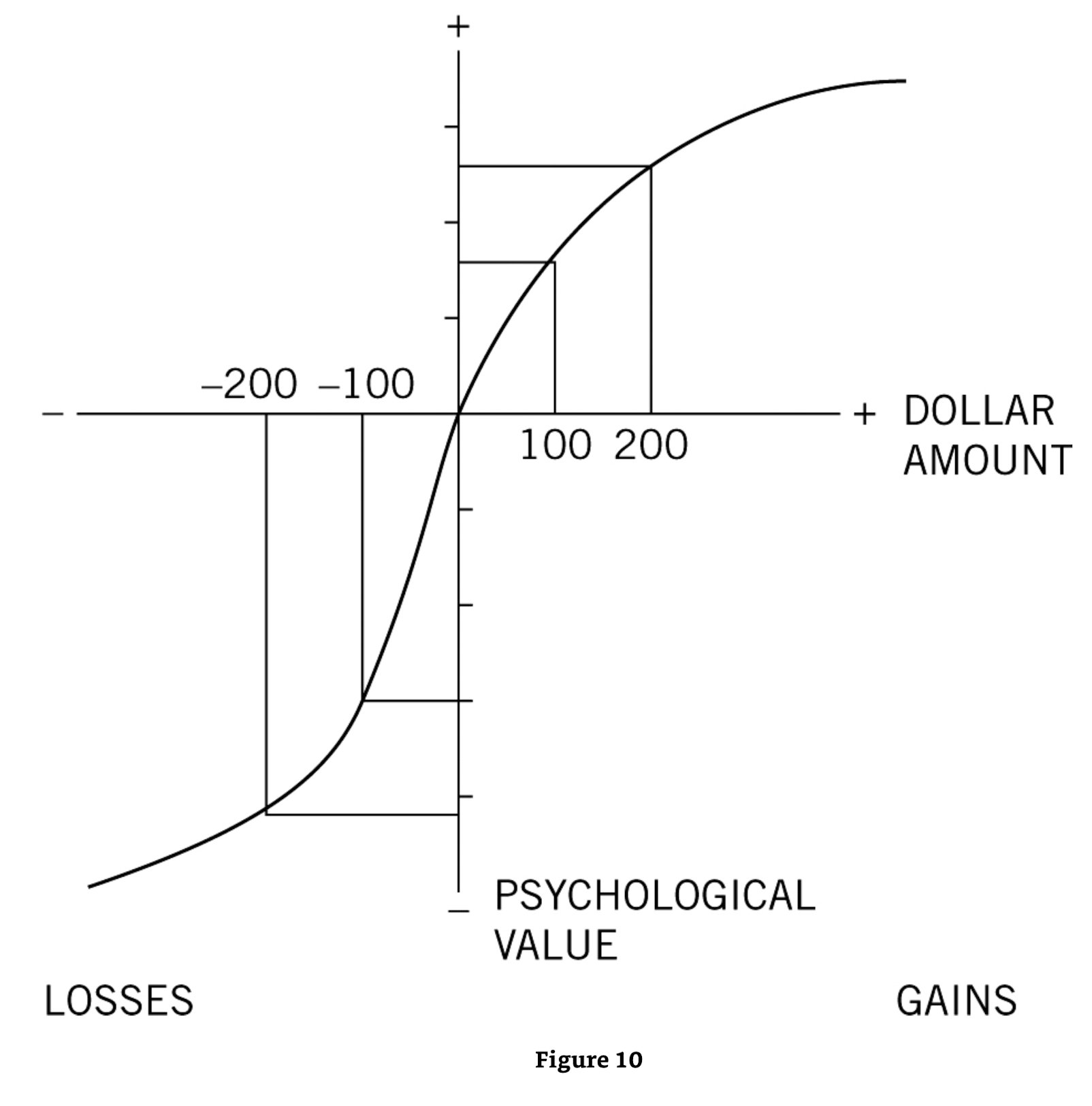

What Kahneman is perhaps most famous for is his finding that people are naturally risk-averse. His so-called Prospect Theory showed that losses hurt much more psychologically than gains: roughly 2x as much. So we tend to prefer the status quo. Here's how the psychological value tends to shift with gains or losses:

