Table of Contents

Disclaimer: This article constitutes the author’s personal views and is for entertainment and educational purposes only. It is not to be construed as financial advice in any shape or form. Please do your own research and seek your own advice from a qualified financial advisor. From time to time, the author might hold positions in the stocks mentioned below consistent with the views and opinions expressed in this article. This is a disclosure, not a recommendation to buy or sell stocks.

Here's why investors should be cautious about emerging-market indices.

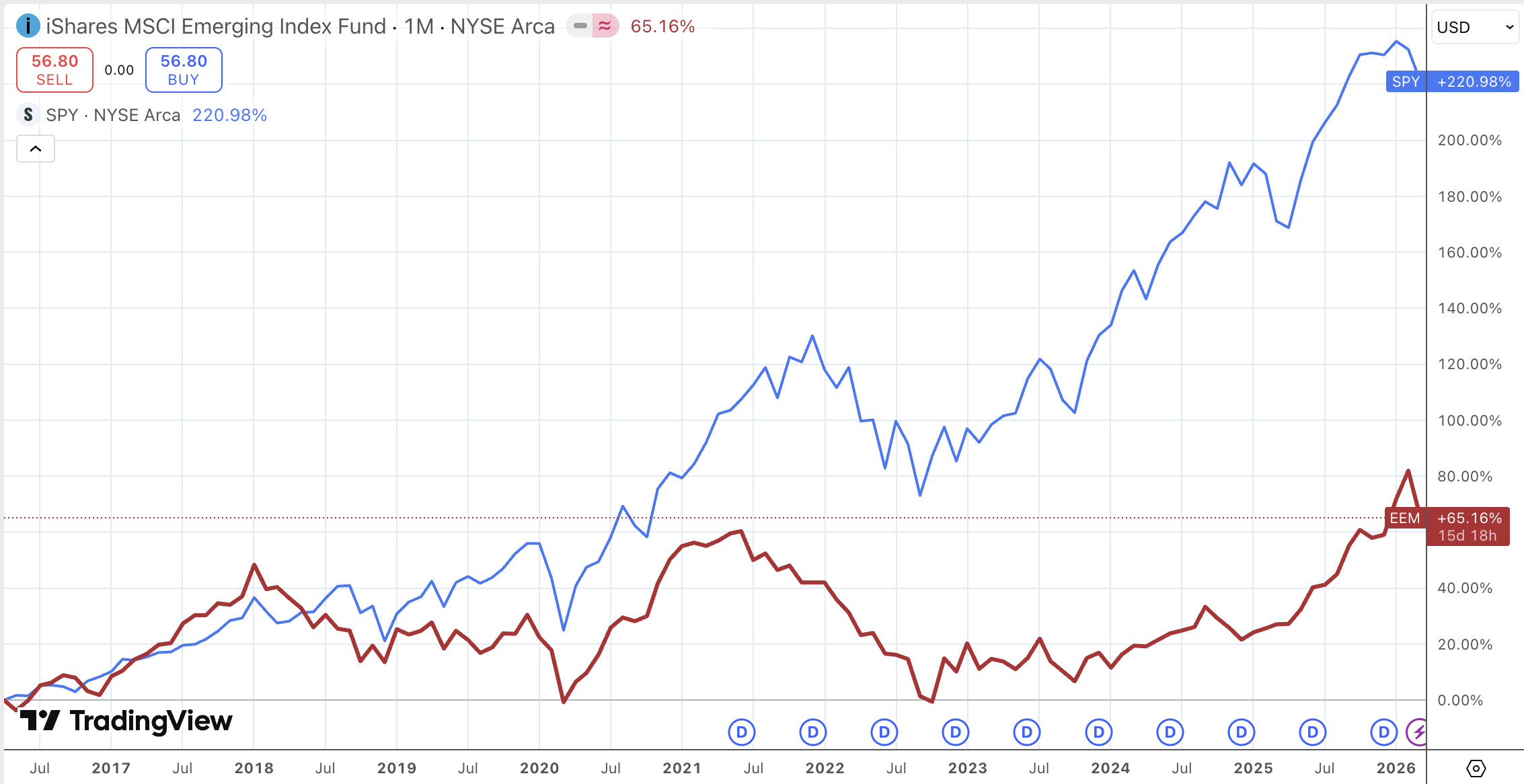

In the past ten years, MSCI Emerging Markets has seriously underperformed the S&P 500:

