Table of Contents

Disclaimer: This article constitutes the author’s personal views and is for entertainment and educational purposes only. It is not to be construed as financial advice in any shape or form. Please do your own research and seek your own advice from a qualified financial advisor. From time to time, the author might hold positions in the stocks mentioned below consistent with the views and opinions expressed in this article. This is a disclosure, not a recommendation to buy or sell stocks.

Substack writer Citrini published a controversial post arguing that AI agents will replace jobs and lead to mass unemployment. Here's a short rebuttal to that article, together with a discussion of the opportunity set in Japan's software-as-a-service industry, as I see it today.

There's no doubt that generative AI tools can generate code quickly. But that doesn't necessarily mean that they will commoditize the entire industry.

I believe in Clayton Christensen's view that customers look for services that solve specific jobs-to-be-done. Consumers and companies have specific budgets to spend, and they'll spend them on whatever tools solve their problems with the least friction and risk.

The problem is that generative AI tools don't always have the right context. Vibe-coded software tends to be approximately right, but not perfect. So an experienced programmer will still need to check the code, meaning the productivity improvement might be on the order of 30-50% rather than 90%+.

And the roles a software company fulfils include not just programming but also:

- User experience design

- Sales & marketing

- Customer support

- Ongoing maintenance

- Dealing with cybersecurity threats

Whenever the technology advances in one area, the competitive frontier will inevitably shift to the other, such as a better user experience or improved technical support.

From what I can tell, generative AI tools excel at content creation, summarization and brainstorming. To take my own industry as an example, I highly doubt that writers will be displaced. But writers who do nothing but summarize news certainly will be. The competitive frontier within the newsletter industry will shift into areas where generative AI tools cannot compete: providing a personal voice, offering genuinely contrarian views on new topics, collecting primary-source material and discussing real-world experiences.

Citrini is wrong, longer-term. There's no need to worry about job losses in a functioning market economy, except in the short- to medium-term. There's an endless demand for services that solve our everyday problems, stimulate us, make us feel accomplished, provide guidance in our lives, or satisfy our need for community. Just because we cannot imagine the jobs of tomorrow, doesn't mean they won't exist.

I don't think vibe coded software has been revolutionary. Or at least not yet. Check out the top success stories from the vibe-coding platform Lovable. They include names like DummyForms, BoomHabits and RaiseFlow. None of them has really made a dent in the global SaaS industry. Their websites look like AI slop, and their services don't seem to be catching on.

OpenAI itself uses Slack, Salesforce, and other SaaS products to manage its business. If OpenAI itself hasn't vibe-coded alternatives to them, it seems unlikely that other customers will.

I agree that AI tools will help competitors iterate faster. Today's AI-native start-ups might be outcompeting companies born in the SaaS and on-prem eras. Therefore, I will make sure that whichever company I invest in 1) has young engineers who know how to use AI tools to solve customer problems, and 2) enjoys significant economic moats that protect it from competition.