Since we tend to think in terms of gains and losses rather than wealth, specific outcomes are also divided into mental accounts. It doesn't feel the same way to play with "house money", i.e. gains. The consequence is that we tend to sell winners early to "lock in gains" in that account. And we tend to shy away from selling stocks at a loss. So we end up cutting the flowers and watering the weeds.

Finally, when we look back at an experience, we tend to forget how it actually felt to live through it. Our memories tend to be shaped by the peak intensity of the experience, rather than by its entire duration. Kahneman calls this bias duration neglect. In practical terms, that means investors might judge a stock based on its latest performance or results — ignoring its longer-term track record.

Now, the question is: how can we fight all of these biases?

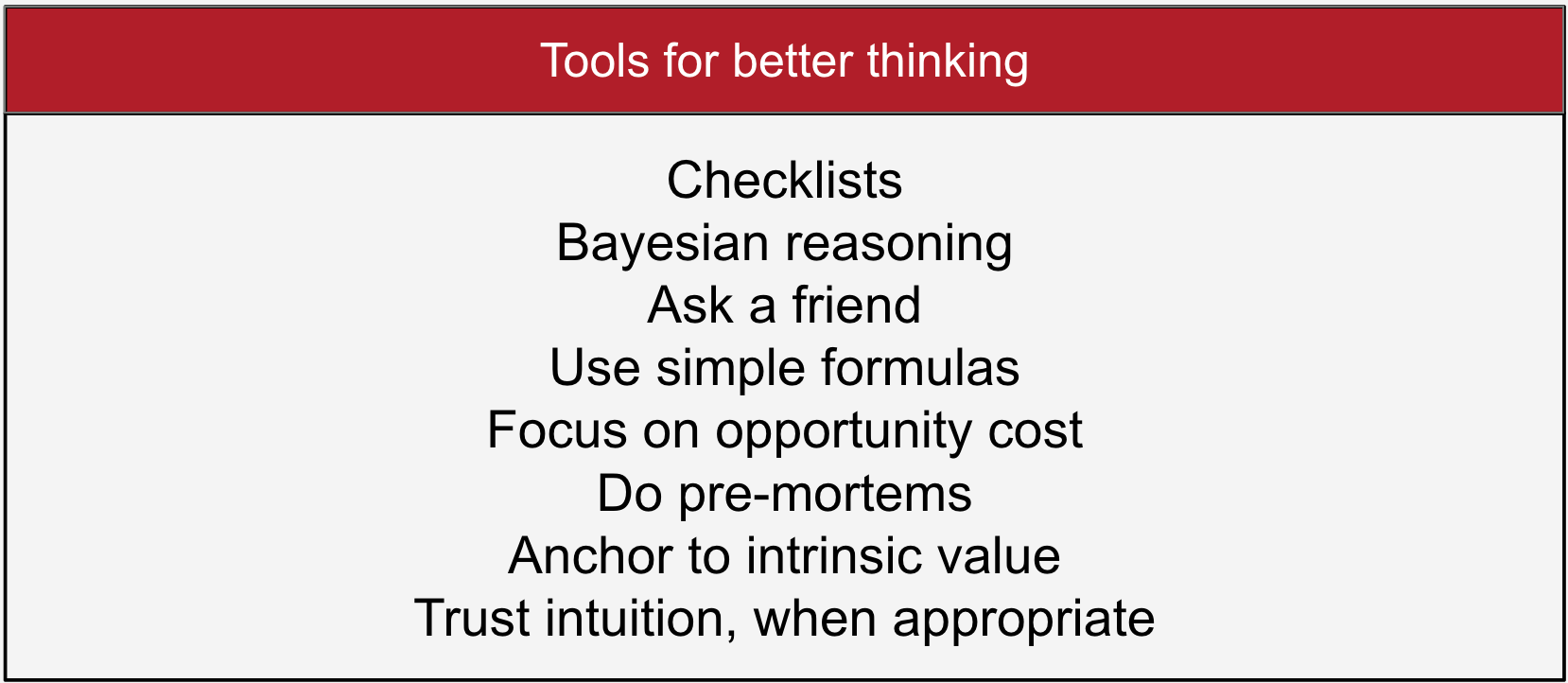

I've come up with a list of eight tools that we can use to make more rational decisions, directly inspired by the recommendations in the book:

Here's the reasoning behind them:

- Kahenman is a huge proponent of using checklists to collect relevant data. Without a checklist, we'll just try to generate a coherent story using the information provided to us. But that information may or may not be complete. That's especially true if you rely on research from an individual or an organisation that has incentives to push a biased view of reality.

- Then use the information to feed into specific formulas. Kahneman thinks that simple formulas can often outperform very sophisticated models. In investing, such formulas might include calculating prospective IRRs or comparing P/E ratios with long-term growth rates. Another formula might be selling the stock whenever something you predicted would happen didn't pan out.

- Next, we'll try to fix our base-rate neglect through so-called Bayesian reasoning. It's named after English statistician Thomas Bayes and refers to a method for estimating probabilities. The first thing you do is to calculate the base rate probability that a particular category of events will occur. Kahneman calls this the "outside view", the purely statistical view. AI chatbots might help you find the statistical information you need. Then determine your subjective probability, based on your personal impression of the case – what Kahneman calls the "inside view". Finally, move away from the base rate towards your subjective view based on your level of conviction. Examples of base rate probabilities might include how often roll-ups implode or how often low-return-on-equity companies trade above 10x P/E. Focusing on base-rate probabilities is important because regression to the mean is a force of nature.