And this is despite the fact that MSCI Emerging Markets traded at just 11.5x P/E at the starting point – much lower than the S&P 500's 17.1x.

The primary reason, in my view, is that almost all emerging-market indices are market-cap weighted: the biggest firms get the biggest weight.

That's great for innovative countries such as the United States, where winners tend to keep on winning. But in smaller markets, it's not necessarily the case. If the index covers a cross-section of countries, some will be experiencing a boom and some a bust. But if you construct a market-weighted index across all of them, you'll end up overweighting the overvalued market and underweighting the undervalued one.

Even within specific countries, the largest companies are often state-owned enterprises or run by some tycoon with political connections, rather than an exceptional business like Apple. So if you buy a market-cap-weighted index, you'll end up allocating more capital to such businesses, rather than smaller, more dynamic private sector enterprises.

There are a few exceptions, of course. Both TSMC and Tencent are obviously very well-run businesses that also enjoy large index weights.

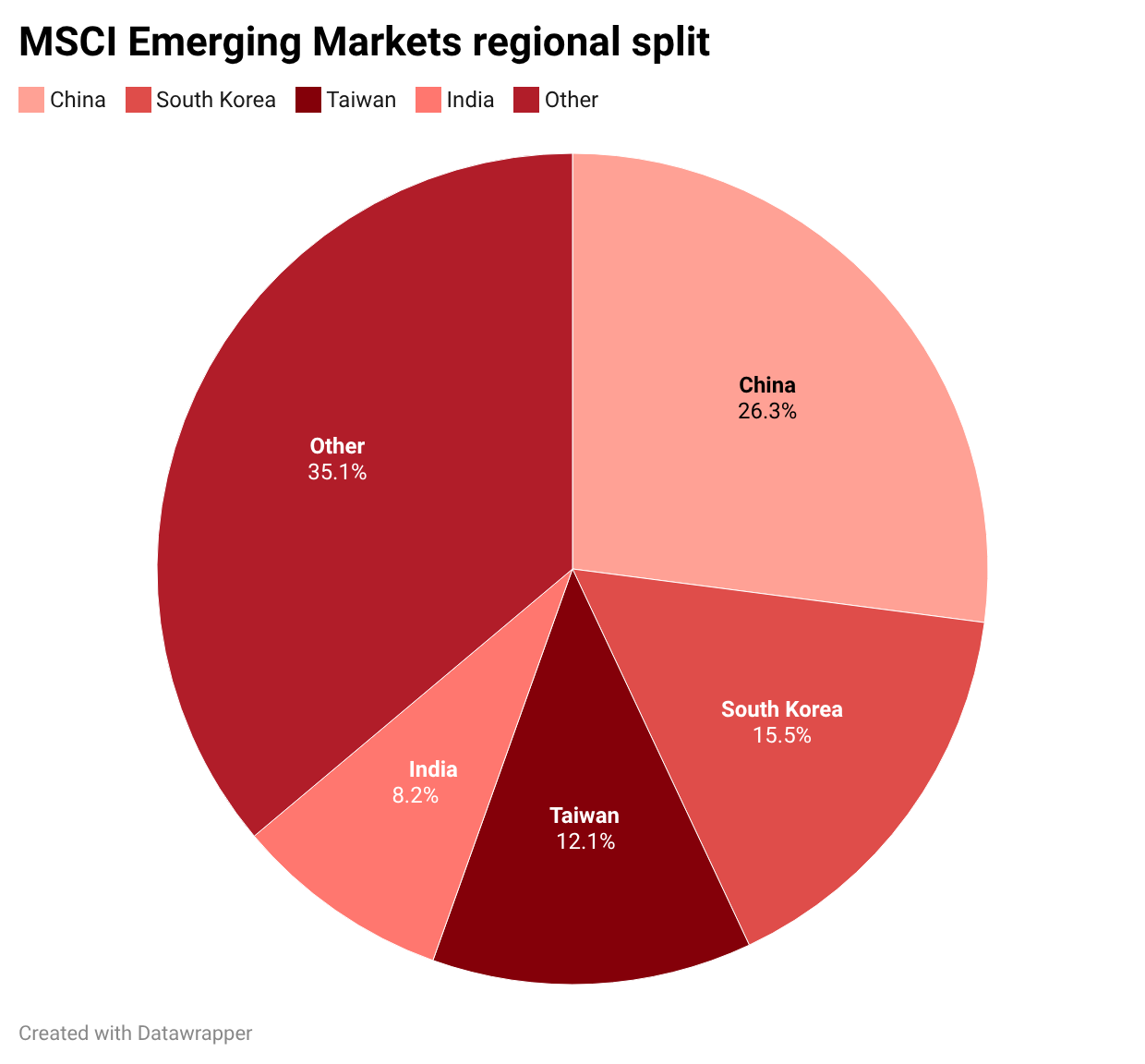

Some indices are also quite concentrated. In 2015, for example, the MSCI Emerging Markets Index had a 69% weight in Asian equities. China alone represented 26%, and South Korea and Taiwan another 27.6%.

With this type of profile, you end up with a great degree of tech exposure and a great degree of China exposure. Unfortunately for MSCI Emerging Markets investors, the Communist Party had a crackdown on its tech platforms in 2020. And with falling property prices, deflation pushed down the net interest margins of the nation's state-owned banks. More recently, the index has rallied thanks to a bull market in AI-related stocks.

The concentration problem is even worse in smaller emerging markets like Indonesia. Because the MSCI Indonesia index has a whopping 49% weight in financials:

Investors may think they're getting good exposure to the Indonesian economy. In reality, they're buying a few banks with coal exposure on the side.