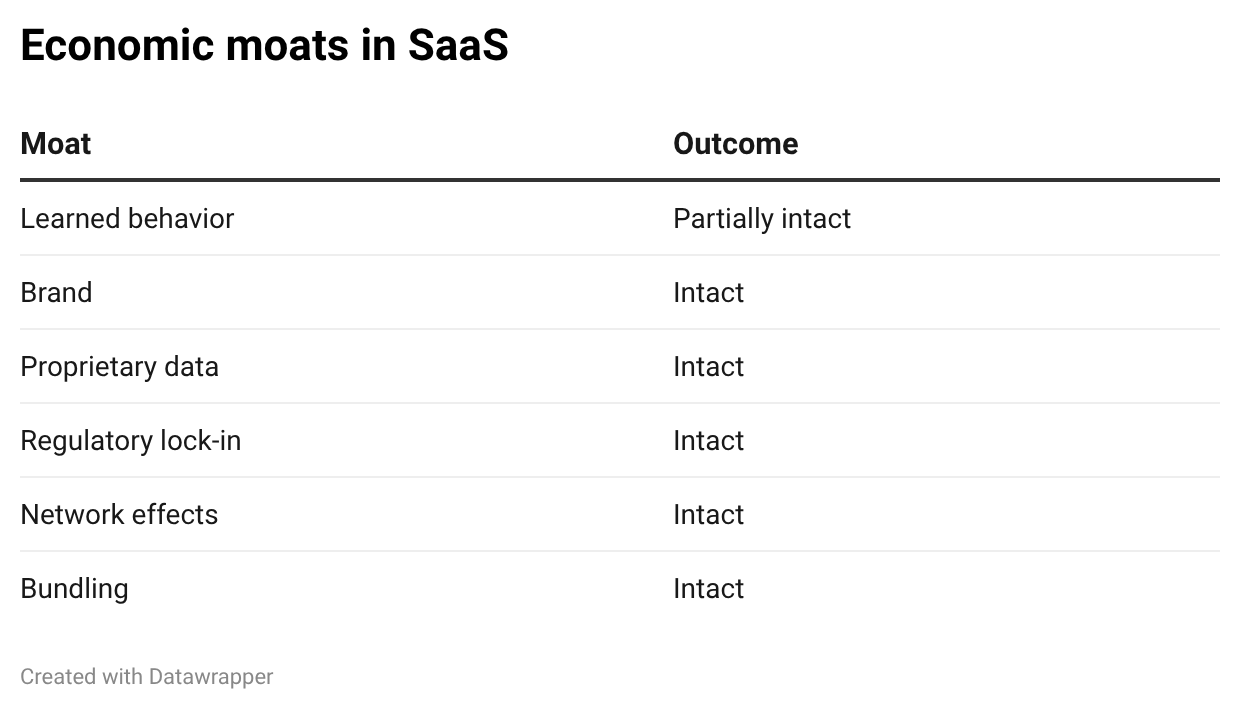

There's a strong case to be made that most of the typical software "moats" remain mostly intact:

For example:

- Why do we keep using Google for search? It has become an ingrained habit after years of using it with favorable results. Getting people to adopt a new habit takes time. I do think that behavior can and will change if a better solution shows up, such as ChatGPT, Claude, or Gemini. So the benefits from learned behavior can diminish if users suddenly prefer to solve their jobs-to-be-done through AI tools.

- A key reason why people buy brand-name products is to reduce their purchase risk. People have learnt that buying Apple products tends to be the safer choice. So finding companies that maintain high quality, whatever the product, is crucial. We're not yet at a point where prompting Claude to generate an app will guarantee that it works under all circumstances. Slight inconsistencies can quickly damage a brand. So if you're at a company facing career risk if you buy the wrong product, you'll most likely go with the safest option. This includes Salesforce, SAP, and other brand-name software suites.

- If the company sits on proprietary data, even better. I learnt from my discussion with Japan's Kaonavi that the employee data was almost impossible to export. Imagine the friction if a company were to try change to a vibe-coded alternative and recreate the data sitting within Kaonavi. In fact, companies sitting on proprietary data will even benefit from probabilistic computing, as they can offer customers better ways to access the data.

- Regulatory lock-in also increases the hurdles for disruption. Software needs to comply with relevant laws and sometimes seek certifications. Implementation cycles, for example, in the Japanese electronic health records industry, are incredibly long. You can't simply vibe-code your way to becoming a major software provider in Japan's electronic health records industry.

- Some companies enjoy network effects, including social media platforms and two-sided marketplaces. For example, Bloomberg's IB Chat has become the de facto communication tool for Wall Street. And since the data generated by these networks is proprietary, it provides further lock-in as the companies learn to implement AI tools on top of them.

- Finally, bundling services can create switching costs. For example, if I use Bloomberg for IB Chat, news, trade execution and portfolio management, switching to competing services will be hard. I'd have to find replacements for all these services, introducing significant friction. And if the software is bundled with hardware, the switching costs will be even greater.

So to summarize, I think that the big software moats are still intact. Companies that provide point-solution software have always been vulnerable, and they are even more so today. Just like in any other industry, I'd be more concerned about generative AI tools unlocking features that solve customer problems better or faster, for example, in the realm of content creation, summarization and brainstorming.