- Once you've bought a stock, anchor to the intrinsic value. Most investors obsess about the price they paid for the stock. But the stock doesn't know you own it. If we instead focus on long-term intrinsic values, then we might avoid the instinct to sell winners prematurely or try to "get even" on loss-making trades.

- Another way to fight our loss aversion is to focus on opportunity costs. The framing will shift entirely if we compare investment opportunities rather than ask whether a single idea is good. This will put the risk-reward into perspective. Or, if you want to go to extremes, use the old Michael Steinhard method of liquidating the entire portfolio, then decide whether you want to buy back your positions. This will frame any investment as a potential gain rather than a legacy loss.

- To make sure we have all the evidence we need, Kahneman suggests doing a pre-mortem by asking yourself: "Imagine you are one year in the future. The outcome was a disaster. Take 5-10 minutes to write down exactly what went wrong." This will be a way to fight our tendency to focus on the information at hand, i.e. the bull case. Ignoring the other possible scenarios that could hurt us in the long run.

- Asking a thoughtful friend of a colleague is another way to expose our blind spots. When we evaluate our own plans and think about our own stocks, we tend to focus on the specifics of why the story will succeed. In contrast, outsiders tend to be better at thinking about base-rate probabilities. So they can help us stay grounded.

- That said, our associate System 1 – our intuition – can also be helpful at times. Kahneman thinks that our intuition works well in situations with a clear feedback loop and plenty of experience to practice. So intuition might help us in short-term trading, assessing market sentiment or judging the character of a CEO. I personally think that even long-term investors eventually develop an intuition for which business models work and which do not. So if you're an experienced investor, trust that intuition.

If there's something I want you to take away from the discussion, it's to use checklists. They will ensure that you don't miss anything major.

The second takeaway is to think about base-rate probabilities. With ChatGPT, it's easier than ever to estimate them. Growth rates, valuation multiples and investor sentiment tend to mean-revert. So you might as well keep that in mind from the very beginning.

{kind=link}