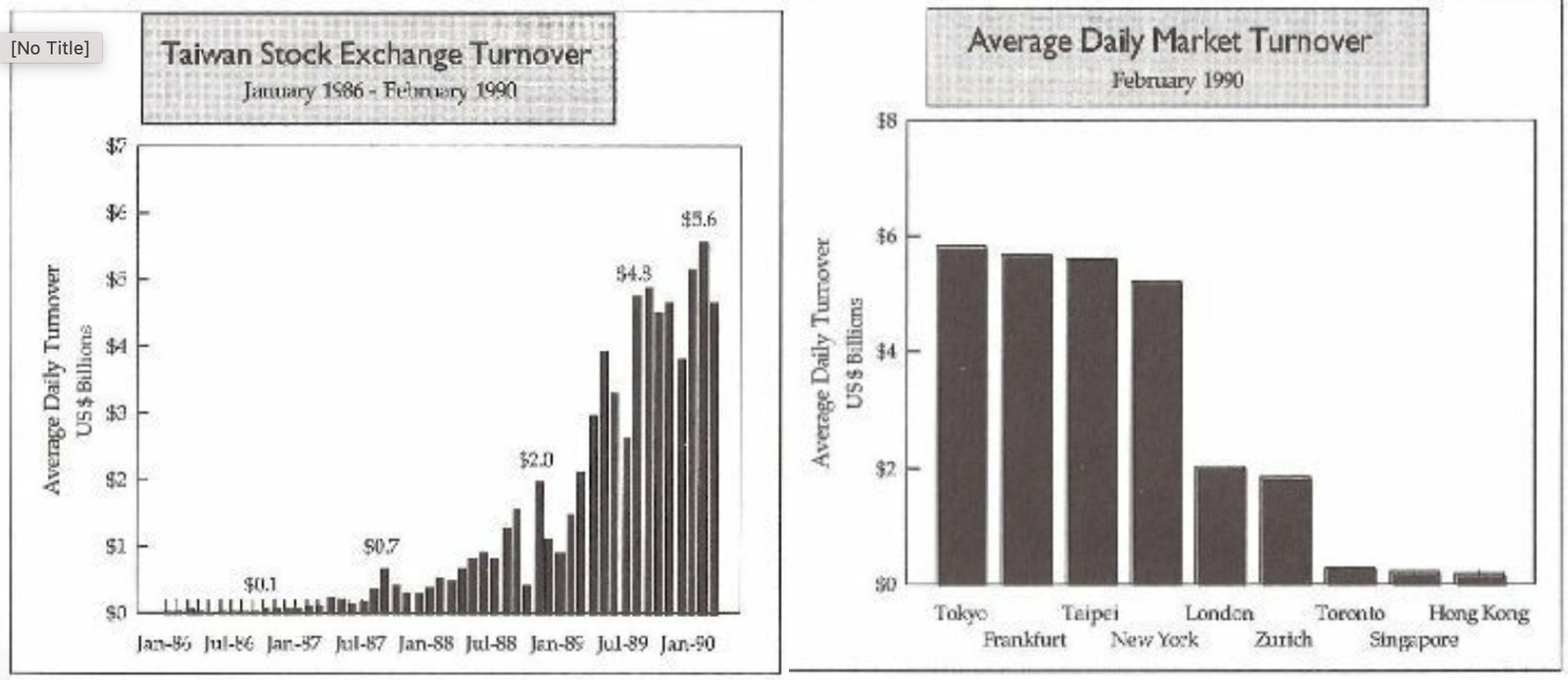

Another issue is that indices go for stocks with high liquidity. But over an emerging market cycle, trading volumes can easily go up 10x. For example, just look at this chart of trading volumes in Taiwan between 1986 and 1990:

ETFs will typically exclude stocks that are too illiquid to buy, or just buy a stock with similar risk factors. So in 1986, indices would probably have excluded Taiwan, and then been more likely to buy at the peak in 1990.