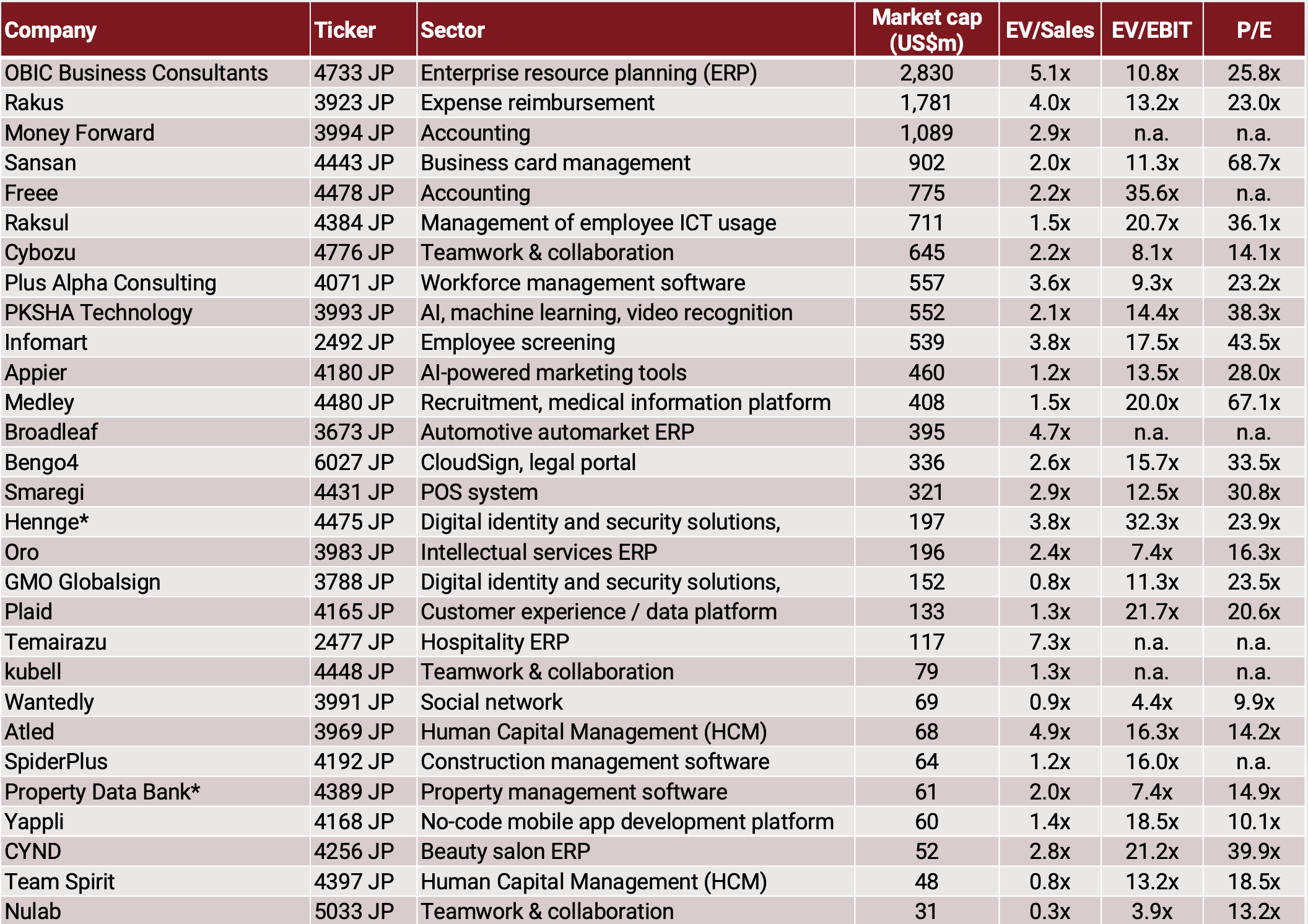

Here's the investable universe of companies within Japan's SaaS industry – a major focal point for software investors within the Asia-Pacific region:

In my view, the companies most at risk are point-solution software developers such as Rakus (the expense reimbursement part), Sansan (the business card OCR part), Bengo4 (the e-signatures part) and Yappli (their no-code mobile app development service).

I also think that Nulab (collaboration software), TeamSpirit (collaboration software) and Hennge (digital identity solutions) might be disrupted. Their customers are often savvy enough to switch to competing alternatives, including from tech giants like Microsoft.

Conversely, enterprise resource planning software suites like OBIC Business Consultant's Bugyo platform, Money Forward or Freee (accounting, payroll, etc.) enjoy significant bargaining power against their customers. I also think that Broadleaf (automotive aftermarket marketplace), Medley (electronic health record systems for hospitals) are moaty businesses with massive switching costs for their customers.

Whether their moats will protect them from the ongoing disruption in the software industry is unclear. But it certainly feels like there's an extreme level of pessimism within the investment community. And moats will remain moats, even in the age of AI.

{kind=link}