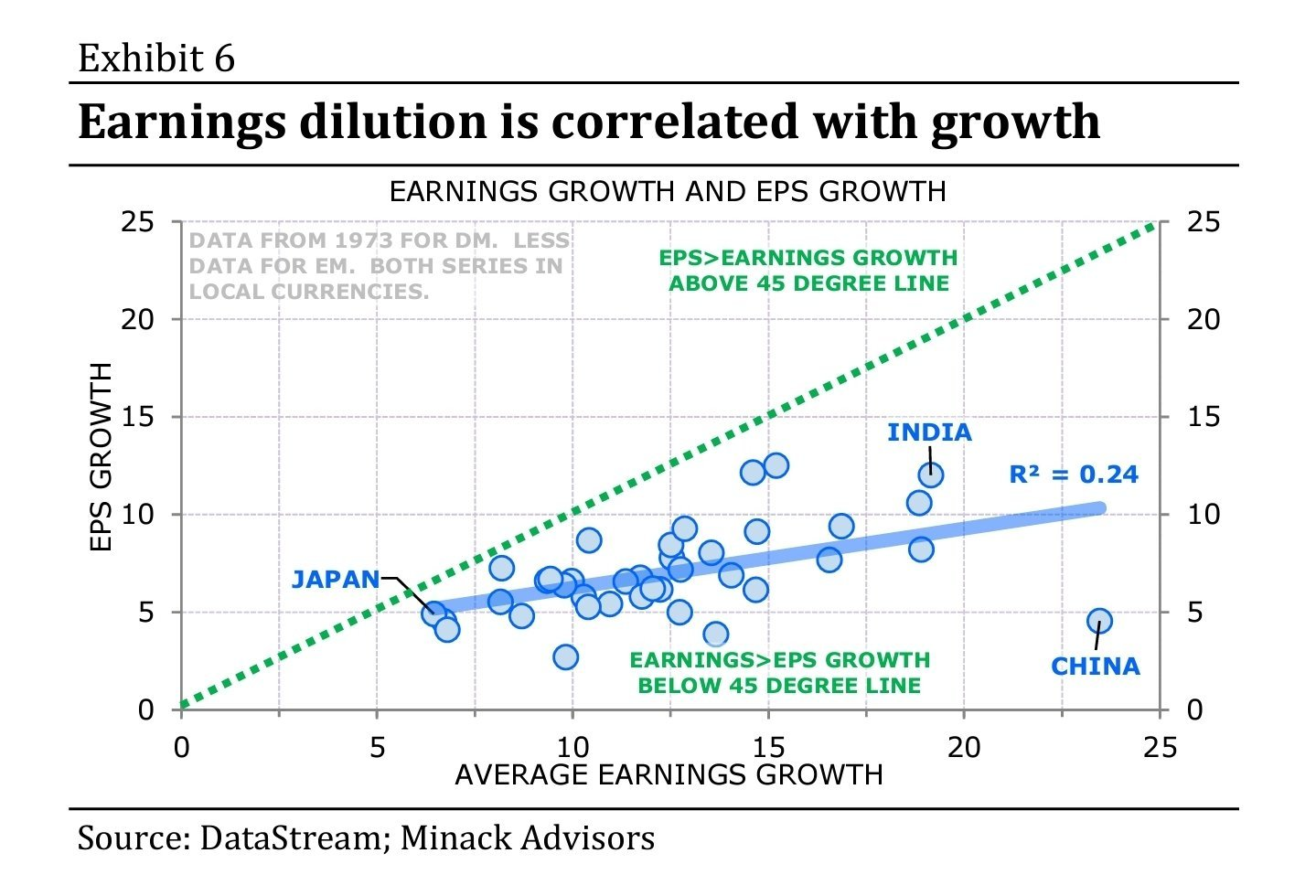

The next issue with emerging-market indices concerns share count dilution. This chart from Gerard Minack shows the issue very clearly:

Despite record-breaking earnings growth in China, the growth in earnings per share has disappointed. Why? Because the share count keeps going up.

Unlike in the United States, Asian companies tend not to buy back shares. Instead, state-owned companies and large caps tend to issue new shares. An index fund will be forced to buy the newly issued shares to maintain its weight. The implication is that becoming an index constituent almost becomes a license to print money: the index funds become permanent ATMs.

Another explanation for the poor performance in the MSCI Emerging Markets is that some of these countries have poor minority protections. Capital is accumulated on the balance sheet. Related-party transactions are then used to funnel capital out of the listed company and into the hands of insiders.

Finally, I think there might also be a problem with hedge funds front-running indices. Index inclusions and exclusions are typically announced before index funds execute their trades. This gives hedge funds an opportunity to bid up the prices of stocks added to the index before selling shares to the index funds.

The bottom line is this: emerging market companies are typically old-economy stocks whose valuations can vary a great deal through the economic cycle. Market-cap weighted indices will typically buy these stocks when they're the most liquid, i.e., at their peak. And the problem will be exacerbated by the issuance of shares by companies in markets where minority protections are weaker.

So what's the solution?

I think the solution is to pick yourself. That way, you can ensure that the corporate governance is decent, that insiders are unlikely to dilute your shareholdings, and that you're buying the shares at a reasonable price. There are high-quality stocks in every market, so by including the emerging market universe, you'll get a much greater opportunity set.

If you insist on buying index funds, you could adopt Verdad's strategy of only buying emerging markets when they're emerging from serious crises. Just be aware that country ETFs are often liquidated right at the bottom — which is exactly what happened to Global X's Nigeria fund back in 2023.

{kind=link}